1.4 billion people still don’t have a bank account.

Most people assume the reason is simple — banks haven’t reached them yet.

Rural areas, weak infrastructure, limited branches, high fees.

That’s true.

But it’s not the full story.

The real reason is deeper.

And honestly, a bit uncomfortable.

Banks don’t exclude people because they are poor.

They exclude people who cannot prove who they are. #Sign @SignOfficial $SIGN

This Isn’t an Access Problem — It’s an Identity Problem

When we talk about financial inclusion, the focus is almost always on access.

Build more branches.

Expand mobile banking.

Lower the cost of services.

The assumption is that once financial systems reach people, the problem will solve itself.

But reality doesn’t work that way.

The system already exists.

Banks already exist.

Financial infrastructure is already in place.

The reason people remain outside the system isn’t because it hasn’t reached them —

it’s because they cannot enter it.

And there is only one gate:

Identity.

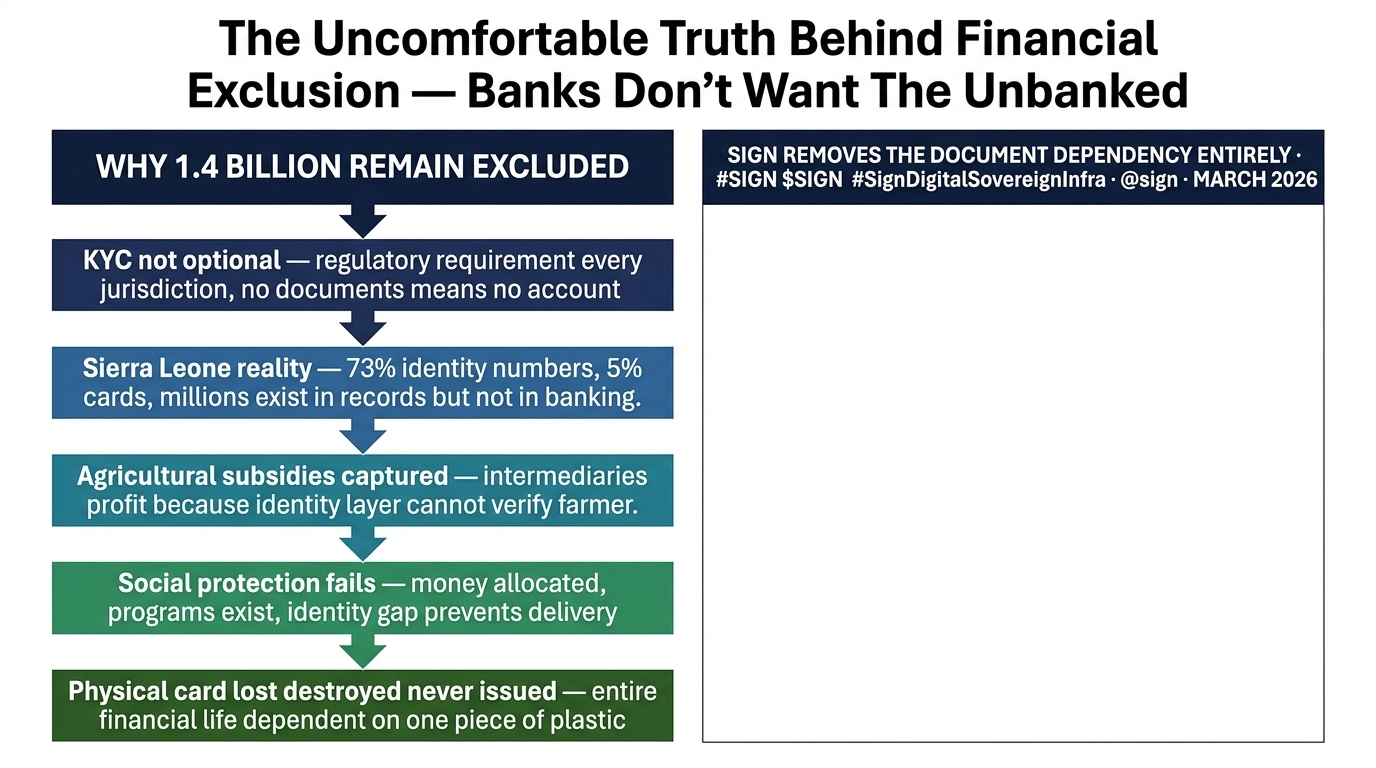

KYC — The Gatekeeper of the Financial System

In the formal financial world, one rule is non-negotiable:

KYC — Know Your Customer.

Every regulated institution, in every country, must verify identity before offering financial services.

That usually means:

A government-issued ID

Proof of address

A tax identification number

Sometimes even income verification

And this is where the problem begins.

Hundreds of millions of people simply don’t have these documents.

No registered address.

No formal paperwork.

No physical ID.

So the system responds in the only way it knows how:

No documents = No access.

It doesn’t matter how honest or hardworking someone is.

If they cannot prove their identity, they are locked out.

The Data Tells a Clear Story

According to the World Bank’s Findex database,

the biggest barrier for unbanked adults is not distance from a bank.

It’s the lack of documentation.

That’s the silent filter —

the invisible wall that keeps people out of the formal economy.

Sierra Leone — A Real-World Example

Take Sierra Leone as an example:

73% of people have an identity number

Only 5% have a physical ID card

Think about that gap.

Millions of people exist in government records.

They are counted. They are recognized.

But when they walk into a bank,

they cannot prove it.

Because they lack physical proof.

That gap isn’t just statistical.

It represents real exclusion.

When Identity Fails, Everything Else Breaks

This problem goes far beyond banking.

Government subsidies fail to reach the right people

Welfare programs leak or get misallocated

Intermediaries exploit the system

Funds never reach those who actually need them

The issue is rarely a lack of money.

The issue is verification.

If a system cannot confirm who someone is,

it cannot serve them effectively.

So What’s the Solution?

If identity is the problem,

then identity has to be the solution.

But not the traditional kind —

the one tied to plastic cards and paper documents.

Because that’s exactly where the system breaks.

The answer is:

Digital, verifiable, portable identity.

Where the Shift Begins

Imagine identity not tied to a physical document.

Imagine this instead:

A simple biometric scan.

Converted into a cryptographic proof.

No paper.

No physical dependency.

No repeated verification.

Just a secure, verifiable identity that works anywhere.

This isn’t theoretical anymore.

It’s already possible.

A Different Approach to Identity

This is where frameworks like Sign come in.

The idea is simple, but powerful:

Remove identity’s dependence on physical documents.

A person registers using whatever they have available:

A biometric scan

An existing identity number

Government validation

Or even a trusted witness

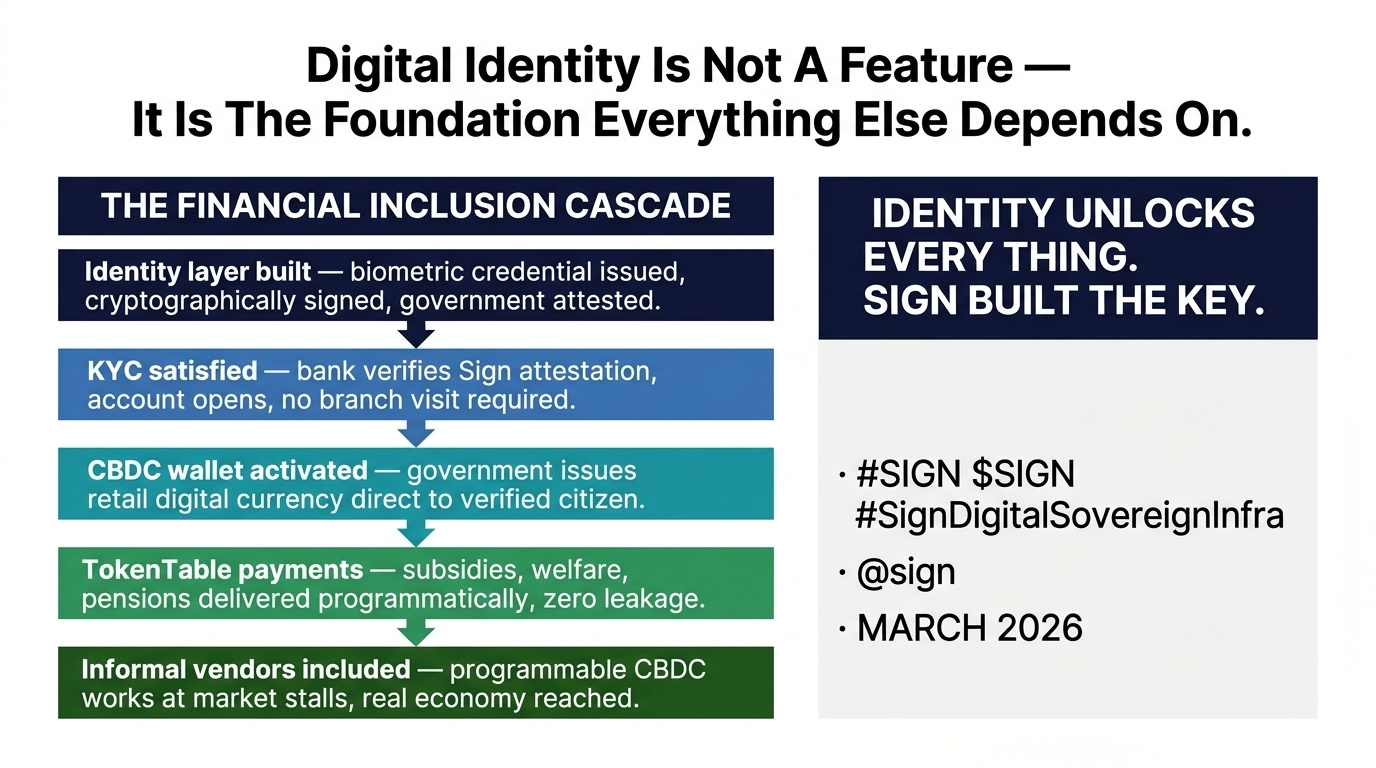

From that, the system issues a cryptographically signed digital credential.

This credential is:

Tamper-proof

Instantly verifiable

Globally usable

And most importantly:

It doesn’t rely on a physical card.

KYC — Reinvented

In the traditional system:

Documents → Verification → Approval

In the new model:

Digital identity → Cryptographic proof → Instant verification

A user presents their identity.

A bank verifies the proof.

The account opens.

No paperwork.

No branch visit.

No repeated checks.

Financial Access Finally Unlocks

Once identity is solved, everything else follows.

Bank accounts

Credit access

Insurance

Savings tools

People who were previously invisible to the system

suddenly become part of it.

The Role of CBDCs

Now add another layer:

Central Bank Digital Currencies (CBDCs).

Traditional banking comes with heavy infrastructure:

Physical branches

Regulatory overhead

High operating costs

This is why low-income and rural populations are often ignored —

serving them isn’t profitable.

CBDCs change that completely.

Governments can issue digital currency directly to individuals.

No bank account needed.

No branch required.

No minimum balance.

Just a verified identity and a digital wallet.

Programmability — The Real Advantage

This isn’t just digital money.

It’s programmable money.

That means:

Government payments can be targeted

Funds can be restricted to specific uses

Transactions can be tracked transparently

Leakage drops.

Efficiency increases.

Including the Informal Economy

Here’s something most systems ignore:

Low-income populations don’t rely on formal retail systems.

They rely on local vendors and informal markets.

Traditional banking struggles to include these participants.

But with digital identity and programmable payments:

Both parties can verify themselves

Transactions can happen directly

No POS machine needed.

No bank account required.

Just identity.

The Real Challenge — Devices

Of course, no system is perfect.

There’s still one real barrier:

Access to devices.

Digital identity requires a smartphone or similar device.

And in many underserved regions,

financial exclusion overlaps with limited access to technology.

Progress, Not Perfection

Solutions are already emerging:

QR-based identity sharing

NFC-enabled verification

Offline credential systems

These reduce dependency on constant connectivity

but don’t eliminate it entirely.

Still, it’s a step forward.

The Bigger Picture

When you zoom out, one thing becomes clear:

The infrastructure to include 1.4 billion people already exists.

Banks exist.

Money exists.

Systems exist.

The missing layer was always identity.

And That Layer Is Finally Being Built

Once identity works:

Financial inclusion becomes real

Government systems become efficient

Economic participation expands

This isn’t just about opening bank accounts.

It’s about bringing people into the global economy.

The Bottom Line

This was never just a banking problem.

It was never just an access problem.

It was always an identity problem.

And now…

That barrier is finally starting to break. 🔥