I’ve been digging into the retail CBDC section of SIGN’s docs for the past couple of days, and honestly, the privacy model is the part I keep circling back to 😂

At first glance, it’s actually more advanced than most people give it credit for.

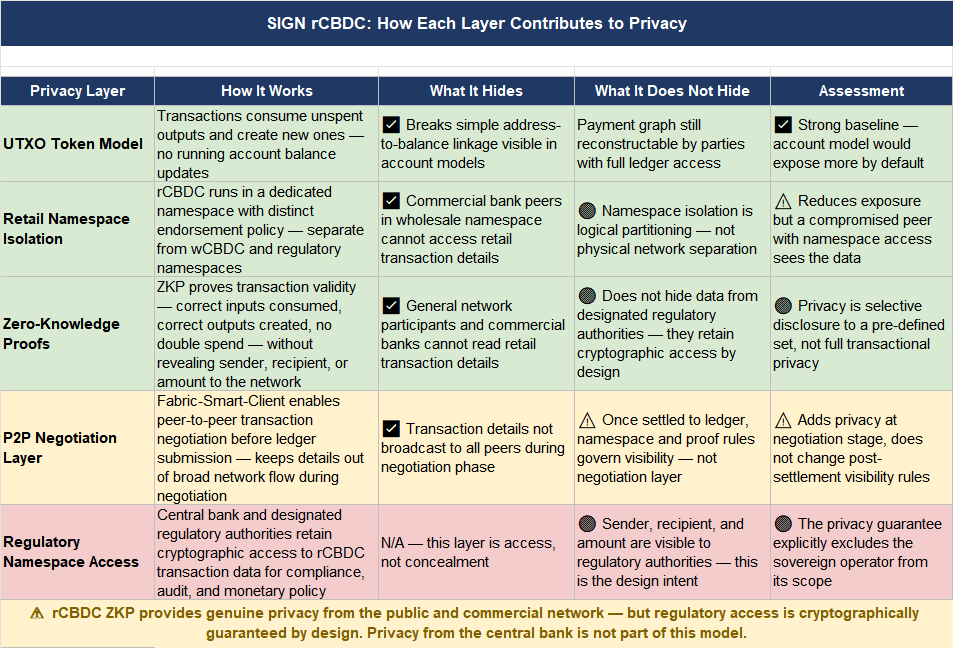

Retail transactions run on a private rail built on Hyperledger Fabric, inside their own isolated namespace. They’re using a UTXO model instead of the usual account-based system, which already changes how traceability works. Instead of balances updating in place, transactions consume and create outputs, making it harder to link activity in a simple, linear way.

Then you layer in Zero-Knowledge Proofs.

So now, a transaction can be verified as valid — no double spends, correct inputs and outputs — without exposing identities or amounts to the broader network. Add the peer-to-peer negotiation layer (via Fabric Smart Client), and a lot of the transaction detail never even hits shared infrastructure in the first place.

Up to this point, it sounds like a genuinely strong privacy architecture. And to be fair, it is.

But there’s one line in the whitepaper that completely changes how I interpret all of this.

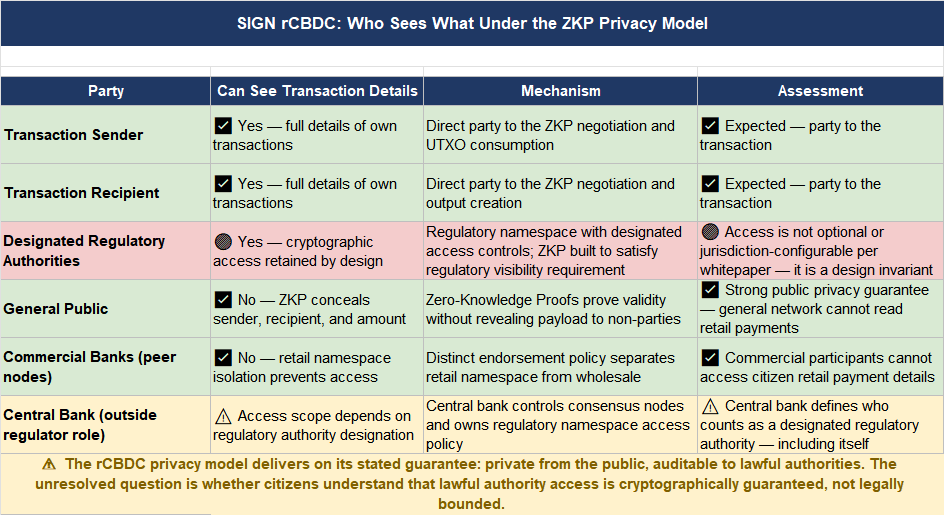

It says transaction details are visible only to:

the sender

the recipient

designated regulatory authorities

That third party isn’t optional. It’s not configurable. It’s built into the system itself.

Which means this isn’t full privacy in the way most people think about it.

What the system is really doing is selective disclosure. The ZKP layer isn’t just hiding data — it’s also designed to reveal that same data to a specific, predefined entity. Regulators don’t need to “break” anything to see transactions. They’re meant to see them.

And from a design perspective, I actually think that’s the honest way to do it.

If a sovereign CBDC is going to include regulatory oversight (and realistically, it always will), embedding that access directly into the cryptographic layer is cleaner than pretending privacy exists and then adding surveillance somewhere else.

But it does create a gap between perception and reality.

For everyday users, this system does provide real privacy — from the public, from other participants, even from commercial banks on the network.

But not from the central authority.

And that’s not a bug. That’s the feature.

So now I’m stuck somewhere in between two interpretations:

Is this a meaningful step forward for financial privacy in government systems?

Or is it a highly refined compliance architecture that uses the language of privacy, while still ensuring the one entity that matters most can see everything?

Not saying it’s good or bad just that it’s worth understanding clearly.

Anyway… I’ve spent way too long on this + watching $LYN and $RIVER charts. Brain is officially done for today 😅

@SignOfficial $SIGN #signDigitalSovereignlnfra