I have been watching the CLARITY Act unfold for a while now, and the more I follow it, the more it feels like one of those stories that should have been simple—but just isn’t. I spent a lot of time on research trying to make sense of the latest draft, expecting some kind of clarity or direction, but instead I found a situation that’s getting even more tangled, especially with banking groups stepping in again with fresh concerns.

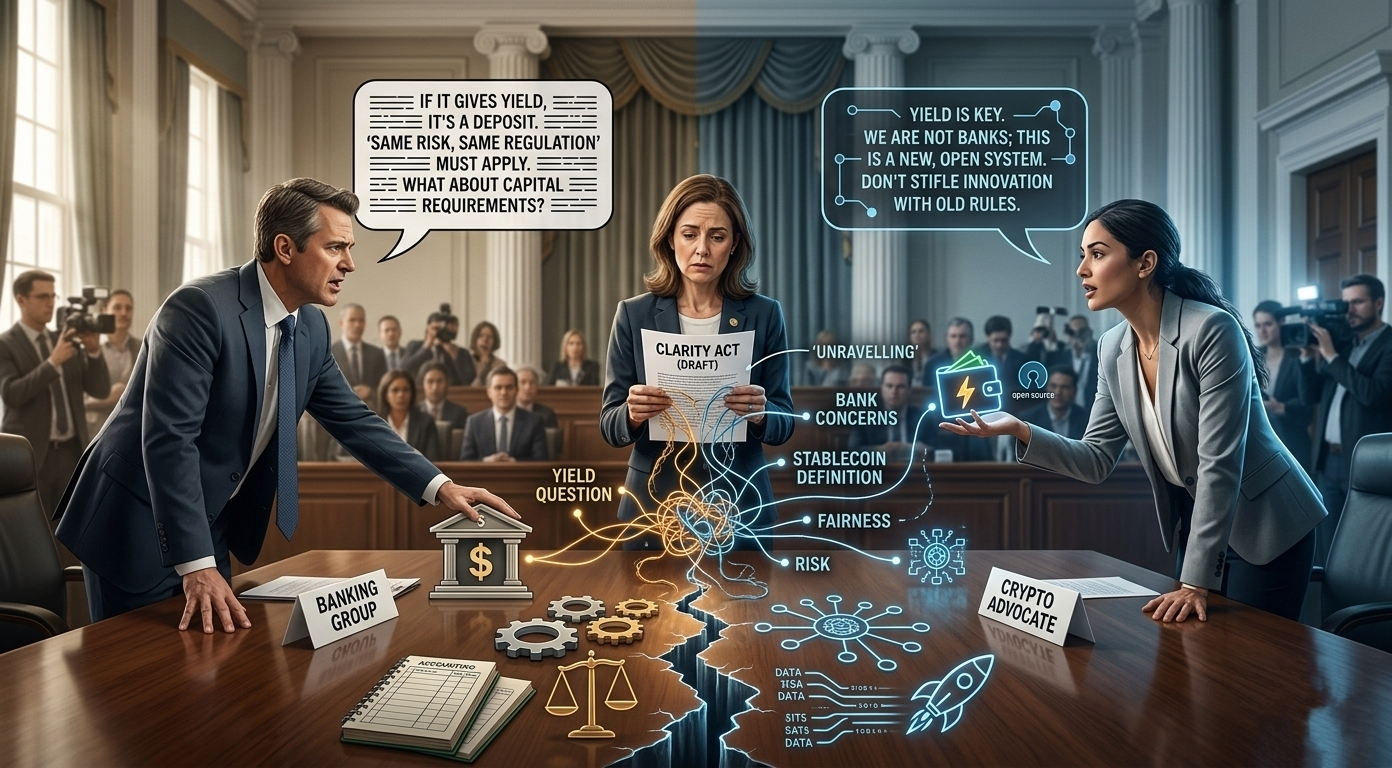

At the center of everything is this idea of stablecoin yield. On paper, it sounds straightforward—people hold stablecoins, and in some cases, they earn a return on them. But I have been watching how this small detail is causing a much bigger debate. It’s not just about yield; it’s about what stablecoins are supposed to be in the first place. Are they just digital dollars meant for payments, or are they turning into something closer to bank deposits or investment products?

From what I have seen during my research, banks are clearly uncomfortable. And honestly, their reaction feels more human than people admit. They’re looking at stablecoin issuers offering returns without the same rules banks have to follow, and it doesn’t sit right with them. I spent time reading through their concerns, and the message is consistent—they’re worried about fairness, about risk, and about what happens if things go wrong in a space that isn’t regulated the same way traditional banking is.

At the same time, I have been watching the crypto side push back just as strongly. For them, this isn’t just policy—it’s about identity. They see stablecoins as part of a new financial system that’s supposed to be faster, more open, and less dependent on traditional institutions. I spent a lot of time on research trying to understand their perspective, and it comes down to this fear that too many restrictions could strip away what makes this space different in the first place.

What makes everything feel uncertain is that there doesn’t seem to be a middle ground yet. I have been watching each new version of the draft try to smooth things out, but every attempt seems to create new friction somewhere else. The yield issue, in particular, keeps coming back like an unresolved question no one can fully agree on. Should companies be allowed to share earnings with users, or should that be something only banks can do? It sounds technical, but it’s actually shaping the entire direction of the industry.

Another thing I noticed while spending time on research is how much of this debate is really about trust. Banks lean on decades of regulation and structure, while the crypto world often builds on the idea that those same systems don’t always work for everyone. I have been watching how these two mindsets clash, and it doesn’t feel like something that can be solved overnight with a single piece of legislation.

There’s also a political undercurrent that’s hard to ignore. The more I looked into it, the more it became clear that this isn’t just about finance—it’s also about who gets to define the future of money. I spent time on research following how different voices approach the issue, and it often reflects bigger beliefs about innovation, control, and risk.

What really stands out to me is how uncertain everything still feels. I have been watching this process long enough to expect some progress by now, but instead it feels like we’re still circling the same core questions. The latest pushback from banking groups just reinforces that nothing is settled yet.

In the end, after everything I spent on research, I don’t see a clear finish line for the CLARITY Act just yet. It feels more like an ongoing conversation than a near-final decision. I have been watching closely, and if there’s one thing that seems certain, it’s that this debate—especially around stablecoin yield—is going to keep shaping how this all plays out.