Yesterday night right after watching the latest monthly unlock settle and the March snapshot window quietly close, I found myself reopening my Sign notes instead of logging off. It was nat hype that pulled me back in it was timing. The kind of timing mismatch that shows up when narrative starts moving faster than infrastructure.

I keep replaying October 2025 in my head that moment where @SignOfficial CEO was sitting across from Kyrgyzstan’s Deputy Central Bank Governor with Changpeng Zhao in the room. That was not a staged conference appearance or a speculative partnership announcement, it was a technical service agreement tied to the Digital Som. Then November follows with Sierra Leone signing a formal MoU for national digital identity and stablecoin rails. For a company founded in 2021, that kind of sovereign-level access is not normal it signals capital credibility, and very intentional positioning.

But every time I shift from the narrative layer into verifiable state, I hit the sam silence. There’s still no independently traceable on-chain citizen credential issuance tied to Sierra Leone, no observable stablecoin transaction flow connected to a government rollout, and no public interface wher a third party can actually track live usage. That gap between signed paper and live infrastructure is where my attention keeps locking in, because it’s the only place where the story either holds or breaks.

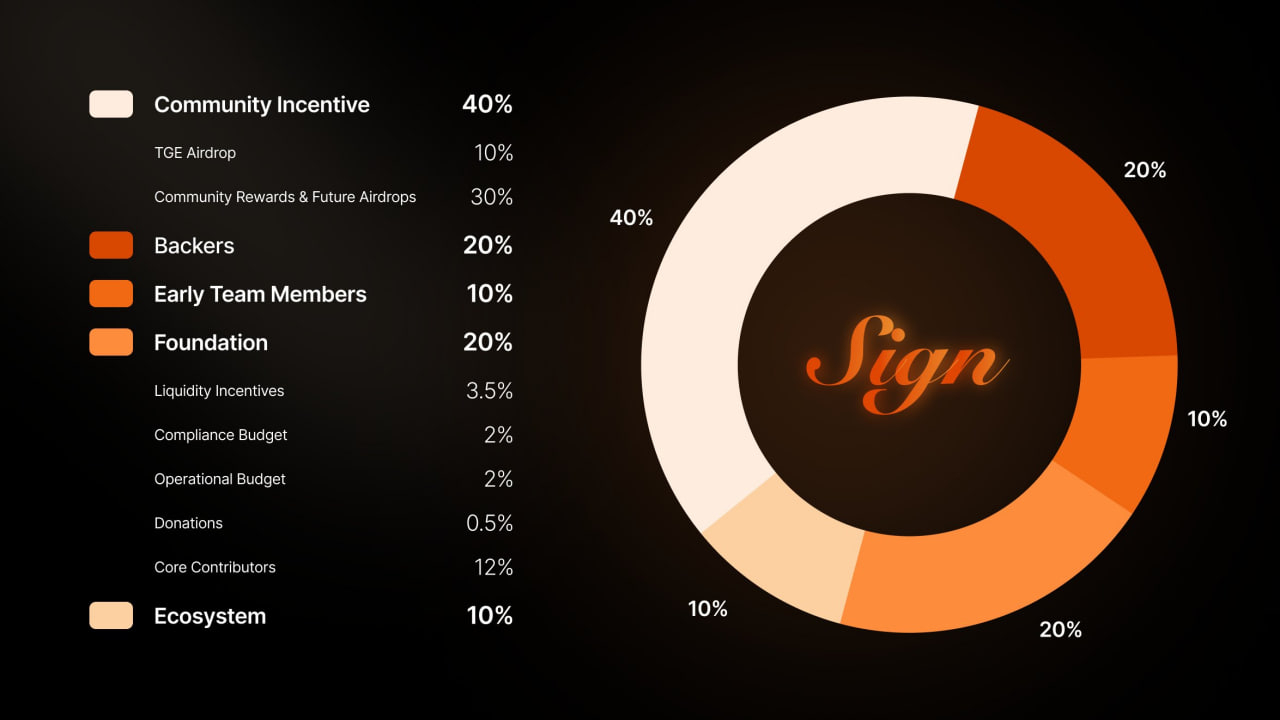

While tracing recent flows I kept noticing a recurring pattern tied to treasury-linked wallets, one of them starting with 0x7a3 and consistently distributing outward around unlock windows. The nombers line up almost too cleanly, roughly 96.6 million SIGN entering circulation per cycle, with gas activity clustering around those distribution moments rather than organic usage. The chain is active, but it’s active because of supply mechanics, not because a citizen somewhere just used a government-issued credential or completed a payment inside a national system. That distinction changes how I read everything.

Around 3:05 AM I tried to simulate what a real deployment would actually look like from the outside, something simple like tracking a state transition from an unverified identity to a verified on-chain credential under a national registry. I wasn’t debugging a failure or dealing with a stuck transaction, I was dealing with absence. No contract emitting identity-linked evints, no public endpoint, no observable flow to map. That was the moment I paused, because technically the architecture Sign promotes should already be capable of exposing at least fragments of that process if anything meaningful were live.

What keeps me engaged is how the system is designed to loop across layers rather than stack neatly. The economic layer is already in motion, with circulating suply expanding and the market implicitly pricing in future sovereign demand. The technical layer is arguably the strongest part of the design, especially the dual-chain approach that separates public verification from private execution, which aligns almost perfectly with how governments think about transparency versus control. Then there’s the identity and governance layer, which is the actual unlock for everything else, because without real citizens being issued credentials, nothing else compounds. Right now that loop isn’t closed, because identity hasn’t translated into usage, usage hasn’t created demand, and demand hasn’t absorbed supply.

When I compare this structure to something like Fetch.ai or Bittensor, the difference becomes even sharper in my mind. Those ecosystems grow from the bottom up, developers and contributors creating activity that gradually scales. Sign is attempting the opposite, a top-down integration where entire national systems plug in at once. It’s slower, heavier, and far more dependent on political timelines, but if it works, it operates at a completely different magnitude.

The honest part I keep returning to is that MoUs are not deployment, pilot programs are not adoption, and access is not execution. Even in the most advanced case, Kyrgyzstan’s timeline stretches well into late 2026 for a decision point, with potential full rollout in 2027. That’s a long latency curve, yet the market behavior I’m observing feels like parts of that future have already been priced into the present.

That’s where the structural tension sits for me. Early capital can absorb time because their positioning was built before the narrative accelerated, but anyone entering on the back of sovereign adoption headlines is exposed to a very different reality, one where supply continues expanding on a fixed schedule while real usage is still waiting for political and technical alignment. Time, in this case, isn’t neutral, it’s a cost that accumulates quietly.

I’m not dismissing Sign, if anything I think the architecture is one of the more grounded attempts at solving a real-world problem that governments actually have. The access they hve secured is difficult to fake, and the design choices reflect an understanding of how state systems operate. But inevitability doesn’t mean immediacy, and that’s the tension I’m still sitting with.

The question that keeps looping in my head is whether, when this finally does go live at scale, it will even feel like a crypto system at all, or if it will dissolve so completely into national infrastructure that the human layer using it wont realize blockchain was ever part of the equation.