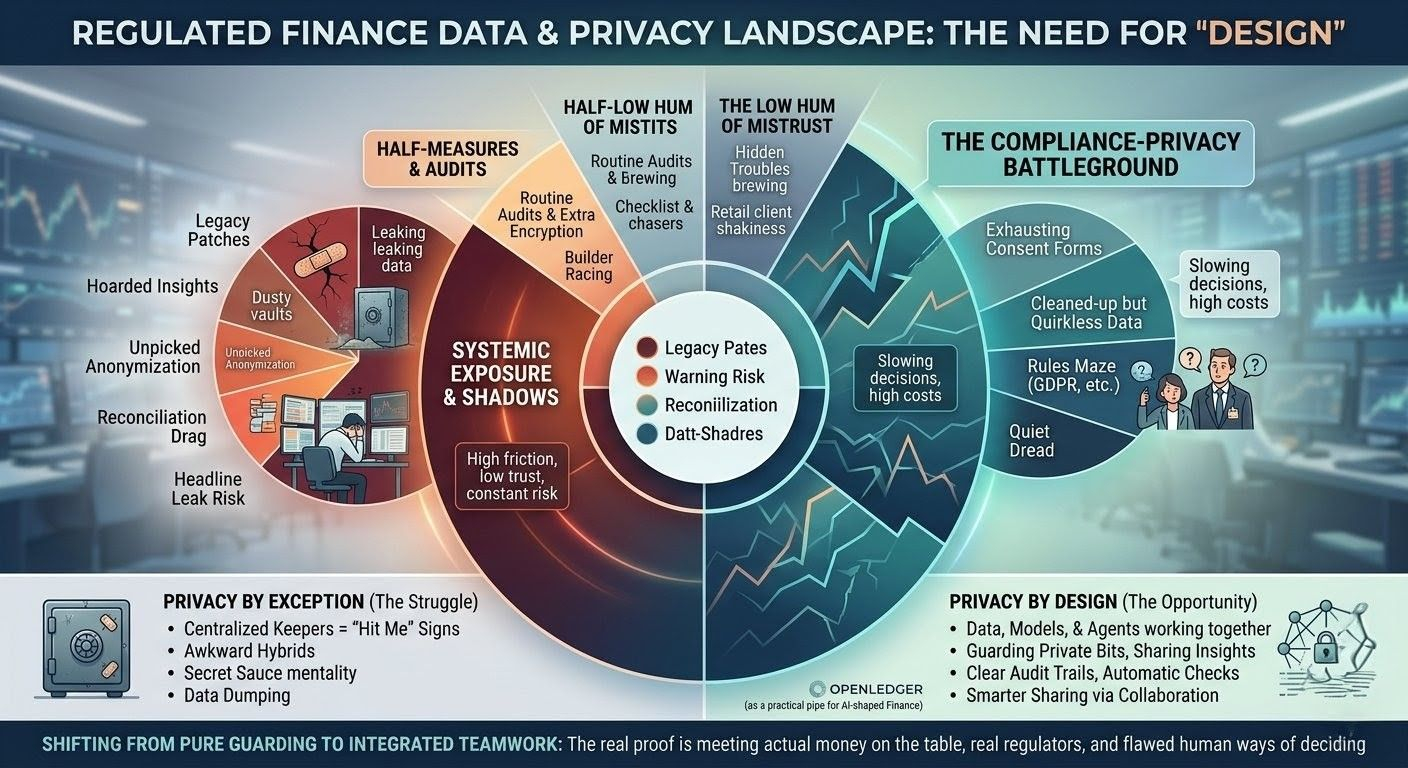

I've been turning this over in my head a lot lately, especially after yet another headline about a big financial player leaking customer data. It hits you while you're having your morning coffee, and you just sit there sighing, thinking, why do we keep slapping patches on the same cracks over and over? Let me paint a picture that's probably familiar to anyone in the trenches. There's this risk manager at a regional bank, maybe in Europe or out in Asia, juggling endless screens and deadlines. She's got stacks of real transaction data that could actually make her fraud detection sharper or help her run better stress tests on portfolios when the next shock hits. But the second she considers sharing even a bit of it—with a partner or even her own AI folks inside the firm—it becomes this exhausting maze of consent forms, those awkward anonymization steps, and this quiet dread that somebody clever will eventually connect the dots anyway. So the data just sits there, gathering digital dust, locked away tight. Meanwhile, regulators are knocking for more visibility into systemic risks. It's not lofty theory; it's the kind of everyday drag that slows decisions, piles on costs, and leaves you with this low-level feeling of being exposed.

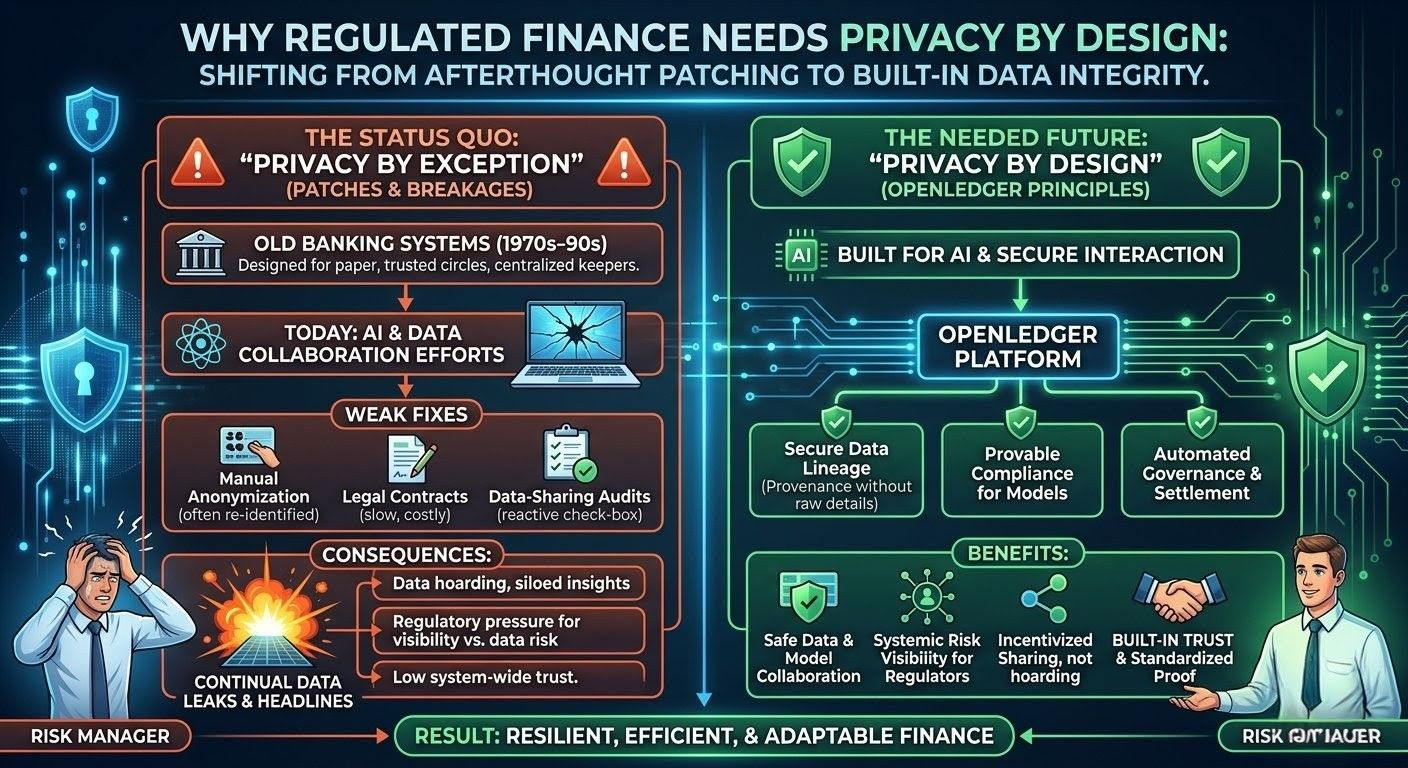

The root of it all, I reckon, goes back to how regulated finance grew up over decades. Privacy got added like an afterthought because the old setups were made for a slower time—paper files, phone calls between folks who knew each other, trusted middlemen. Now AI is gobbling up everything at speed, and those old compromises are showing their age badly. To build models that actually work, you need rich, real-world messy data. But trying to share it? It risks breaches, side-eyes from regulators, all of it. Those big centralized keepers promise safety but basically hang up "hit me" signs. And the anonymized versions everyone relies on? They get unpicked surprisingly fast these days. The fixes I've watched in real life always feel a bit makeshift and unsatisfying. Legal departments crank out page after page of agreements just to move data around once. Models get fed on cleaned-up bits that miss the human quirks that matter. Banks and funds hoard their sharpest insights like they're guarding family secrets, which means we all lose out on bigger-picture stuff—like spotting liquidity crunches early or building warnings that could help the whole system. It breeds this low hum of mistrust, wastes time, and crumbles when rules change from one country to the next.

Looking back, most of the solutions I've come across feel like half-measures. Throwing on extra encryption or running those routine audits sounds fine when you're presenting, but day-to-day it just means more steps to reconcile, slower everything, and teams chasing shadows trying to match records. The builders I know are usually racing to check regulatory boxes, so privacy ends up as a checklist item instead of something thought through from the start. Regulators ask for clear trails, but you get the sense they're uneasy too, worried that hiding too much might brew new troubles. Regular people—retail clients or company treasurers—feel the shakiness but stick with what they know because changing course seems scarier. And let's be honest about human nature: we're wired to get through today without too much trouble, not always planning for rock-solid setups years down the line. So we muddle through with privacy handed out only here and there—special permissions, locked gates—rather than something that just flows naturally with the data.

That's why OpenLedger has stuck with me in a low-key sort of way. Not as the next big flashy thing, but more like someone trying to lay down some basic pipes for finance that's getting more and more shaped by AI. It seems aimed at letting data, models, and even those self-running agents work together, with ways to follow who's using what and how value moves, while still guarding the really private bits. In the regulated parts of the world, it might ease some genuine headaches around showing where your model got its info from—proving it came from okay sources without spilling raw details about clients everywhere. The needs around settlement and following rules wouldn't just vanish, but maybe this setup could make the checks simpler without demanding you show everything.

I'm pretty wary though. I've seen enough past attempts trip up. Old banking systems don't plug in neatly; you often end up with these awkward hybrids that create even more tangles. Doing heavy AI stuff on a chain could rack up costs quicker than expected, and if the rewards for sharing data push people to dump in volume instead of good stuff, that'd be a problem. Legally, contracts on the chain help with some flows, but in the end, courts and watchdogs still want those paper trails and real people to hold responsible. Rules differ wildly across places—think strict European privacy takes versus others—and that won't smooth out easily. Plus, on a human level, I wonder if the big players will ever commit real weight here. A lot seem happier keeping their secret sauce in their own closed rooms, only testing waters carefully in small trials. My doubt comes from watching ideas that sounded decentralized quietly pull back toward centers once real stakes and money showed up.

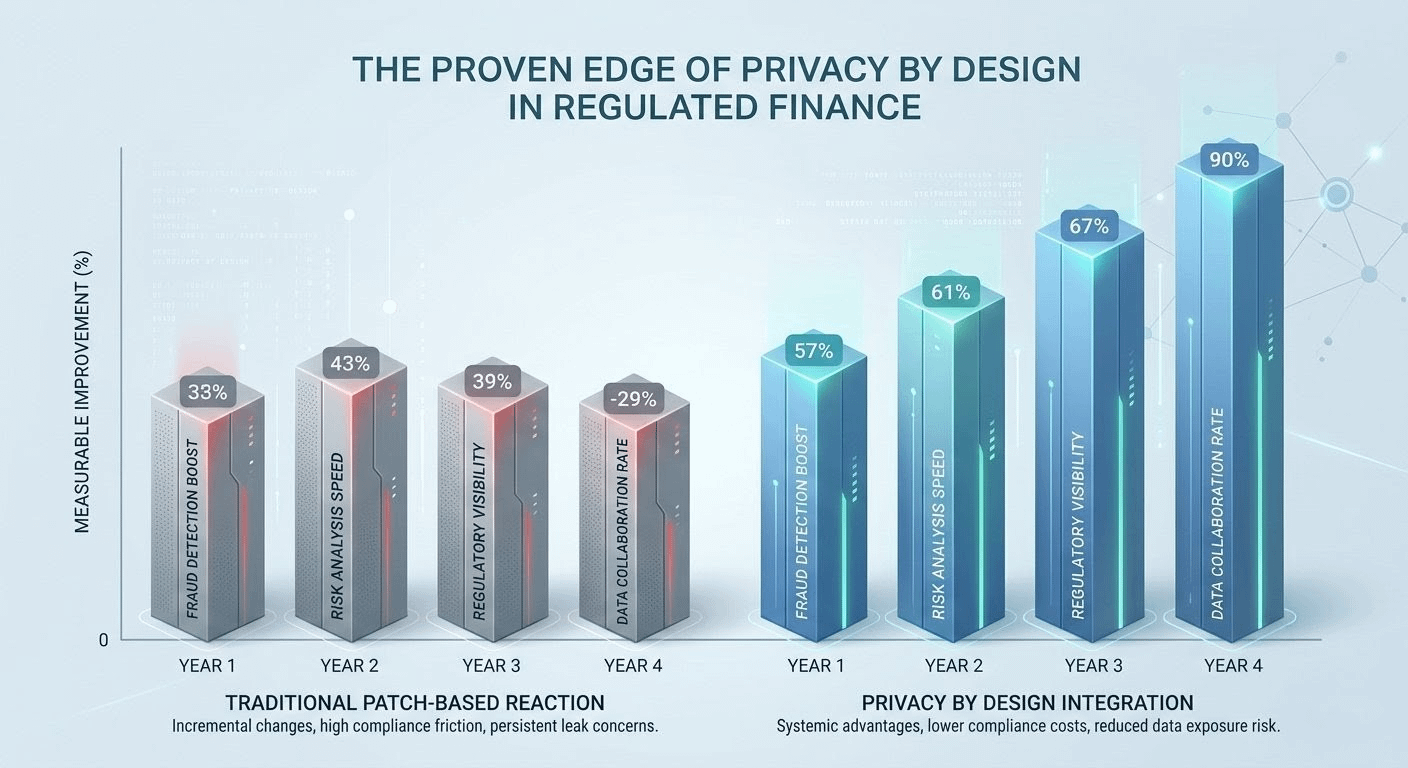

Still, there's something practical that tugs at me. Take trade finance or those shared reports on environmental stuff, where groups have to team up but can't show all their cards. A design like this might lighten the endless back-and-forth reconciliations and foster a bit more trust through clear records instead of crossed fingers. Banks adding patterns, smaller tech firms tweaking models—they could actually earn something back for their contributions, instead of it all flowing one way to the giants. It might slowly shift us from pure guarding to smarter sharing, building better shared resources over time. Privacy done this way isn't about total lockdown; it's cutting the leaks you don't need while allowing the teamwork that regulators sometimes call for to keep things steady. Day-to-day costs could drop if checking things gets more automatic. And folks might warm to it if it slips into their routines without forcing a total overhaul.

Of course, questions hang there. Will the rules around it stay fair and resist being taken over or flooded with junk? Can it give the rock-solid finality on deals that big institutions need, without leaning on outside helpers that bring old risks back? Real use will probably start small, in spots where faster model work and solid compliance proof clearly beat the hassle of setting up.

In the end, I suspect the first ones to give it a real go would be the practical mid-sized outfits: asset managers chasing better edges through shared AI without tying themselves to one supplier, fintechs that bridge old and new compliance, or groups teaming up in touchy areas like group loans. It could stick if it quietly shows in real tests that it cuts daily headaches and gives audit trails people feel good about—real help, no drama. It might stumble if the rewards twist behavior too much, if watchdogs demand stricter central points, or if it just can't fit with all the old systems and our built-in caution.

These setups don't need to be perfect. They just have to learn from the bruises we've collected—those leaks, dashed hopes, tough integrations. If OpenLedger grows into solid, quiet infrastructure instead of another show, it might find its place by making the data movements we can't escape in finance feel a touch less breakable. I'm keeping an eye on it with careful interest, no big bets. The real proof will come when it meets actual money on the table, real regulators in the room, and all our flawed human ways of deciding.