The Middle East is sitting on one of the largest concentrations of sovereign capital the world has ever seen — and quietly, a big part of it is still moving through systems that were never designed for this scale. #Sign @SignOfficial $SIGN

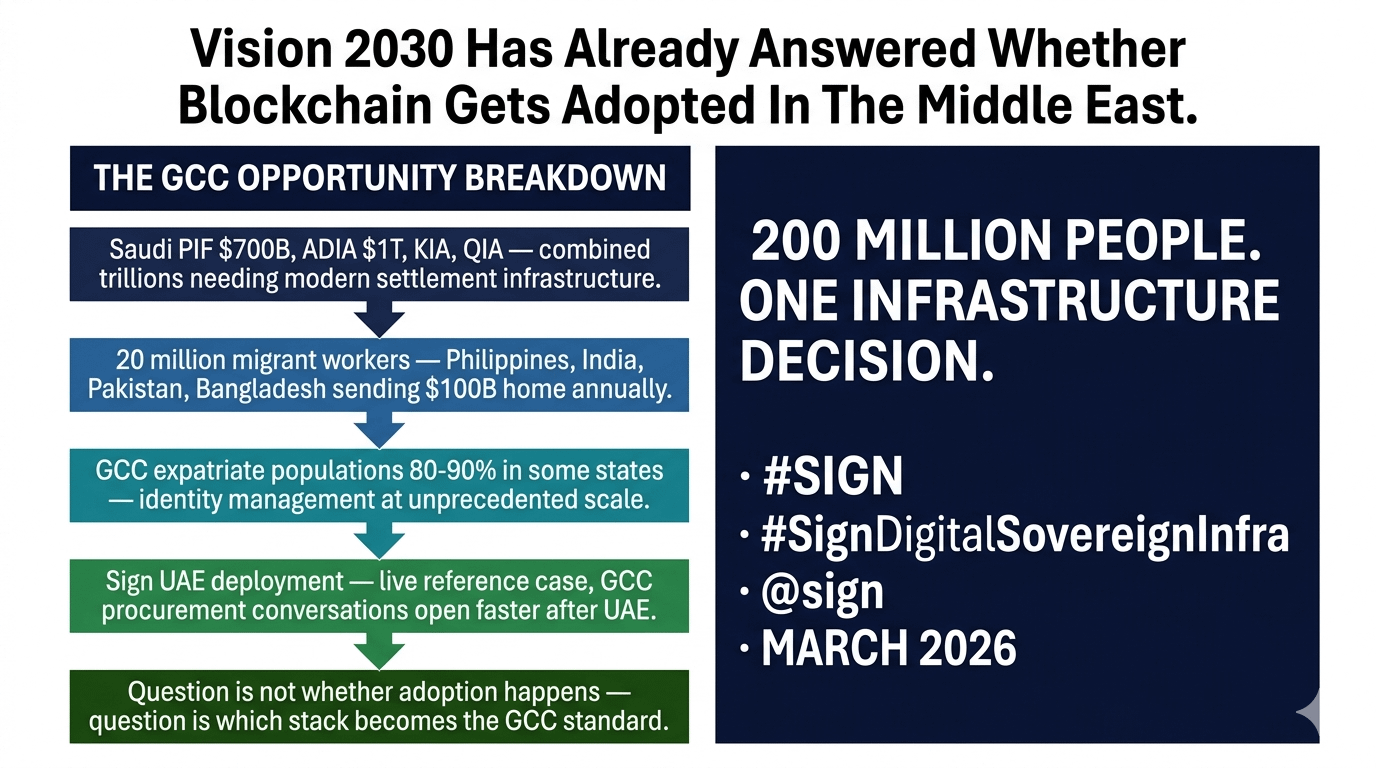

Saudi Arabia’s Public Investment Fund alone manages assets in the range of $700 billion. Abu Dhabi goes even further, with well over $1 trillion under management. Then you have Kuwait, Qatar, and other sovereign entities across the GCC — and when you step back and look at the full picture, you’re not talking about billions anymore. You’re looking at trillions of dollars that need to move across borders, settle efficiently, and remain both transparent and private at the same time.

That’s where the real issue begins.

Because despite how advanced these economies are becoming, the infrastructure moving this capital is still largely built on correspondent banking — a system designed decades ago, for a completely different financial world. Back then, volumes were lower, compliance was simpler, and speed wasn’t the defining factor it is today.

Now, it is.

Today, moving capital across borders can still take days. Fees quietly stack up at every layer. And every new jurisdiction introduces another round of KYC and AML checks — often repeating the same verification processes again and again. It’s not just inefficient, it actively slows down how quickly capital can be deployed.

And when you’re dealing with sovereign-scale investments, delays aren’t small problems. They’re structural limitations.

This isn’t something that might become an issue in the future. It’s already happening. Every major sovereign fund in the region is dealing with these friction points right now — whether it’s settlement delays, compliance duplication, or the constant balance between transparency and confidentiality.

What’s interesting is that the Middle East isn’t ignoring this.

In fact, it’s one of the few regions where the intent, the capital, and the urgency are all aligned at the same time.

Take Saudi Arabia’s Vision 2030. This isn’t just a high-level ambition — it’s a fully funded transformation plan with clear timelines. Digital infrastructure sits right at the center of it. Government services are being digitized. Identity systems are being rethought. Financial rails are being modernized.

And importantly — these aren’t optional upgrades. They’re mandates.

Which means the conversation is no longer about if the system evolves. It’s about how fast it happens and who builds the foundation.

Now layer in another major piece of the puzzle — remittances.

The GCC is home to more than 20 million migrant workers. Every year, they send money back to countries across South Asia, Southeast Asia, and parts of Africa. In total, those flows exceed $100 billion annually.

But here’s the part most people overlook — a noticeable percentage of that money is lost in the process. Transfer fees, currency spreads, intermediary costs — they all add up. In many cases, workers lose anywhere between 5% to 10% of their earnings just to move money home.

Over time, that’s not a small number. That’s billions quietly drained from the people who can least afford it.

A more modern financial rail — especially one backed by government-level infrastructure — could change that completely. Lower costs, faster settlement, and better visibility for regulators. Not just more efficient, but more fair.

Then there’s identity — another layer that doesn’t get enough attention, but arguably matters just as much.

Several GCC countries rely heavily on expatriate populations. In some cases, expats make up 80% to 90% of the total population. Managing identity, residency status, work permits, and access rights at that scale is not a simple task.

Most of it still relies on fragmented systems — a mix of legacy databases, manual processes, and isolated government platforms that don’t communicate seamlessly with each other.

The result?

Redundancy, delays, and administrative overhead that grows with the population.

Now imagine replacing that with a system where identity is verifiable, portable, and instantly accessible — where credentials like residency status, employment authorization, or professional licenses can be confirmed across borders without repeated checks.

That’s not just a technical upgrade. That’s a fundamental shift in how governments interact with people.

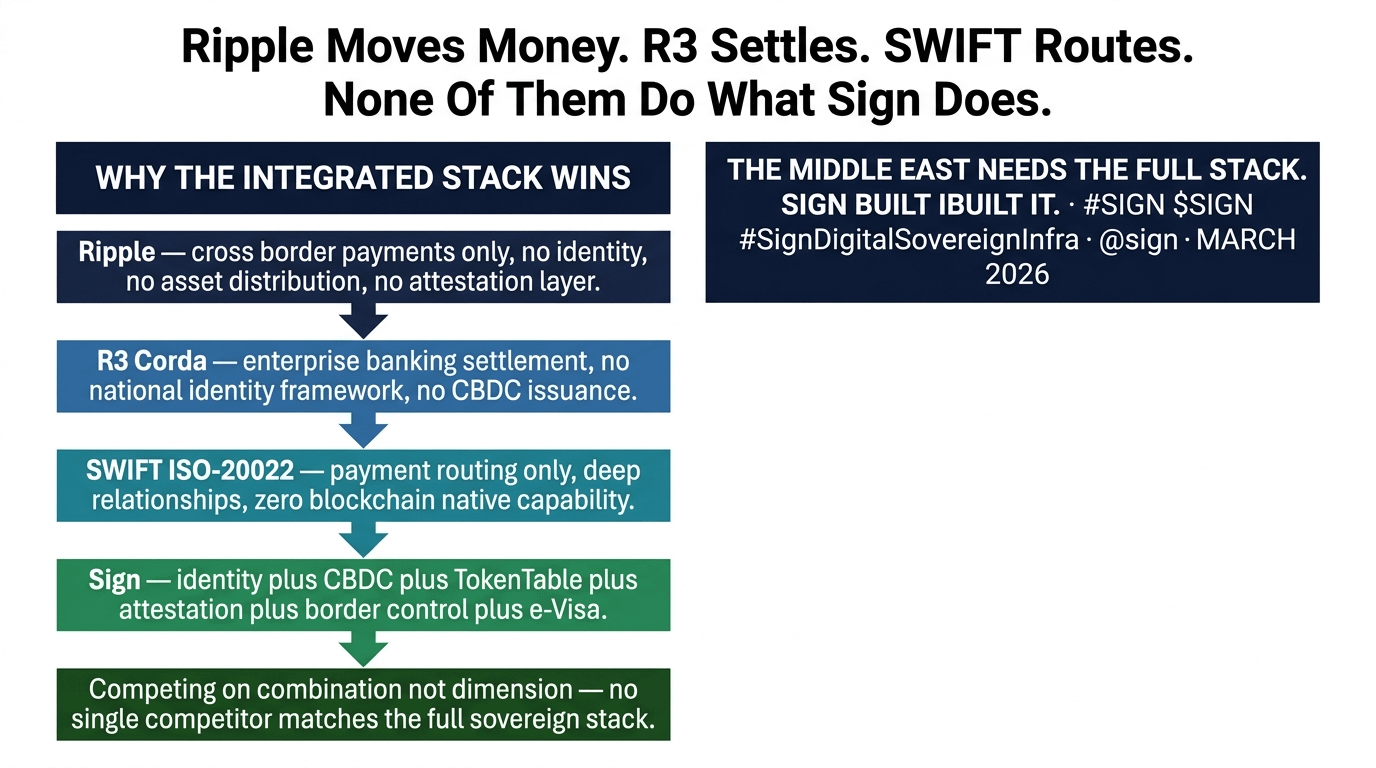

This is exactly where something like Sign starts to stand out.

Because it’s not approaching the problem from just one angle.

Most existing players in the space tend to specialize. Some focus on payments. Others on settlement. A few on messaging or compliance layers. But rarely do they bring everything together into a single, unified framework.

Sign’s positioning is different.

It’s not just about moving money faster. It’s about building an infrastructure layer where identity, payments, credentials, and compliance can all exist together — and actually work together.

And the fact that it’s already deployed in the UAE matters more than it might seem at first.

In the GCC, real-world implementation carries weight. When one country adopts a system and it proves effective, others don’t ignore it. They watch closely. They evaluate. And if it aligns with their own strategic direction, decisions tend to move faster.

That creates a kind of regional momentum.

A live deployment isn’t just a technical milestone — it becomes a signal.

It tells neighboring governments that the system isn’t theoretical. It works. It scales. And it can be integrated into real-world operations.

That kind of validation is hard to replicate, especially in a region where trust and execution matter as much as innovation.

Of course, this space isn’t empty.

There are serious players already active in the region. Ripple has been building relationships with central banks. R3 has strong ties within enterprise banking networks. SWIFT, with its ISO 20022 transition, still holds deep institutional connections across global finance.

These aren’t small competitors. They have history, infrastructure, and influence.

But they’re also built around specific functions.

Payments. Settlement. Messaging.

What they don’t offer — at least not in a fully unified way — is a complete sovereign infrastructure stack that connects identity, assets, compliance, and programmability into one system.

And that’s where the difference becomes clear.

Because the next phase of financial infrastructure isn’t just about faster transactions. It’s about interconnected systems — where identity informs payments, where compliance is embedded, and where assets can move with logic attached to them.

It’s a different way of thinking.

And the region is ready for it.

So the real question isn’t whether the Middle East will adopt new infrastructure. That part is already in motion.

The real question is which system becomes the standard.

Which platform ends up powering identity verification, cross-border payments, government services, and digital assets for hundreds of millions of people across the GCC and beyond.

Because once a standard is set at that level, it doesn’t just stay local. It expands.

And early positioning matters more than anything.

Right now, Sign has something that’s difficult to ignore — it’s already in the field.

Not in theory. Not in testing.

Live.

And in a region like the Middle East, that kind of head start doesn’t just give you an advantage.

It shapes the direction of everything that comes next. 🔥