Expectations about interest rates from the Fed have changed quickly. Short-term bond yields are moving unpredictably, mainly because oil prices have jumped.

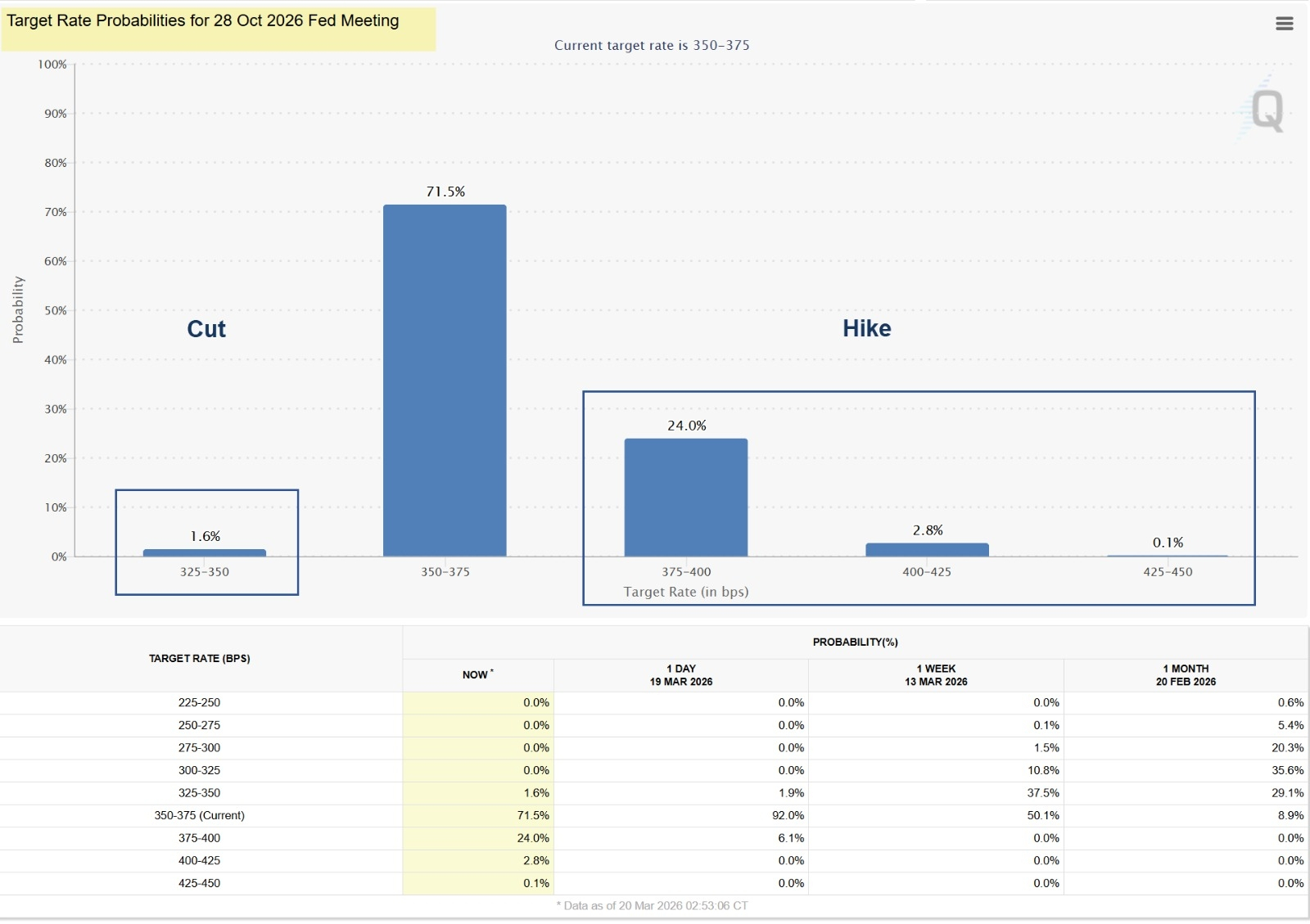

Right now, Fed funds futures show a 35% chance that interest rates will be raised by at least 0.25% after the October Fed meeting. Just one month ago, markets expected a 35% chance that rates would actually be cut by 0.50%.

The 2-year Treasury yield is now above 3.9%, its highest level since July. Back in July, yields dropped sharply due to weak job data, starting a steady decline that lasted about seven months. That drop has now been completely reversed after the recent tensions involving Iran.

Similar to what happened in 2022, the 2-year yield is no longer closely following the Fed’s expected rate path. Market strategist Seth Golden pointed out that traders are again increasing bets that the Fed may raise rates before the end of the year.

He also noted that in 2022, higher interest rates didn’t significantly hurt consumers because government support (like spending programs and tax measures) helped cushion the impact.

Looking ahead, Fed chair nominee Kevin Warsh is expected to support using other tools—beyond just changing interest rates—to control rising inflation risks.

At the same time, Christian Fromhertz highlighted that the MOVE index (often called the “VIX for bonds”) is rising sharply.

A higher MOVE index means there is more uncertainty about where interest rates are heading. Historically, this kind of uncertainty often comes before bigger swings in financial markets.

Large spikes in the MOVE index can also signal potential increases in stock market volatility and possible declines in equities.