As BTC struggles to reclaim the $100,000 milestone, the spotlight has intensified on MicroStrategy ($MSTR) and its Executive Chairman, Michael Saylor.

The firm's aggressive "Bitcoin Treasury" model, which has turned $MSTR into a high-beta proxy for the king of crypto, is facing its toughest test yet. With the stock lagging during the current market dip, critics are asking: Has the "Saylor Play" become too risky?

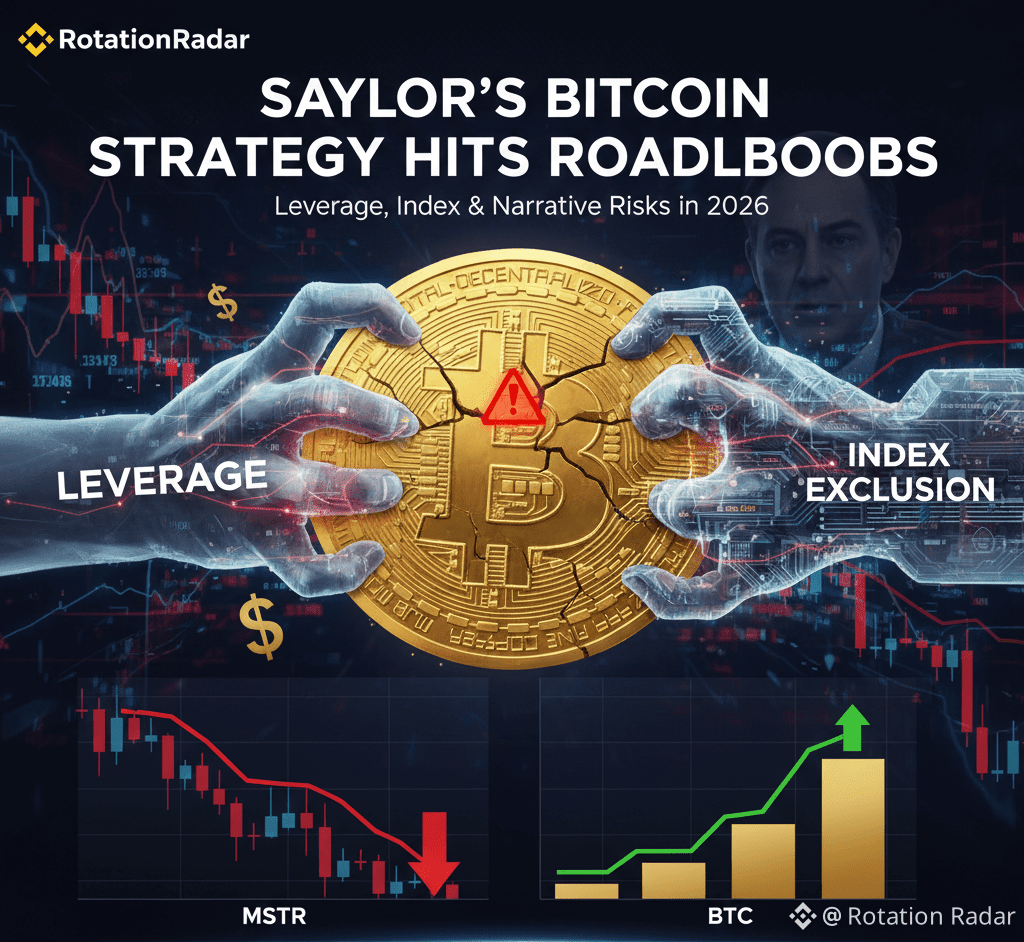

The Performance Gap: $MSTR vs. $BTC

While BTC has seen a healthy consolidation after its 2025 highs, MicroStrategy’s stock has shown deeper wounds. Historically, $MSTR traded at a massive premium to its Net Asset Value (NAV)—sometimes as high as 2x to 3x the value of its Bitcoin holdings.

Current Data Snapshot:

* BTC Holdings: 687,410 $BTC (Current value: ~$62.3 Billion) ₿

* Average Cost: ~$75,353 per BTC

* The "NAV Gap": In early 2026, $MSTR’s premium has largely evaporated. During the recent dip to $87,000, the stock briefly traded at a discount, with a market cap below its underlying Bitcoin value.

This "premium collapse" is critical. Without a high stock premium, Saylor's primary engine for growth—issuing equity to buy more $BTC stalls.

The Three Pressing Risks

1. The Index Reclassification ⚖️

A major "black swan" was narrowly avoided this month. MSCI (Morgan Stanley Capital International) considered reclassifying $MSTR as an "Investment Company" rather than an operating software firm. While MSCI ultimately decided to retain the company in its indexes for now, they have placed $MSTR in a "penalty box," refusing to increase its weighting despite new share issuances.

2. The Debt & Dividend Burden 💸

MicroStrategy now carries significant liabilities, including its "Class A" common stock and perpetual preferred stocks ($STRC, $STRD). To service approximately $844 Million in annual dividends and interest, the firm must maintain its cash reserves. While Saylor recently boosted USD reserves to $2.25 Billion, any prolonged BTC bear market could pressure the firm to sell assets.

3. ETF Cannibalization 🏦

With the maturity of spot $BTC ETFs in 2026, institutions now have a cheaper, direct way to gain exposure without $MSTR's management fees or corporate leverage. This is siphoning off the "scarcity value" the stock once held.

Saylor’s Defense: The "42/42" Plan ₿

Despite the headwinds, Saylor remains defiant. He is moving forward with his "42/42" plan, targeting a total capital raise of $84 Billion over the next few years to stack more $BTC.

> "Orange or Green?" Saylor recently teased on X, referring to his strategy of adding to either Bitcoin or USD reserves to ensure the company never becomes a forced seller.

RotationRadar’s Take 🔍

The debate for 2026 is whether MicroStrategy is a leveraged genius play or a fragile house of cards. If BTC breaks $120,000, $MSTR will likely rocket back to a massive premium. But if the $95,000 support fails to hold, the "leverage flush" could be painful for bulls.

What’s your play?

Are you buying the $MSTR dip for a leveraged bounce, or sticking to spot BTC for safety?

#Bitcoin #MicroStrategy #MichaelSaylor #cryptotrading #BullMarket