Stablecoins have solved one major problem in crypto: price volatility. What they have not fully solved is credit. A financial system only becomes functional when capital can move predictably, be borrowed responsibly, and support real economic activity.

Plasma’s collaboration with Aave offers a useful case study in how a stablecoin-based credit market can be designed from first principles rather than short-term growth targets.

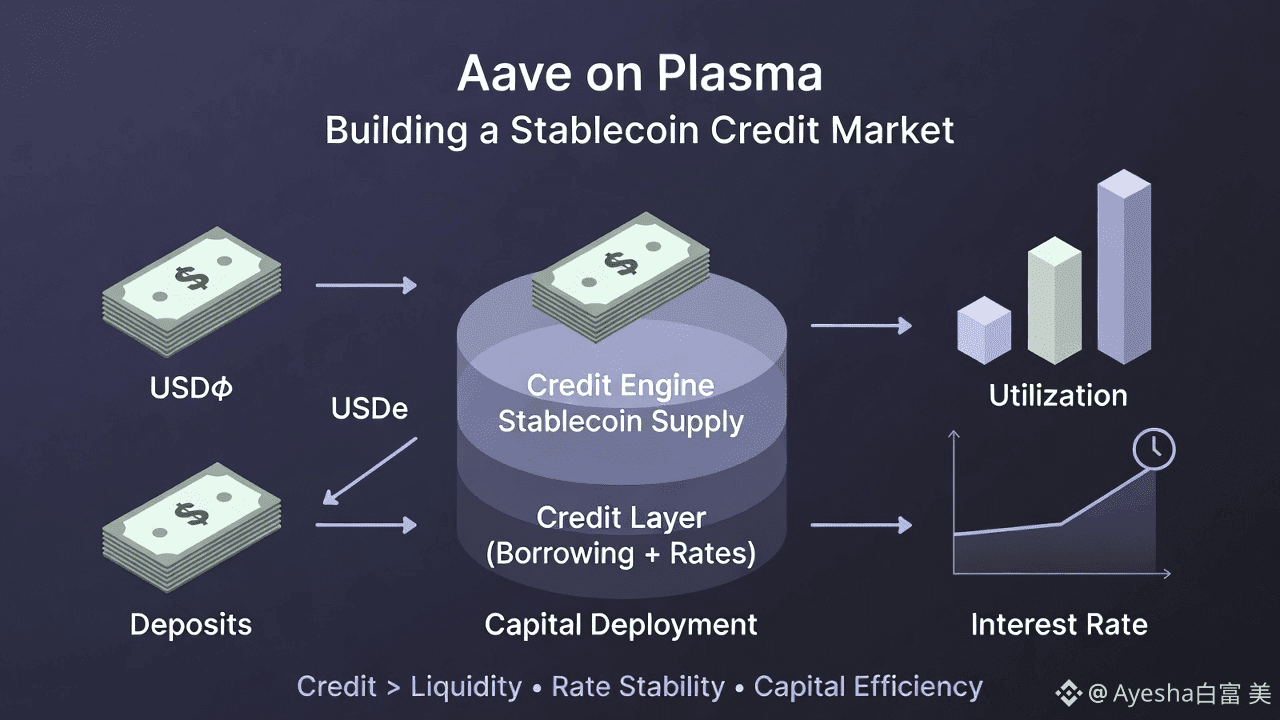

Why a Credit Layer Matters More Than Liquidity

Liquidity alone does not create a financial system. Large deposits can exist without generating meaningful economic output. Credit, on the other hand, measures intent. When users borrow, they are expressing conviction—either in leverage, yield, or capital efficiency.

Plasma’s approach focuses on transforming stablecoin deposits into usable borrowing capacity. The objective is not to maximize headline numbers, but to make stablecoins behave like productive capital that can support strategies across different market conditions.

This shift from passive liquidity to active credit is what separates infrastructure from experimentation.

Borrow Rate Stability as Infrastructure, Not Incentive

Many lending markets rely on fluctuating incentives to attract users, often resulting in volatile borrow rates. This creates an environment where strategies only work temporarily and collapse once conditions change.

On Plasma, the emphasis has been on rate predictability. Stable USD₮ borrowing costs allow users to plan leverage and yield strategies without relying on perfect timing. For institutions and advanced users, this consistency is more valuable than momentary low rates.

Predictable borrowing costs turn DeFi from speculation into financial tooling.

Incentives as a Catalyst, Not a Crutch

The $XPL incentive allocation tied to Aave’s deployment played a specific role: activating liquidity early while the market matured. The key distinction is that incentives were used to initialize the system, not to sustain artificial demand.

What followed was more important than the inflow itself. Liquidity transitioned into active borrowing, showing that users were not simply chasing rewards but engaging with the credit market.

This behavior suggests that the underlying structure was strong enough to stand beyond incentive cycles.

Preparing for Scale Before Capital Arrives

A common failure mode in DeFi is attracting capital before systems are ready. Plasma avoided this by defining risk parameters, oracle integrations, and asset configurations early.

This preparation allowed the Aave market on Plasma to handle large capital flows without destabilizing rates or utilization. When borrowing activity increased, the system responded smoothly rather than defensively.

This is a subtle but important signal of maturity.

Native Assets and Capital Efficiency

Another structural choice was the use of LayerZero-native assets under the OFT standard. Assets like USD₮0, USDe, sUSDe, and weETH can move into Plasma without fragmentation, slippage, or liquidity breakage.

For users, this matters more than it appears. Capital that moves cleanly is capital that can be deployed immediately. Frictionless movement reduces hidden costs and improves strategy execution, especially at scale.

Efficient capital movement is a prerequisite for efficient credit.

Why Borrowing Activity Tells the Real Story

Total deposits are often used as a proxy for success, but they only show supply. Borrowing shows demand.

On Plasma, a significant portion of supplied liquidity is actively borrowed. This indicates that users are deploying capital into leverage, yield looping, and balance-sheet optimization rather than leaving it idle.

High utilization across key assets suggests that the credit market is functioning as intended, recycling capital instead of storing it.

The Importance of Rate Consistency Over Time

One of the clearest signals of market health is how borrowing costs behave under changing conditions. Plasma’s USD₮ borrowing rates have remained relatively stable even as total liquidity shifted.

For leverage-based strategies, rate spikes can be fatal. For yield strategies, unpredictable costs erode margins. Consistency allows strategies to be evaluated on fundamentals rather than short-term noise.

This stability moves the market closer to traditional credit behavior while retaining onchain transparency.

Concentration as a Design Choice

Rather than listing many borrowable assets, Plasma focused borrowing around a small set: USD₮0, USDe, and WETH. This concentration deepens liquidity, improves utilization, and reduces fragmentation.

Supply-only assets still play an important role as collateral, but separating borrowing from collateral complexity simplifies risk management.

Deep markets are usually healthier than wide but shallow ones.

Plasma’s Rapid Position Within Aave

Plasma’s rise within the Aave ecosystem is notable not because of size alone, but because of efficiency. High utilization and meaningful borrowing activity indicate that capital is being used, not just parked.

This matters because it reflects organic demand rather than incentive dependency. Markets that rely solely on rewards often shrink once incentives fade. Markets driven by borrowing needs tend to persist.

How Collateral Becomes Productive Capital

Yield-bearing collateral is central to Plasma’s credit design.

Ethena’s sUSDe allows users to earn asset-level yield while borrowing stablecoins against it. This creates stacked efficiency: yield from the asset, incentives from lending, and liquidity from borrowing.

Ether.fi’s weETH follows a similar logic for ETH holders, enabling borrowing without giving up staking exposure. This approach aligns with how sophisticated capital allocators think—maximizing efficiency without sacrificing core positions.

What This Architecture Enables Long-Term

The early performance of Aave on Plasma suggests a broader trajectory. A functioning credit layer is the foundation for connecting DeFi to real economic activity.

As integrations expand into on-ramps, off-ramps, FX, payments, and custody, stablecoin credit can move beyond onchain strategies into settlement, treasury management, and cross-border flows.

This is where stablecoins evolve from digital representations of dollars into financial infrastructure.

Plasma’s credit market is not an endpoint. It is a base layer for building how stablecoin-denominated finance operates at scale.