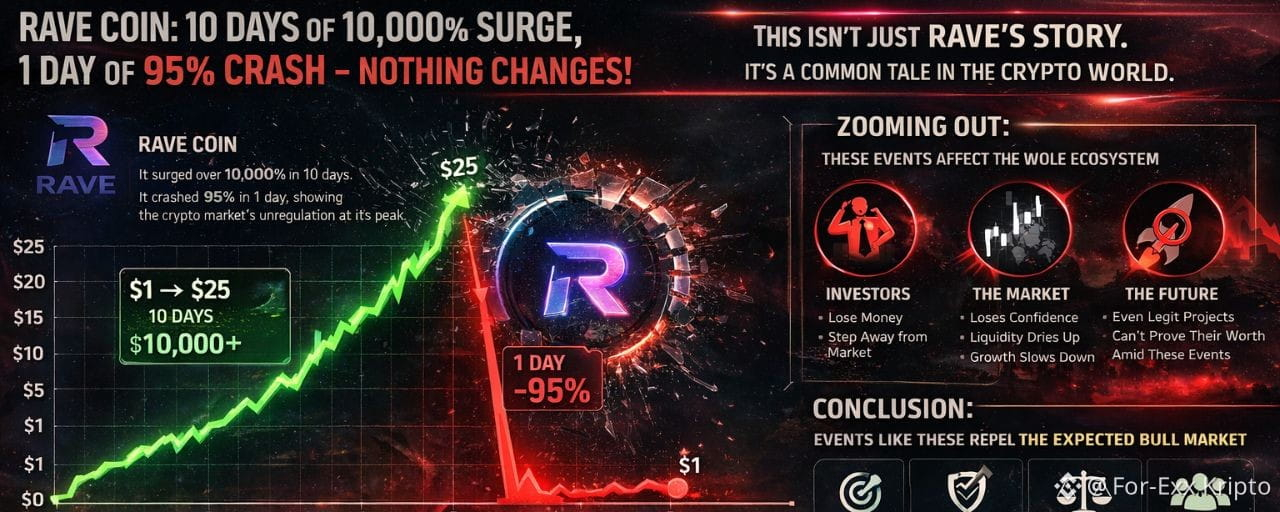

Imagine a token. On the first day of April, it trades below 50 cents. Almost no one is talking about it. Over the next fifteen days, the price rockets to 28 dollars, the market cap reaches 6.6 billion dollars, and the token enters the top 20 on CoinGecko, leaving behind well-known names like XMR, XLM, and ZEC. Then, in a single trading session, it falls roughly 85% and returns to wherever it came from. Left behind are tens of thousands of liquidated positions, investors who lost millions of dollars, and a familiar scenario repeating itself once again.

This is the story of $RAVE , the native token of RaveDAO. But in truth, this is not the story of one token; it is the story of a system. And the real question we must examine is not only how the event unfolded, but who saw what and when, when they acted, and why they did not.

The Pages of a Playbook

On-chain investigators established early on that the RAVE move was no coincidence. The timeline speaks for itself. While the price was still below 50 cents, addresses linked to RaveDAO's deployer wallets transferred 18.58 million tokens to Bitget. There was no announcement, no disclosure. About 10 hours later, the move began and did not stop. Roughly three days after this transfer, on April 13, angel investor Jeremy was among the first to sound the alarm on X: unusual wallet movements from deployer addresses to exchanges, futures open interest exceeding 200 million dollars, RSI piercing the 95 level, and daily trading volume rivaling the token's entire market cap. The full picture had already been laid out in publicly available data while the price was still at a quarter of its eventual peak.

Seventy-four percent of market participants on Binance were positioned short; that is, they were expecting a decline. At precisely this point, insiders began pulling back the tokens they had transferred to Bitget. Selling pressure was artificially drained. Every upward move triggered short liquidations, those liquidations turned into fresh buys, and a classic short squeeze chain unfolded. In just a 24-hour window, roughly 43 million dollars' worth of futures positions were forcibly closed on the exchanges; about 32 million of that came from the short side, a figure close to the token's entire market cap a week earlier. In liquidations, RAVE ranked third, behind only Bitcoin and Ethereum. A 60-million-dollar token sitting in the same table as Bitcoin and Ethereum shows how fragile the table itself had become.

The source of this fragility lies on the supply side, and it forms the backbone of the case. According to data from Arkham and other on-chain analytics platforms, more than 90% of RAVE's supply — roughly 248 million tokens — sits in just three Gnosis Safe wallets. Some researchers pushed this figure to 95.3%. A significant portion of the remaining supply is alleged to be distributed among user accounts on Bitget and Gate.io that are also linked to insiders. Gnosis Safe addresses are the multi-signature smart contract wallets project teams typically use for treasury management; meaning, these wallets are not technically owned by some "random whale," but are structures highly likely to belong to the project team. The picture is this: nearly the entire supply of a token is controlled by a handful of people around the same table, and the small remainder is the slice that changes hands among investors on the open market. It is hard to call this a "market," because there is no classical supply-and-demand balance; the insider's decision to sell alone can determine the fate of the token. Because circulating supply is so thin, when a thick enough wall of buyers is set up, the price can easily be pushed upward, and when that same wall is pulled, the price cannot find a floor to land on. The sharpness of ZachXBT's public call stems from this: he argues that it cannot be permitted for insiders holding more than 90% of the supply to continue extracting capital from retail investors. In his view, this is blatant market manipulation. Another striking detail is the project's backer list: RaveDAO's background includes names like World Liberty Financial, Warner Music Group, Tomorrowland, and YZi Labs — a Web3 incubator linked to former Binance staff. An impressive list, but it does not change what the on-chain data shows.

Moreover, if RAVE had been a unique case in crypto history, it might be filed away as a technical anomaly. But it is not. We have watched similar parabolic rallies and subsequent collapses in recent months in ARIA and SIREN. The scenario is the same every time: a low-liquidity token, supply heavily concentrated on the inside, coordinated transfers to exchanges, four-digit percentage gains within weeks, and then liquidity vanishing suddenly. As insiders walk off the stage with pockets full, only the retail investor is left on it. This is not a mistake; it is a playbook. And new editions of the same book are pushed to market each time with a different cover and a different project story.

The Exchanges' Delayed Reflex and the Legal Vacuum

The stance of the exchanges may be the most contested dimension of the case. Between April 1 and 13, as the price exited below 50 cents and went parabolic, abnormal transfers from deployer wallets to exchanges were happening; the supply concentration and transfer table were public, visible to anyone. On April 13 came Jeremy's detailed warning, and that same day 43 million dollars in liquidations occurred. On April 14, RaveDAO itself posted a warning from its official X account, stating that the project was observing heightened market volatility in RAVE and urging users to exercise caution regarding the associated risks, especially when using leveraged positions. This statement amounted to an admission that the project's own token was inside a problem. From April 14 to 17, the price continued its upward march, pushed toward 28 dollars, and the market cap exceeded 6.6 billion dollars — and still no statement from the exchanges.

On April 18, ZachXBT published a long post, alleging that the pump-and-dump activity originated on Bitget, Binance, and Gate, directly tagging Binance co-founder He Yi and Bitget CEO Gracy Chen, calling for internal investigations and the offboarding of responsible actors. He offered a personal bounty of first 10,000, then — with community contributions — 25,000 dollars for whistleblowers. Following the call, Bitget CEO Gracy Chen replied, announcing they had started investigating RAVEUSD. Binance CEO Richard Teng shortly issued a similar public statement, saying they were looking into the situation and would do their part to examine market misconduct. That same day, the price fell by about 85%, and 24-hour liquidations exceeded 48 million dollars. RaveDAO stated that its team was not involved in and not responsible for the recent price action; however, it did not directly address the concrete on-chain allegations regarding concentration and transfer timing. In the same statement, the project also acknowledged that portions of unlocked tokens were planned to be sold "when appropriate"; this admission, arriving in the middle of a 48-million-dollar liquidation event, only deepened the selling pressure.

This timeline makes an important question visible: were the exchanges late? The technical answer is clear. The fact that nearly the entire supply sat in a few wallets, the unusual transfers from deployer wallets to exchange accounts, the abnormal bloating of futures open interest — all were signals that Bitget and Binance could have detected with their own internal surveillance systems. Most of these signals were observable by any user through publicly available sources. To launch an investigation only after waiting for an external investigator to issue a public call, while the data was already there, is an admission of how many billions of dollars had to be dislocated before action was taken. If a surveillance mechanism notices the red flags on its own screens only after someone from outside points them out, that mechanism is not truly functioning. To be fair, there are practical difficulties in having exchanges actively monitor every listed token at all times; however, when the token in question is one whose market cap jumps from 60 million to 6 billion dollars in a week, that ranks third in futures liquidations alongside Bitcoin and Ethereum, and whose supply distribution is strikingly imbalanced, the "it only just came onto our radar" explanation becomes strained. The speed of the CEOs' social media responses may show they are not indifferent to the issue; but the fact that this speed manifested after the event, not before it, does not eliminate the core critique. Deterrence is built not through an investigation opened after the event, but through a surveillance infrastructure that prevents the event from starting. Moreover, Bitget and Binance have given no commitment on how long their investigations will take; Gate has yet to issue a public response; and concrete findings reports and restitution mechanisms are still not on the table.

Behind this picture lies a larger gap, and that is where the real problem sits. In traditional markets, a stock rising 10,000% in a month and then dropping 85% in a single session is unthinkable. If such a move occurred, the SEC, FCA, or the relevant regulator would halt trading within hours; open an investigation under headings like insider trading, market manipulation, and wash trading; and those found guilty would face million-dollar fines and even prison sentences. For this reason, manipulation has not fully ended in traditional markets either, but it carries a deterrent cost. In the crypto market, though, the token is issued in one jurisdiction, the team sits in another, the exchanges are registered in a third, and the investors come from all over the world. This geographic blur serves as the excuse for no regulator being able to claim full authority. Independent investigators like ZachXBT document events one by one, exchange CEOs say "we are looking into it" on social media, and occasionally a token is delisted. But no one can step forward and say, "Here is the person who traded on inside information, here is the penalty." The enforcement chain is broken. For the insider actor, the risk-reward balance is clear: the potential of millions of dollars in gains against near-zero risk of punishment. In such an equation, manipulation is not expected to decrease — it is expected to increase.

The Real Cost: Stolen Reputation and a Delayed Bull Market

The invisible real cost of such moves is not the millions directly lost. Because those millions ultimately flow within the market, from one pocket to another. What is truly lost is the institutional reputation the sector has painstakingly tried to build. 2024 and 2025 were a quiet transformation period for crypto. Spot ETFs were approved, large asset managers expanded their allocations, and the regulatory framework in the U.S. gradually took shape. The question the institutional world had been asking for a decade — "is this asset class suitable for investment?" — slowly began to be answered with "yes, under certain conditions." But every RAVE case expands the "under certain conditions" part of that sentence and reframes the question.

Imagine a pension fund manager, a family office CIO, a treasury team at an insurance company. Their duty is to protect capital. To them, a token rising 10,000% is not an enticing opportunity but a red flag. As long as the manager's question "what is our exposure in this sector?" is answered with "there, just last week, a token fell 85% in a day, and no one could do anything before it happened," institutional capital will remain reluctant to flow into this space in full. If crypto wants to be taken seriously by macro capital, it must behave like a serious market. The same holds for the anticipated bull cycle. The liquidity is ready right now: the direction of Fed rate cuts, the trajectory of global M2, capital flows in Asia — all paint a supportive backdrop for risk assets. But for that backdrop to expand from Bitcoin to altcoins, and from altcoins to mid-cap and small tokens, trust is required. As long as the retail investor feels that every altcoin rally is being used as an "exit door," they will not enter the next bull market with the same courage. As long as the institutional investor views the altcoin side as an unregulated casino, they will not extend their mandate beyond Bitcoin and Ethereum. Trust is the precondition of liquidity; without trust, a bull market, at best, is a bull market limited to a few majors.

A Way Forward and Conclusion

This picture seems bleak, but it is not unsolvable. On the exchange side, the tightening of listing standards, additional transparency obligations for tokens whose supply distribution exceeds a certain concentration threshold, internal systems that monitor insider wallet movements in real time, and automatic trading halt mechanisms for suspicious movements are all technically possible. The clearest lesson the RAVE case teaches is this: a token whose 90% of supply sits in a few wallets should already be on the red-flag list; large transfers from deployer wallets to exchanges should trigger an automatic review flow; futures open interest exceeding market cap should sound an alarm. These measures may reduce short-term volume revenue for exchanges, but they preserve their long-term institutional and regulatory relationships. On the regulatory side, MiCA has clarified the framework in Europe; in the U.S., the division of authority between the SEC and CFTC is taking concrete shape step by step; in Asia, Japan, Singapore, Hong Kong, and the United Arab Emirates have established their own frameworks. The next stage is information sharing and coordinated enforcement across these jurisdictions in manipulation cases. An actor issuing a token in Singapore, trading from Dubai, moving liquidity to an exchange registered in the Caribbean, and harming a retail investor in the U.S. should no longer be viewed as a case of "unclear who has authority." Within the sector itself, the work of on-chain investigators has become the most valuable self-regulation layer in crypto over the past two years. Cases documented by names like ZachXBT can now become reference sources even for regulators. It is critical that this layer grow, that a stronger media ecosystem support it, and that communities continue to pressure exchanges on listing decisions. In RAVE, what moved the exchanges was ZachXBT's public call; that is a success, but at the same time, it is an admission of the sector's own internal mechanisms' inadequacy.

RAVE is not a new event; it is the new face of an old problem. A token falling from 28 dollars to 2 dollars actually vaporizes more than just a few billion dollars of market cap. It also carries away with it part of the capital that would flow to the crypto market in the next bull cycle. Because the one feeling institutional and retail investors share is the loss of trust; and trust, once lost, is the most expensive asset to rebuild. Exchange investigation statements are of course important, but not enough on their own. Unless those statements are followed by concrete findings, offboarded actors, restitution mechanisms, and most importantly, structural measures to prevent the same scenario from repeating, these investigations will not go beyond being a consolation prize for the market. Retail investors are now watching how each exchange approaches this case, and waiting to see who will answer the question of who will stop the repeating playbook, and when. Crypto has been one of the fastest-maturing asset classes in financial history; sustaining that maturation will take more than saying "we've grown up." If it is to behave like a major market, it must hold itself to the minimum standards of major markets. Otherwise, every parabolic candle pushes the next bull market a little further away, and every abrupt collapse drives a few more new investors who believed in the crypto story away from the market. The pages of the playbook are now being read by everyone. Putting this book back on a dusty shelf is the sector's most basic debt to its own future.