When settlement ceases to be a footnote, you begin to notice just how much of finance relies on quiet, delicate mechanisms.” I was put in mind of this as I waited for a routine securities transaction to clear: The trade, of course, occurred in an instant, but the settlement took several days. This has all happened with complete normalcy, nothing whatsoever was amiss, and yet this interlude between agreement and actual ownership strikes one as inconsequential, and yet precisely this interlude has not been an accident of the system.

This gap is where the opinion of Dusk Network on on-chain settlement of securities manifests itself. It’s not a focus on speed for the sake of speed; it’s a concern with regard to a reliable function under regulatory restrictions. On-chain settlement in general is looked upon as a back-office function.

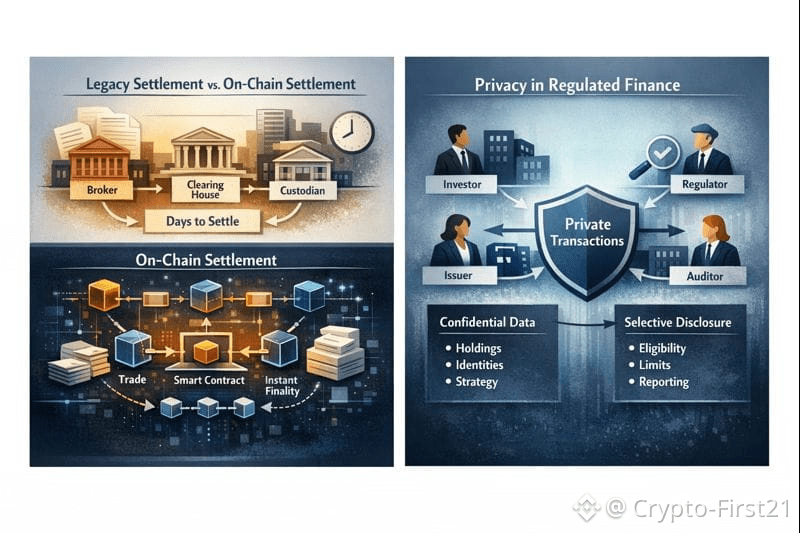

On-chain settlement can be described as follows: when it comes to on-chain settlement, it essentially implies that the ledger is the final authority on ownership. In traditional markets, when an exchange is made, it involves a series of clearing and reconciliation processes followed by custody updates. This is followed by the legal transfer of ownership. When settlement ceases to be a footnote, you begin to notice just how much of finance relies on quiet, delicate mechanisms. I was put in mind of this as I waited for a routine securities transaction to clear: The trade, of course, occurred in an instant, but the settlement took several days. This has all happened with complete normalcy, nothing whatsoever was amiss, and yet this interlude between agreement and actual ownership strikes one as inconsequential, and yet precisely this interlude has not been an accident of the system.

This gap is where the opinion of Dusk Network on on-chain settlement of securities manifests itself. It’s not a focus on speed for the sake of speed; it’s a concern with regard to a reliable function under regulatory restrictions. On-chain settlement in general is looked upon as a back-office function.

On-chain settlement can be described as follows: when it comes to on-chain settlement, it essentially implies that the ledger is the final authority on ownership. In traditional markets, when an exchange is made, it involves a series of clearing and reconciliation processes followed by custody updates. This is followed by the legal transfer of ownership. Settlement infrastructure should be reliable over economic cycles, not necessarily attuned to periods of high activity.

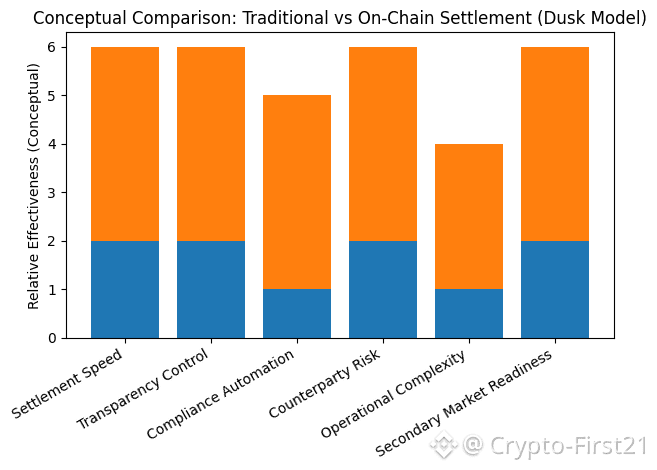

In the overall market environment, on-chain settlement of securities is not competing with retail trading platforms. Rather, on-chain settlement is competing with existing infrastructure that is well-established and recognized under the law. This is a matter of regulatory approval and working comfortably with existing infrastructure, which is inherently an incremental process.

There are certainly risks involved. The lack of regulatory harmonization by geographic area may impede adoption. The added complexity from privacy-preserving networks must be carefully balanced. The force of institutional inertia, not to be underestimated, takes time for standards to develop. The strategy proposed by Dusk does not lack these challenges, but reduces their scope with a settlement solution that starts in the area where there are known and valuable efficiencies to be gained.

What’s striking is the unremarkable nature of all this work. There aren’t any stories, only a careful consideration for the role of privacy, compliance, automation, and incentives. But it’s the settlement level where markets work or break. There isn’t any hype here. This kind of infrastructure is creating financial plumbing that should simply work and fade into the background. That’s the important part of this kind of infrastructure, and it’s why it matters more than speculation. It’s a shift in understanding blockchain from an experiment to a reliable infrastructure.