We’ve had days of negative funding, yet the market refuses to break down. That alone says more than most indicators right now. Shorts are literally paying to stay in their positions, while price has quietly climbed nearly 23% from the February lows—and still, no one seems willing to step back.

This isn’t just positioning anymore. It’s something deeper.

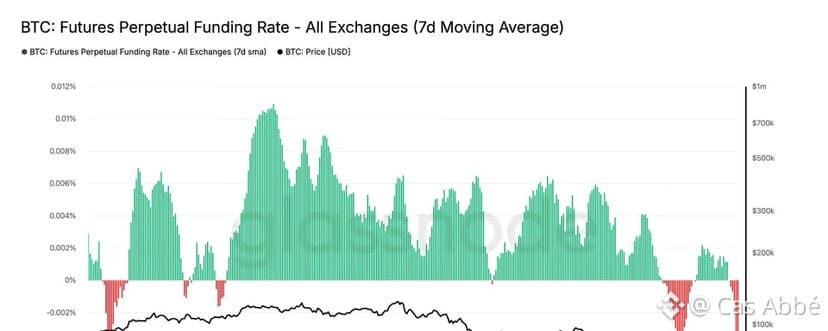

Looking at K33’s latest data, the extended stretch of negative funding stands out. But it’s not just the streak—it’s the context around it. The last time we saw this kind of persistence, the market was forming a bottom. The pattern was similar: traders heavily leaning in one direction, while price moved against that bias.

CryptoQuant data reinforces this picture. Funding rates have dropped to around –0.011, which isn’t just slightly negative—it’s aggressively skewed. That kind of reading usually signals a one-sided market. You don’t need complex models to interpret it. When everyone is on the same side, the risk builds naturally.

Santiment data tells a similar story. Short exposure remains elevated, sentiment is tilted bearish, and the crowd is behaving exactly as you’d expect. But this doesn’t feel like fresh fear—it feels recycled. Like traders are reacting based on past pain rather than present conditions.

The memory of the October crash still lingers. That event didn’t just liquidate positions—it changed behavior. Since then, every rally has been treated with suspicion. Every upward move is faded, assumed to be a trap. Shorts are being added as price rises, not when it falls. That’s not disciplined strategy—it’s emotional response. Call it revenge trading or fear-driven hedging, but it’s clearly visible.

And it’s not going away.

Open interest continues to creep higher alongside this trend. That means more leverage, more conviction, and more traders convinced they’re right. Historically, that’s when things become unstable—when crowded positions start reinforcing each other.

Meanwhile, price just sits there. Holding steady. Grinding upward. Refusing to deliver the breakdown everyone is betting on.

That’s where the irony comes in.

The market isn’t squeezing yet—but it’s starting to lean in that direction. Slowly, quietly. Because if price pushes higher, even slightly, the unwind could accelerate quickly. Short positions don’t close calmly—they get forced out. And once that process starts, it tends to cascade.

That said, nothing here is guaranteed. Negative funding can persist longer than expected. Markets can stay stagnant. Macro conditions are still uncertain, and liquidity remains thin. The same environment that contributed to the October wipeout hasn’t fully disappeared.

But the imbalance is clear.

The crowd is paying to be right—and the market isn’t confirming it.

That’s often where reversals begin.