For a long time I've wondered why governments kept building digital payment infrastructure and getting it wrong in the same two ways. Either they built something fully centralized and operationally strong but geopolitically brittle — dependent on a single technology vendor, a single jurisdiction's legal framework, or a single payment rail that competitors or adversaries could cut off. Or they looked at permissionless blockchain and correctly identified that no government procurement office was signing off on infrastructure that a pseudonymous validator set could exit or fork. The gap between "digitize the currency" and "do it in a way that's actually sovereign" has been real and largely unsolved. And perhaps @SignOfficial has identified the specific moment in 2024-2025 when the two sides of that gap became close enough to bridge.

The two failure modes, named

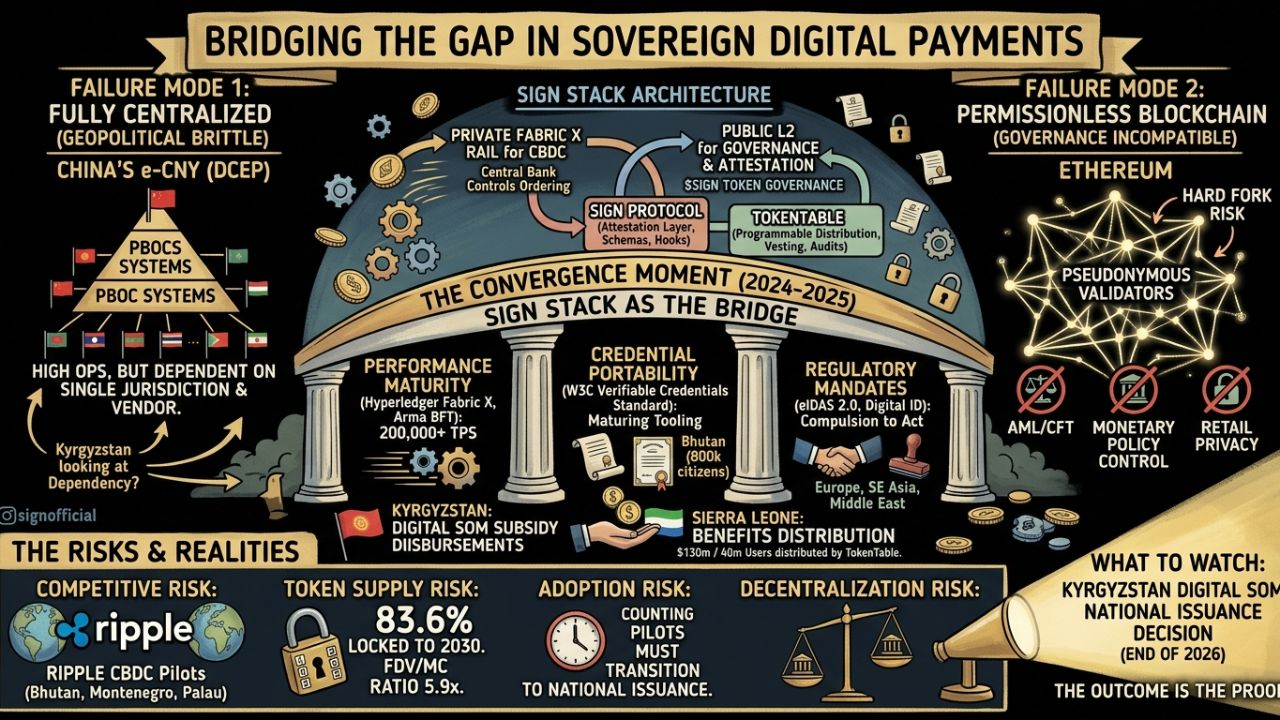

China's digital yuan — the e-CNY, DCEP — is the most advanced central bank digital currency in operational deployment globally. Over 7 trillion yuan in transactions by late 2024, 950 million wallets registered, live in over 26 provinces. The operational execution is genuinely impressive. But the e-CNY is PBOC infrastructure, running on PBOC systems, under PBOC governance, with zero portability to external verification frameworks and no interoperability with heterogeneous credential systems outside China's state apparatus. Kyrgyzstan looking at e-CNY as a model isn't looking at sovereignty — it's looking at a different dependency.

Ethereum goes to the other extreme. Genuinely decentralized, censorship-resistant, open to any verifier anywhere. The transparency and decentralization that make Ethereum trustworthy also make it incompatible with the requirements of a central bank digital currency: programmable monetary policy, supervisory access for AML/CFT compliance, privacy for retail transactions that doesn't expose every citizen's payment history to the public, and governance that doesn't require a hard fork to change monetary parameters. No government CTO has cleared Ethereum mainnet for national payment infrastructure. The properties that make it credible to the crypto community are the properties that disqualify it from the procurement process.

what changed in 2024 that makes Sign's moment real

Three things converged that didn't exist simultaneously before. First: Hyperledger Fabric X and Arma BFT reached production-ready maturity in 2025, giving a permissioned blockchain stack the throughput characteristics (200,000+ TPS in benchmarks) that sovereign financial infrastructure requires. The performance gap between "blockchain" and "existing payment rails" became narrow enough that procurement teams stopped treating it as disqualifying. Second: the W3C Verifiable Credentials standard reached Recommendation status with enough tooling maturity that governments could actually implement the credential portability layer without starting from scratch. Bhutan proved it with 800,000 citizens. Third: regulatory pressure from eIDAS 2.0 in Europe and analogous national digital ID mandates across Southeast Asia, the Middle East, and Sub-Saharan Africa created a market where the question shifted from "should governments digitize identity and payments" to "which infrastructure stack should they use."

Sign's SIGN Stack — Sign Protocol for attestation and DID, TokenTable for programmable distribution, and a dual sovereign chain architecture (public L2 for governance and attestation, private Fabric X rail for CBDC) — is positioned precisely at the intersection of these three things. It doesn't ask governments to adopt permissionless infrastructure. It doesn't ask them to give up operational control. It asks them to adopt a standards-compliant, auditable, cryptographically sound infrastructure that preserves sovereignty while enabling portability. That's a genuinely different pitch than anything the crypto space was making in 2018.

the mechanism, developer tooling, and use cases

Sign Protocol's attestation layer uses an omnichain design — attestations issued on one network are portable and verifiable across EVM chains, Solana, and TON without re-issuance. The Schema Hook system lets issuers define programmable conditions: a credential only validates if the attesting party's reputation score exceeds a threshold, or the credential automatically revokes if the issuing organization loses accreditation. For a government issuing subsidy eligibility credentials to millions of citizens, that programmability is the difference between a static document and a live, machine-enforced policy.

TokenTable — already used to distribute $130 million across 40 million users before $SIGN 's own TGE — handles the distribution mechanics that sovereign programs require: vesting schedules, conditional claims, delegated claiming, and audit trails. The same engine that manages token distribution for web3 projects is being proposed as the infrastructure for Digital SOM subsidy disbursements in Kyrgyzstan and benefit distribution in Sierra Leone.

CEO Xin Yan brings a hardware engineering and crypto VC background — unusual combination for a project building at the intersection of government procurement and protocol design, and probably the right one. CTO Jack Xu's academic work in blockchain at USC gives the team institutional credibility with the government CTO conversations that close sovereign deals. The investor stack — Sequoia across three branches, YZi Labs (twice), Circle, IDG Capital — provides access to institutional networks in the jurisdictions Sign is targeting.

the risk section, honest

Competitive risk is real and specific. Ripple's CBDC platform is in live pilots with the central banks of Bhutan, Montenegro, and Palau — not MOUs, actual pilots. Ripple has 15 years of institutional relationship-building in the correspondent banking world and a legal team that has been through regulatory combat in the US. Sign doesn't have that institutional history. The sovereign deployment pipeline is promising; the competitive moat is still being established.

Token supply risk is the one I keep coming back to. 83.6% of $SIGN is locked through 2030. FDV of $453 million against a market cap of $77 million produces a 5.9× ratio that implies either significant price appreciation is priced into the unlock schedule or significant sell pressure is waiting. The March 31, 2026 unlock of ~49 million tokens is the near-term test. The August 2025 buyback ($117 million worth of $SIGN) shows the foundation is willing to manage supply, but buybacks don't reduce future unlock obligations.

Adoption risk is the subtlest one. Sign's sovereign thesis requires that governments who sign technical service agreements actually deploy the infrastructure at national scale. The Kyrgyzstan Digital SOM pilot is real. The decision point for full national issuance is end of 2026. A government that pilots and then doesn't deploy is a different outcome from the one the current narrative prices in.

Decentralization timeline risk: the private CBDC rail that carries Sign's highest-value sovereign deployments is permissioned by design. The central bank controls the ordering layer. $SIGN governance rights extend to the public protocol — not to the private rails where national payment infrastructure runs. That separation is architecturally honest, but it means the token's governance utility is bounded by what the public layer actually does.

what I'm watching

Sign's thesis will be tested most concretely by the Kyrgyzstan Digital SOM decision at end of 2026. If the central bank confirms full national issuance for January 1, 2027, that's the first live proof of sovereign blockchain deployment at population scale under a technical service agreement that was signed in public. If it slips — not because the technology failed, but because procurement, political, or operational complexity extended the timeline — the narrative around Sign's deployment cadence changes materially.

That decision is what I'm actually waiting for. Everything before it is evidence about the probability. The outcome itself is the proof.

#SignDigitalSovereignInfra