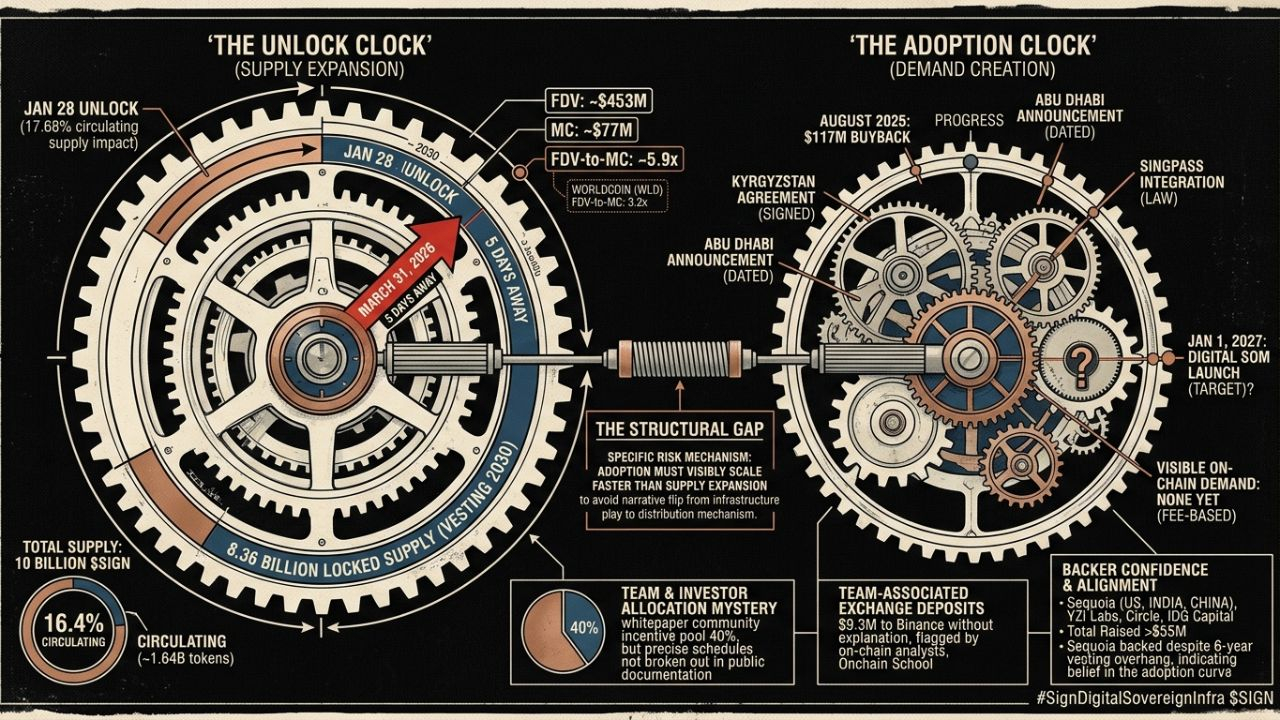

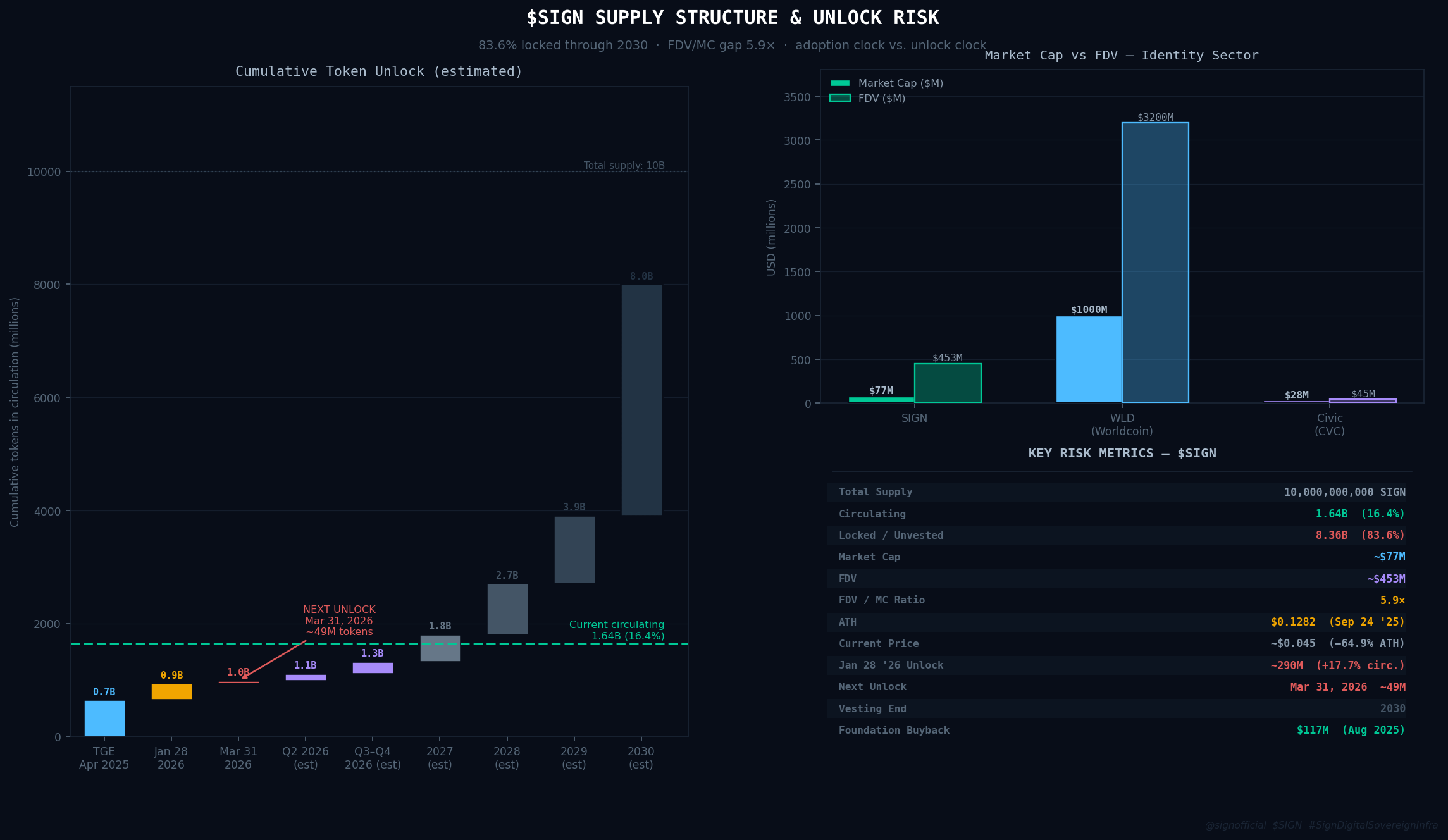

I pulled up the unlock calendar for $SIGN around 11 PM last Tuesday and the number that hit me first wasn't the amount — it was the timing. March 31, 2026. Five days away. The January 28 unlock had already gone through: roughly $11.6 million worth of tokens, representing about 17.68% of the circulating supply at that point. The market absorbed it without drama. But that event was followed quietly by a $9.3 million worth of SIGN moving from team-associated addresses to Binance in early 2026 — flagged by on-chain analysts and picked up by Onchain School, circulated through crypto Twitter with the predictable split: half saw normal treasury operations, half saw the team selling into strength after March's 100%+ move.

I spent the next hour going through the supply structure properly rather than assuming.

the numbers that sit with me

@SignOfficial 's total supply is 10 billion $SIGN. Of that, 16.4% — roughly 1.64 billion tokens — is currently circulating. The remaining 8.36 billion are locked under a vesting schedule that runs through 2030. The market cap at ~$0.045 sits around $77 million. The fully diluted valuation is approximately $453 million. That FDV-to-MC ratio of 5.9x means that if all locked tokens were circulating at today's price, the total value of the network would be nearly six times what the market is currently pricing. Every unlock event between now and 2030 is a potential supply event.

For comparison: Worldcoin (WLD) — the closest comparable in the identity and attestation space by ambition — has roughly 31% of its 10 billion supply circulating as of late March 2026, with a market cap around $1 billion and a fully diluted valuation near $3.2 billion. WLD's FDV-to-MC ratio is roughly 3.2x, and a 52%-of-supply unlock event is scheduled for July 2026. Both projects have significant supply overhangs. Sign's is proportionally larger right now.

The team allocation question is the one I couldn't fully resolve from public docs. The whitepaper describes the community incentive pool as 40% of total supply — 4 billion tokens — dedicated to ecosystem growth, user acquisition, and long-term incentives. But the specific vesting schedules for investor allocations, team allocations, and the foundation reserve aren't broken out in public-facing documentation at the level of precision that would let me calculate sell pressure per quarter with confidence. The Jan 28 unlock documentation referenced a 17.68% circulating supply impact, which implies approximately 290 million tokens entered circulation in a single event. That's meaningful for a token where total circulating supply was roughly 1.64 billion before the event.

the risk I can name precisely

The structural problem with low-float, high-FDV tokens isn't that unlocks are inherently bearish. It's that adoption has to visibly scale faster than supply expansion to avoid the narrative flipping from "sovereign infrastructure play" to "distribution mechanism for early investors." Sign's advantage is that the adoption pipeline is genuinely real — the Kyrgyzstan technical service agreement is signed, the Abu Dhabi announcement is dated, the Singpass integration is under actual law. The disadvantage is that none of these partnerships generate visible, on-chain, fee-based demand for $SIGN tokens on a schedule that clearly competes with unlock cadence through 2027.

The $117 million buyback in August 2025 was the clearest signal that the foundation is aware of this dynamic and willing to use treasury resources to manage it. But buybacks absorb circulating supply, not future unlock supply. The $9.3M exchange deposit from team-associated addresses without accompanying documentation is a harder thing to contextualize — not because it's necessarily sell pressure, but because a project whose core thesis is verifiable trust and transparent attestation should be able to explain its own token movements without the community having to infer from on-chain analytics.

still working out the long game

The case for watching despite all of this comes back to something that's easy to underweight. Sequoia Capital invested across all three branches — US, India, China — alongside YZi Labs (twice), Circle, and IDG Capital. The total raised exceeds $55 million. Sequoia doesn't typically back infrastructure plays with a six-year vesting overhang unless they believe the adoption curve justifies it. That doesn't make the token economics clean. It does mean the people with the most information about Sign's sovereign deployment pipeline chose to stay exposed.

The Kyrgyzstan central bank decision on full Digital SOM issuance is scheduled for end of 2026. If the Digital SOM goes live at national scale for 7.2 million citizens on January 1, 2027 as targeted, the demand-side story for SIGN changes materially. If it doesn't — or if the adoption timeline slips — the supply schedule doesn't.

That gap between the adoption clock and the unlock clock is the actual risk to watch. Not "crypto is volatile." The specific mechanism is: 83.6% of supply unlocking through 2030 while sovereign deployments are still proving out at scale. Whether the adoption story stays ahead of that schedule is what I'm still working through.