The frustration didn’t come from a bad trade, but from trying to move funds between two venues during a volatile session. The transaction went through, then sat in a strange limbo. Not failed, not settled. Just waiting. I knew the mechanics well enough to explain it, but that didn’t make it less uncomfortable. In trading, uncertainty is expected. In payments, even brief ambiguity feels like a flaw rather than a feature.

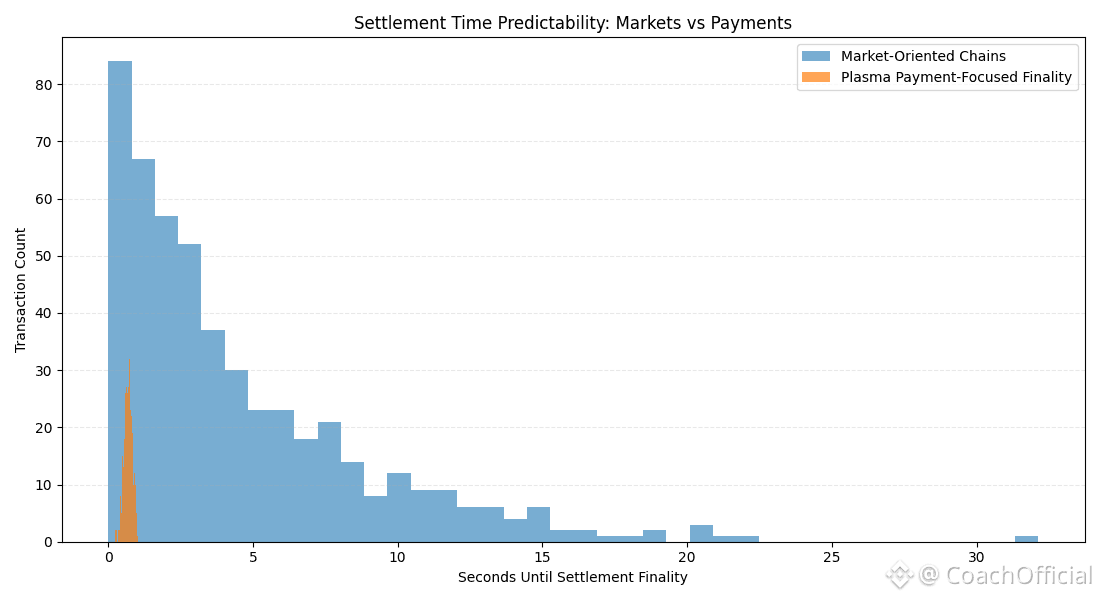

The underlying problem is simple. Many blockchains were designed with markets in mind, not everyday settlement. Probabilistic finality, reorg risk, and variable fees are manageable when you are speculating. They become liabilities when the system is used to pay salaries, settle invoices, or move stablecoins at scale. Payments demand predictability more than optional upside.

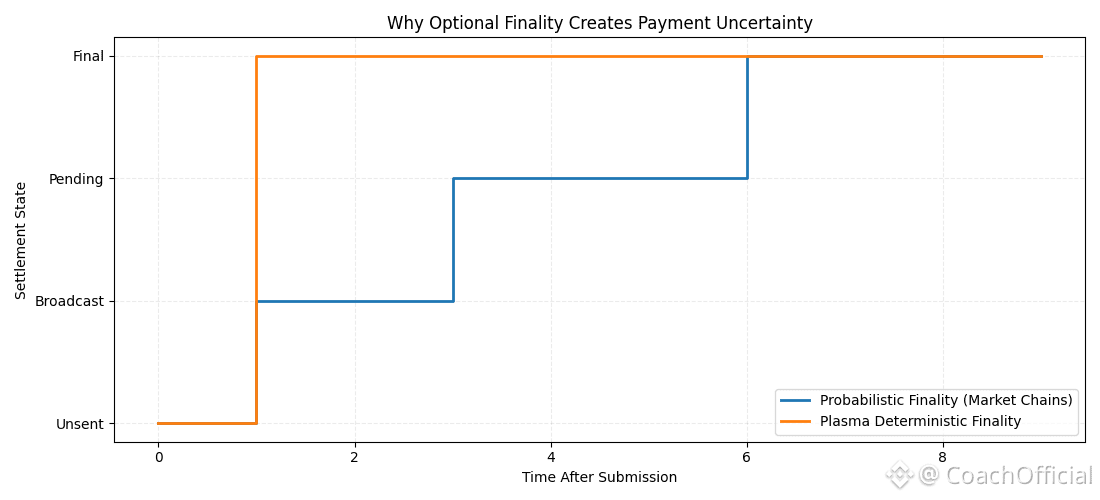

The analogy that fits best is card payments. Imagine a point-of-sale terminal that says “approved, unless reversed in a few minutes depending on network conditions.” No merchant would accept that. Speed matters, but certainty matters more.

This is the design gap that Plasma tries to address. In plain terms, it is a Layer 1 built specifically for stablecoin settlement rather than general-purpose activity. One implementation detail is its consensus mechanism, PlasmaBFT, which targets sub-second finality so transactions are considered settled almost immediately. Another is its use of a modified Ethereum execution environment via Reth, allowing existing smart contracts to run while operating under stricter settlement guarantees.

The system also makes deliberate UX tradeoffs. Stablecoins can be used to pay transaction fees, and transfers can be structured to feel closer to payment rails than to trading infrastructure. That does not make the network faster in every dimension. It makes it more predictable, which is the point.

The token’s role is structural. It secures the network through validator staking, pays for execution when stablecoins are not used directly, and governs parameters related to settlement and fees. It does not turn payments into speculation. It supports the machinery that makes settlement reliable.

Market context explains why this focus exists at all. Stablecoins now process well over $10 trillion in annual transfer volume, often rivaling traditional payment networks in raw throughput. At the same time, most of that activity still relies on blockchains where finality is probabilistic and fees fluctuate. That mismatch is increasingly visible as usage shifts from trading desks to real-world payment flows.

From a short-term trading perspective, payment-focused infrastructure can look uninteresting. Price action tends to follow narratives, liquidity cycles, and broader risk sentiment. Long-term infrastructure value shows up differently. It accumulates through consistent behavior under load, through integrations that choose reliability over optionality, and through systems that are boring in the best sense of the word.

There are real risks. Competition from established Layer 1s and specialized payment rails is intense, and network effects are hard to displace. A plausible failure mode is underestimating adversarial conditions. If sub-second finality assumptions break during coordinated attacks or validator outages, trust erodes quickly. There is also uncertainty around adoption paths. Building for payments does not guarantee users will migrate if existing systems remain “good enough.”

I do not assume certainty belongs exclusively to any one design. What feels clear is that payment networks fail quietly when finality is treated as optional. Markets can live with ambiguity. Daily settlement cannot. Whether this approach becomes standard will depend less on attention and more on time, usage, and how often the system does exactly what it promises without needing explanation.

@Plasma #plasma #Plasma $XPL