Większość traderów nie budzi się myśląc o infrastrukturze płatniczej. Ruch cenowy jest głośny. Narracje są jeszcze głośniejsze. Uwaga podąża za zmiennością.

Jednak stablecoiny cicho stały się najważniejszym przypadkiem użycia kryptowalut w realnym świecie na długo przed tym, jak rynek w pełni to dostrzegł.

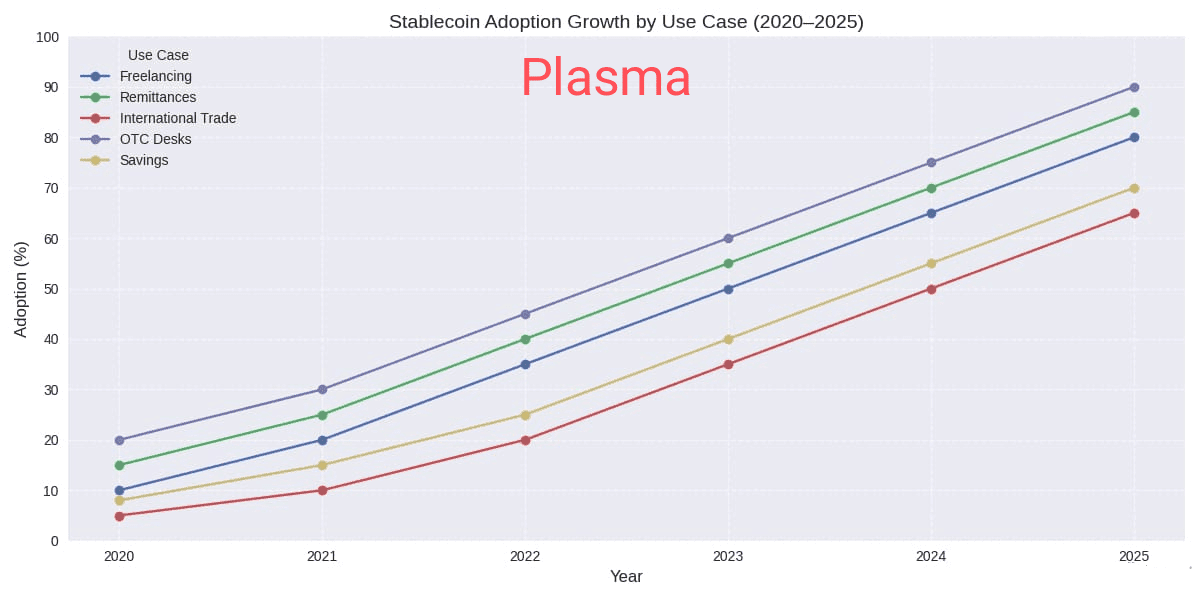

Widzisz to w freelancingu, przekazach pieniężnych, handlu międzynarodowym, biurach OTC i codziennych oszczędnościach w krajach z kruchymi lokalnymi walutami. Ludzie nie używają stablecoinów, ponieważ kochają blockchainy. Używają ich, ponieważ cyfrowe dolary poruszają się szybciej niż banki, sięgają dalej niż karty i działają, gdy tradycyjny system jest zamknięty.

To zapotrzebowanie stawia proste pytanie: jeśli stablecoiny są produktem, dlaczego wciąż muszą działać na ogólnych blockchainach, które nigdy nie były projektowane do płatności?

To problem, który Plasma ma rozwiązać.

Plasma to warstwa 1 zaprojektowana specjalnie dla stablecoinów i globalnych płatności, z USD₮ (Tether) jako jej głównym celem od pierwszego dnia. Zamiast traktować transfery stablecoinów jako po prostu inny typ transakcji konkurujący z monetami memowymi, NFT i grami na łańcuchu, Plasma jest zbudowana wokół idei, że płatności powinny być głównym zadaniem łańcucha – a nie poboczną misją.

Sieć pozycjonuje się jako wysokowydajna L1 zoptymalizowana pod kątem płatności USD₮ na globalną skalę, podkreślając niemal natychmiastowe rozliczenia, niskie opłaty i pełną kompatybilność z EVM. Dla inwestorów prawdziwy sygnał nie tkwi w języku marketingowym – to implikacja. Łańcuch płatności nie jest oceniany na podstawie liczby aplikacji, które na nim powstają, ale na podstawie tego, czy może niezawodnie obsługiwać powtarzalny, wysokowolumenowy, niskomarginalny ruch pieniędzy. To bardzo inne pole bitwy niż typowy wyścig zbrojeń L1.

Najbardziej niedocenianym problemem doświadczeń użytkowników w stablecoinach jest gaz. Na większości blockchainów użytkownicy muszą posiadać oddzielny zmienny token, aby przenieść swoje stablecoiny. Teoretycznie to normalny projekt kryptograficzny. W praktyce łamie narrację płatności w momencie, gdy próbuje stać się mainstreamem. Wysłanie komuś 20 dolarów w USDT nie powinno wymagać najpierw zakupu innego aktywa. Dla traderów to trywialne. Dla zwykłych użytkowników to problem nie do zaakceptowania.

Plasma zajmuje się tym bezpośrednio za pomocą mechanizmów natywnych dla stablecoinów. Łańcuch obsługuje transfery USD₮ bez gazu za pośrednictwem systemu relayer/paymaster, który jest konkretnie ukierunkowany na bezpośrednie płatności stablecoinami. Użytkownicy mogą przenosić środki bez myślenia o tokenach gazowych, zarządzaniu opłatami czy nieudanych transakcjach. To, co brzmi jak szczegół produktu, jest w rzeczywistości strategiczną infrastrukturą: eliminuje tarcia, obniża wskaźniki błędów i sprawia, że stablecoiny zachowują się bardziej jak pieniądz, a mniej jak kryptowaluta.

Z perspektywy struktury rynku, zmienia to ekonomikę wprowadzania na rynek. Gdy tarcie gazowe znika, stablecoiny stają się łatwiejsze do zintegrowania z aplikacjami konsumenckimi, kasami handlowymi, systemami płac i produktami przekazów. Płatności nie skalują się przez entuzjastów – skalują się przez zmniejszone tarcie. To tutaj twierdzenie Plasmy o 'globalnych płatnościach' wykracza poza branding.

Kompatybilność to kolejny kluczowy element. Plasma jest w pełni kompatybilna z EVM, co pozwala deweloperom na wdrażanie przy użyciu znanych narzędzi i portfeli Ethereum, zamiast uczyć się nowego stosu. Plasma nie prosi budowniczych o ryzykowanie w niszowym ekosystemie. Prosi ich, aby wprowadzili aplikacje płatnicze do środowiska zoptymalizowanego pod kątem tego, co stablecoiny robią najlepiej.

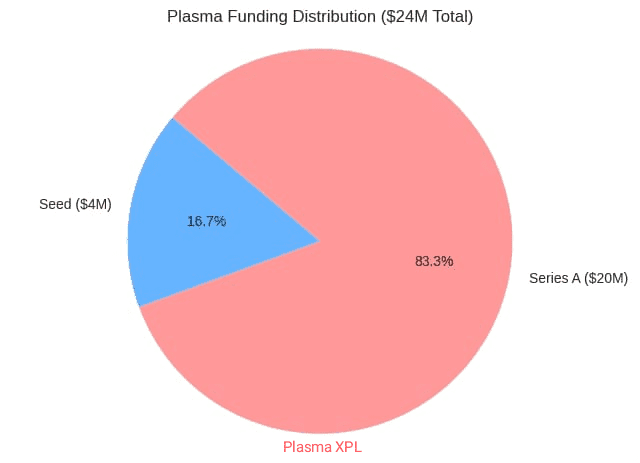

Jest też wyraźny wątek instytucjonalny. Infrastruktura płatności to nie tylko wyzwanie techniczne – to problem płynności i zaufania. Finansowanie Plasmy odzwierciedla tę rzeczywistość. W lutym 2025 roku Plasma ogłosiła pozyskanie 24 mln dolarów w ramach rund Seed i Series A, które prowadziły Framework Ventures i Bitfinex/USD₮0, z udziałem Cumberland (DRW), Flow Traders, IMC, Nomura, Bybit i innych, obok aniołów inwestycyjnych, w tym Paolo Ardoino i Petera Thiela. CoinDesk również relacjonował to pozyskanie, przytaczając 20 mln dolarów w rundzie Series A po 4 mln dolarów w rundzie seed.

To istotne, ponieważ płatności stablecoinów na dużą skalę wymagają głębokich szyn: animatorów rynku, integracji giełd, dostawców depozytów i partnerów, którzy priorytetowo traktują czas działania nad szumem.

Szerszy rynek wspiera tezę, że stablecoiny jako płatności nie są już niszą. Główne fintechy eksperymentują teraz ze stablecoinami wyraźnie w celu obniżenia kosztów transakcji międzynarodowych. Financial Times niedawno raportował, że Klarna uruchomiła stablecoina płatniczego (KlarnaUSD), aby poprawić efektywność międzynarodową – wyraźny dowód na to, że nawet duże fintechy konsumenckie postrzegają stablecoiny jako infrastrukturę, a nie spekulację. Gdy fintechy zaczynają przyjmować kryptograficzne szyny, zazwyczaj dzieje się to dlatego, że systemy dziedziczone są zbyt wolne i zbyt drogie dla nowoczesnego handlu.

Najłatwiejszym sposobem zrozumienia Plasmy jest normalny przypadek użycia: płacenie dostawcy za granicą, otrzymywanie dochodów od zagranicznego klienta lub wysyłanie pieniędzy do rodziny za granicą. Dzisiejsze opcje to wciąż kompromisy – przelewy bankowe są wolne i kosztowne, sieci kartowe nie obsługują bezpośrednich transferów, a usługi przekazów ukrywają opłaty w spreadach. Stablecoiny już rozwiązały problem ruchu cyfrowego dolara. To, co nie zostało w pełni rozwiązane, to sprawienie, aby to doświadczenie wydawało się naturalne, niezawodne i bezpieczne dla wszystkich, za każdym razem.

Jeśli Plasma odniesie sukces, nie będzie to dlatego, że uruchomiła następny gorący ekosystem DeFi. Będzie to dlatego, że cicho sprawi, że stablecoiny będą działać jak prawdziwe szyny pieniężne: szybkie rozliczenia, przewidywalne koszty, minimalne tarcie, łatwa integracja i niezawodność pod obciążeniem.

Dla traderów i inwestorów Plasma to zakład na konkretną wizję przyszłości kryptowalut – nie 'wszystko na łańcuchu', ale ruch pieniędzy na łańcuchu w skali. Potencjał jest jasny: jeśli stablecoiny nadal będą narzędziem płatniczym domyślnym, łańcuchy zaprojektowane wokół tego przepływu mogą stać się krytyczną infrastrukturą. Ryzyko jest równie jasne: płatności to brutalna arena, w której pozyskiwanie użytkowników jest kosztowne, zgodność jest nieunikniona, a zaufanie zdobywa się powoli.

Niemniej jednak, Plasma odzwierciedla bardziej dojrzałą fazę myślenia o kryptowalutach. Nie pyta, co jeszcze można tokenizować. Zadaje poważniejsze pytanie: jeśli stablecoiny są już globalnymi cyfrowymi dolarami, jak powinna wyglądać warstwa bazowa, gdy świat w końcu zacznie je tak traktować?