Bitcoin still matters because it is the only crypto asset that combines a credibly fixed monetary policy with the deepest security, liquidity, and institutional integration in the sector. In a market flooded with narratives, Bitcoin has quietly become the neutral base layer that the rest of the ecosystem continues to orbit.

Bitcoin’s dominance is not an accident

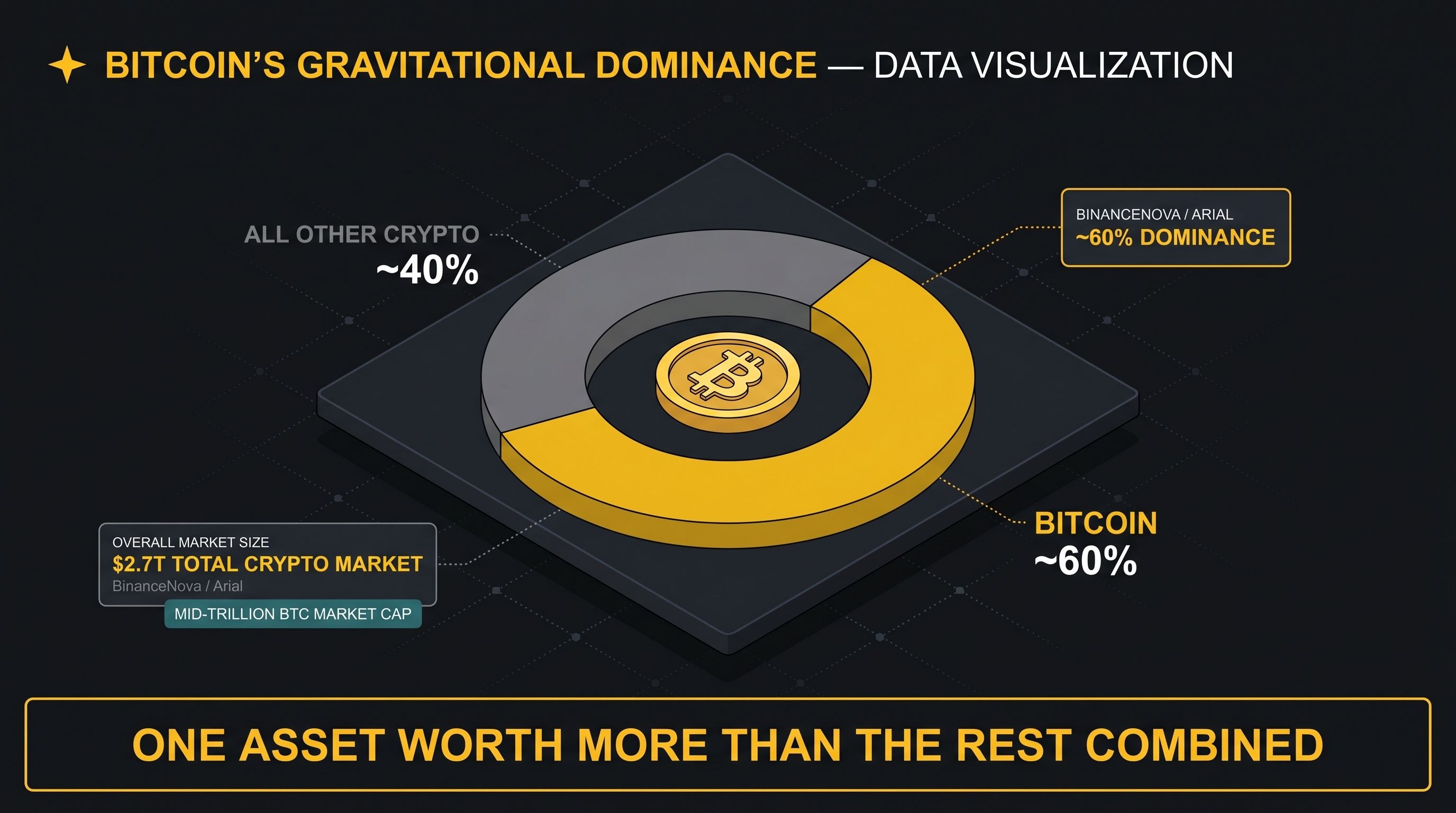

Despite thousands of tokens, Bitcoin still commands close to 60% of total crypto market capitalization, with current estimates putting its dominance around the high‑50s and sometimes above 60% depending on the source and day. Its market cap sits around the mid‑trillion range out of a roughly 2.7 trillion dollar crypto market, meaning one asset is more valuable than the rest of the field combined. That kind of gravitational pull is not just brand inertia; it reflects where large pools of capital feel safest parking size.

Monetary policy you can actually model

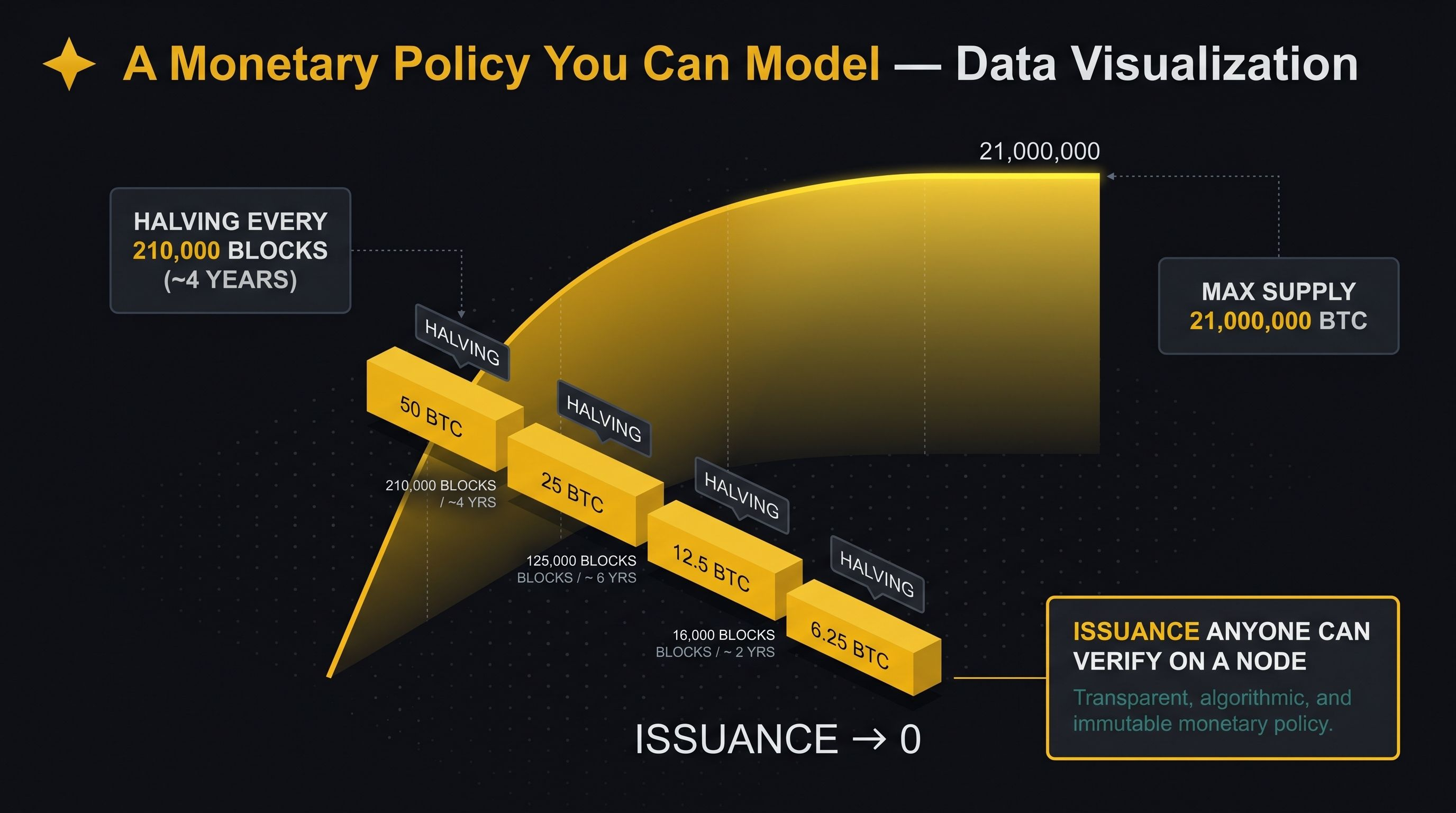

Bitcoin’s maximum supply asymptotically approaches 21 million coins, enforced by consensus rules rather than committees or tokenholder votes. New issuance follows a transparent schedule: block rewards started at 50 BTC and are cut in half every 210,000 blocks (roughly four years) until the subsidy effectively reaches zero. Anyone running a node can independently verify that issuance follows this curve, which is why Bitcoin’s long‑term inflation path is easier to model than almost any fiat currency or governance‑mutable token.

Security at industrial scale

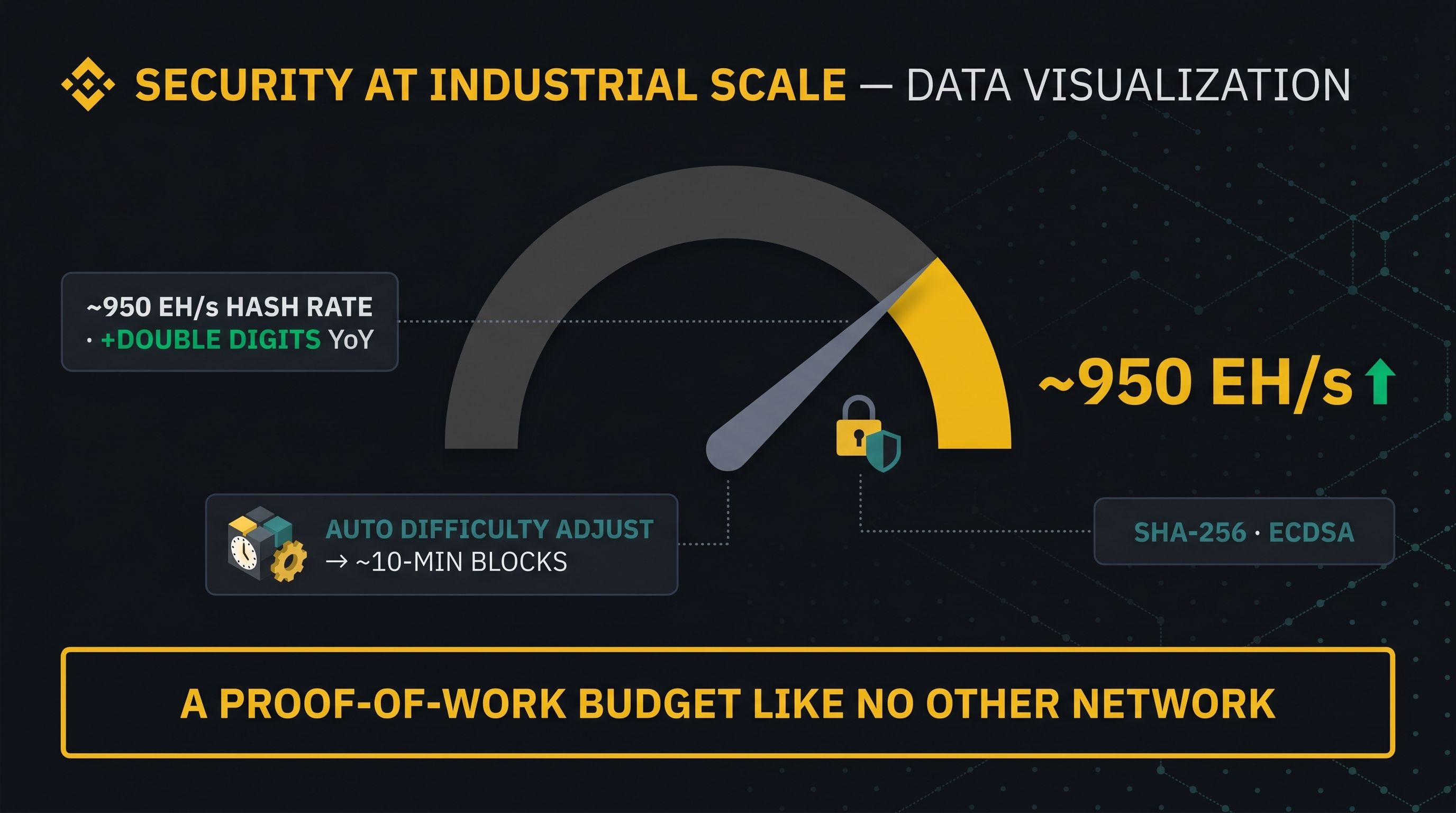

Bitcoin’s security budget is backed by one of the highest sustained hash rates of any proof‑of‑work network in history, currently around 950 million terahashes per second (about 950 exahashes) and up double‑digit percentages versus a year ago. Even after weather‑driven miner shutdowns pushed hash rate below 1 zettahash and triggered some of the largest difficulty drops since the China mining ban, the protocol’s automatic adjustment mechanism kept blocks targeting roughly 10‑minute intervals. Under the hood, Bitcoin relies on SHA‑256 hashing and ECDSA signatures, with collision attacks estimated to require energy on the order of stellar outputs over billions of years, far beyond any realistic adversary.

The ossified base layer is a feature

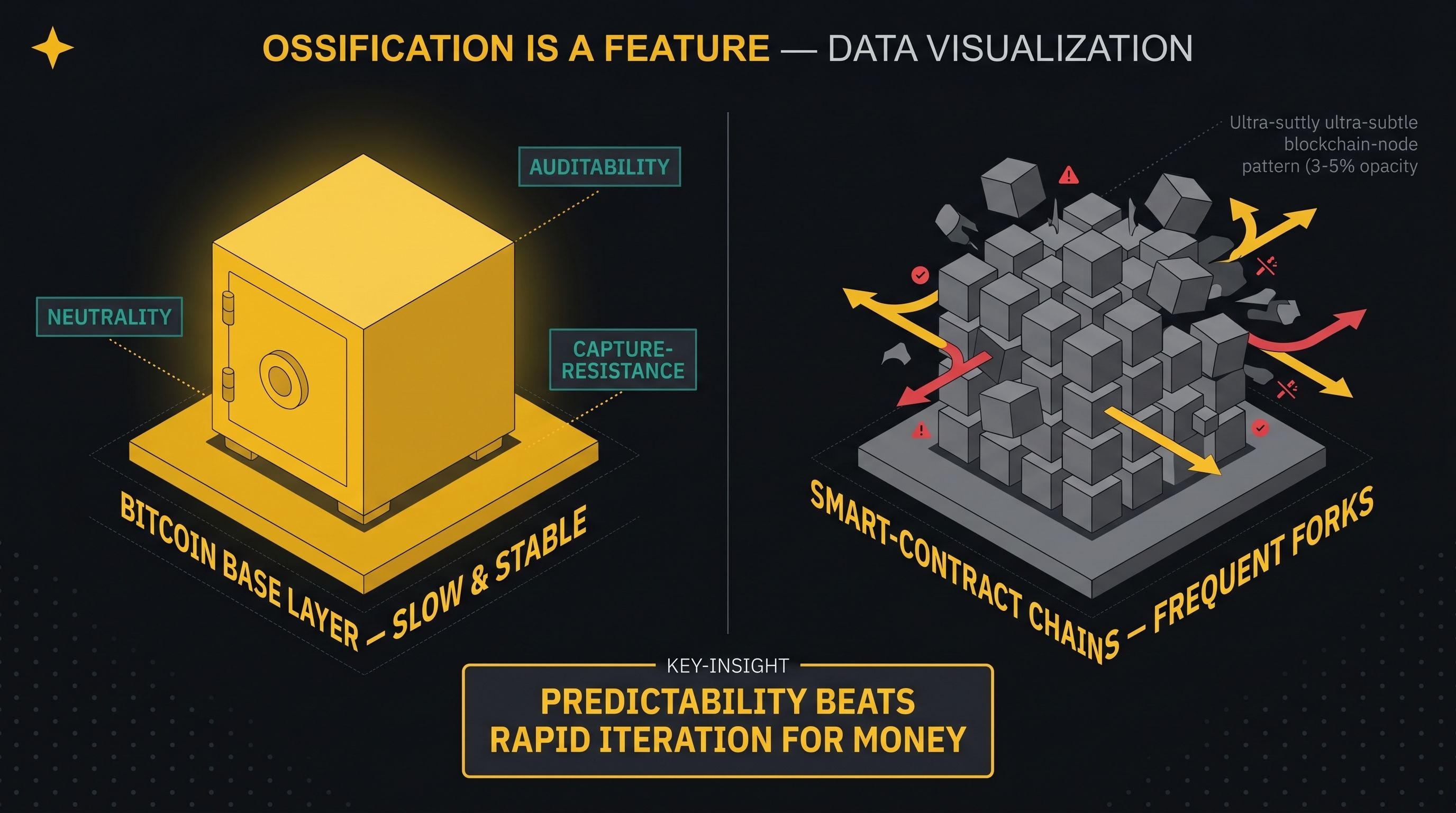

Bitcoin’s core protocol changes slowly and conservatively compared to smart‑contract platforms that ship frequent hard forks and experimental features. That conservatism is intentional: monetary and settlement layers benefit from predictability and backward compatibility more than from rapid iteration. While other chains compete on throughput and expressivity, Bitcoin’s base layer optimizes for neutrality, auditability, and resistance to capture, making it a credible foundation for long‑lived value storage.

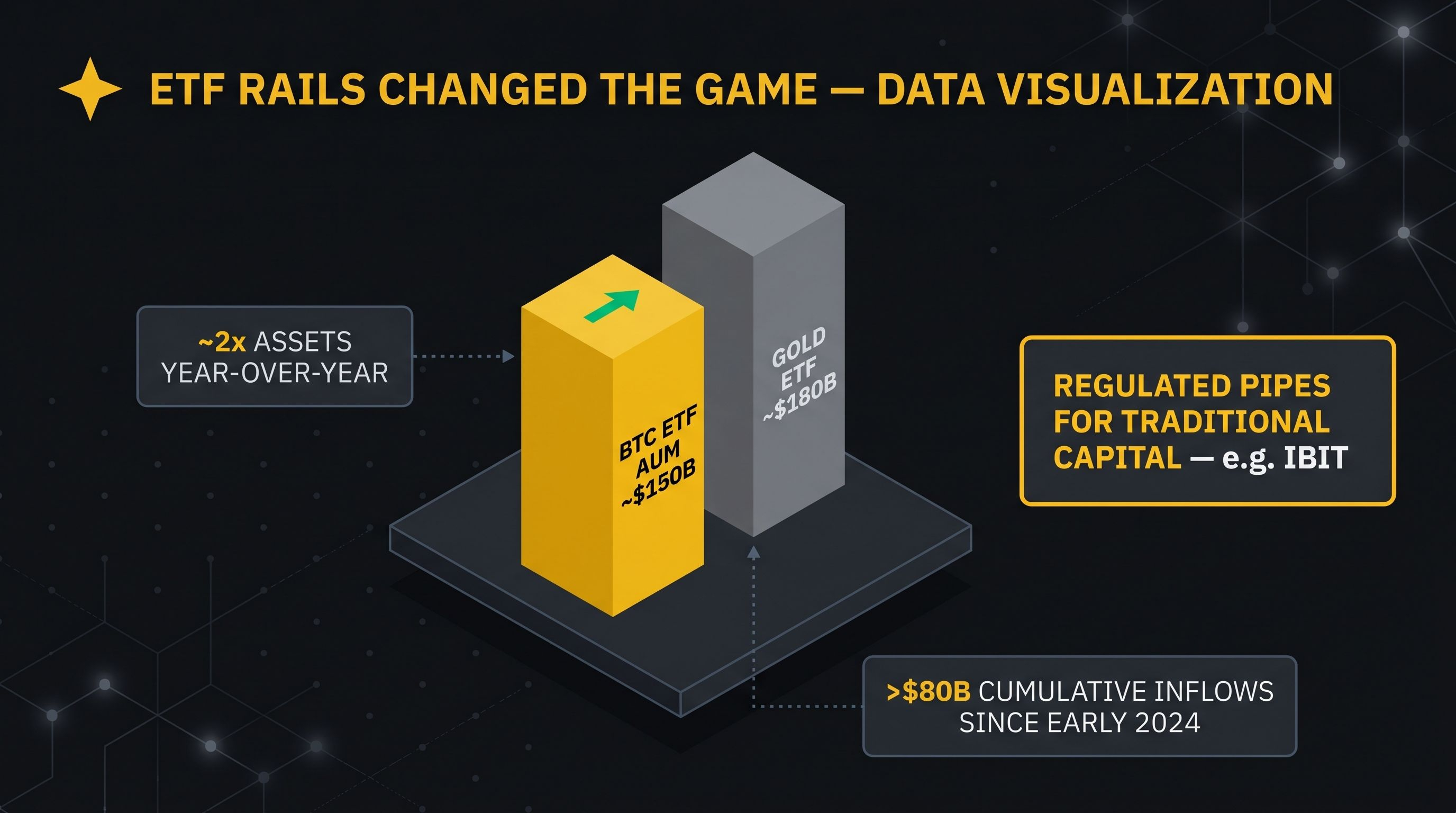

Liquidity and ETF rails changed the game

Since U.S. spot Bitcoin ETFs were approved in early 2024, regulated products have become one of the main pipes through which traditional capital accesses BTC. By mid‑2025, Bitcoin ETFs had roughly doubled assets under management year‑over‑year to about 150 billion dollars, closing in on gold ETFs at around 180 billion and marking a structural shift in how allocators gain exposure. Cumulative net inflows into global crypto ETPs since the ETF launch have surpassed 80 billion dollars, with flagship funds like BlackRock’s IBIT alone managing tens of billions and trading billions in daily volume.

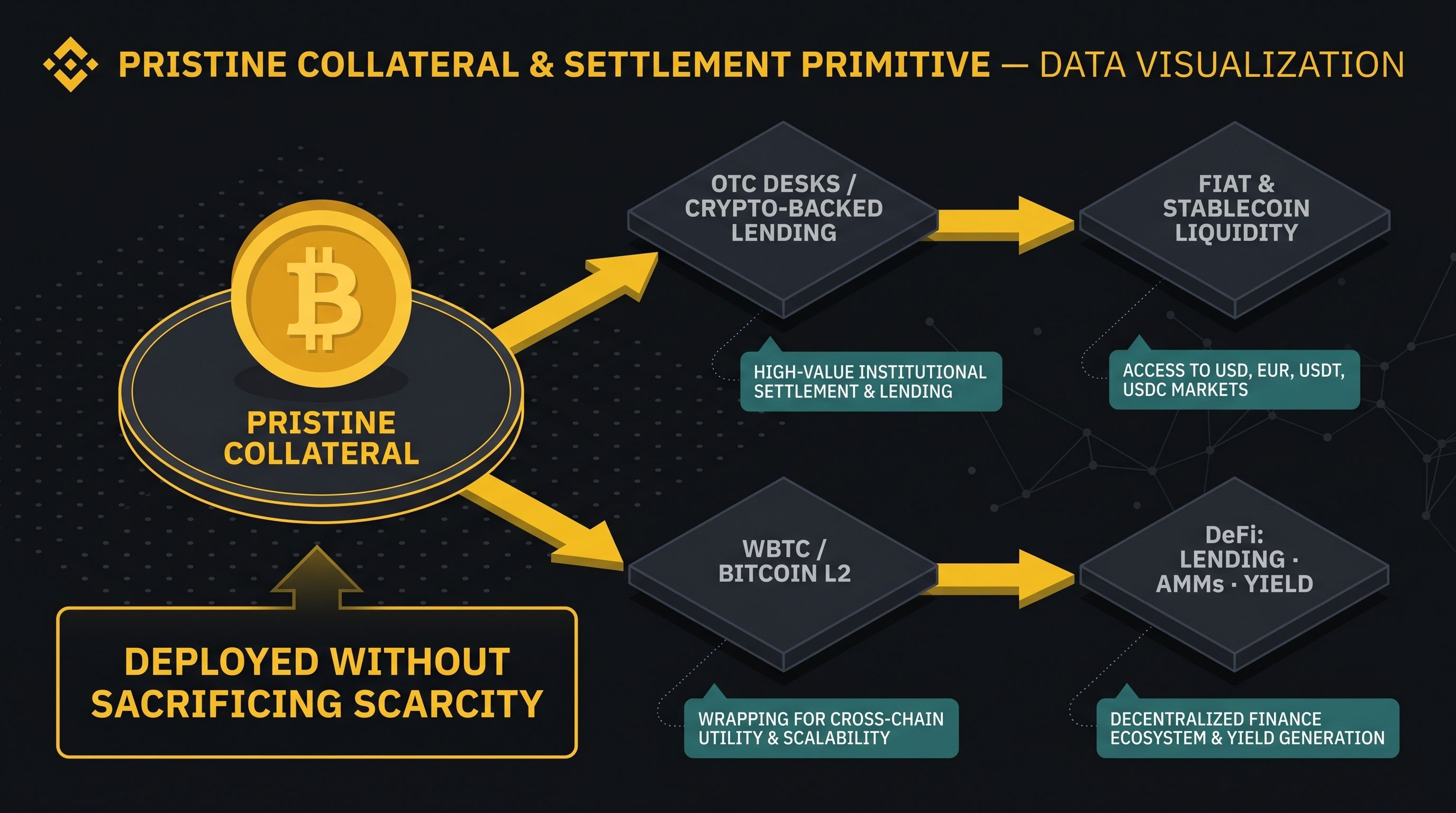

Bitcoin as collateral and settlement primitive

In practice, Bitcoin increasingly functions as pristine collateral rather than just a speculative chip. OTC desks report BTC borrowing demand driven both by shorting and by using BTC as collateral in structured products and loans. Crypto‑backed lending platforms now routinely accept Bitcoin deposits in exchange for fiat or stablecoin liquidity, treating BTC similarly to blue‑chip collateral in traditional prime brokerage. On the programmable side, wrapped Bitcoin (WBTC and similar) and emerging Bitcoin‑native Layer 2s allow BTC to be deployed into DeFi, where it can secure lending markets, AMMs, and other yield‑bearing strategies without sacrificing the base asset’s scarcity narrative.

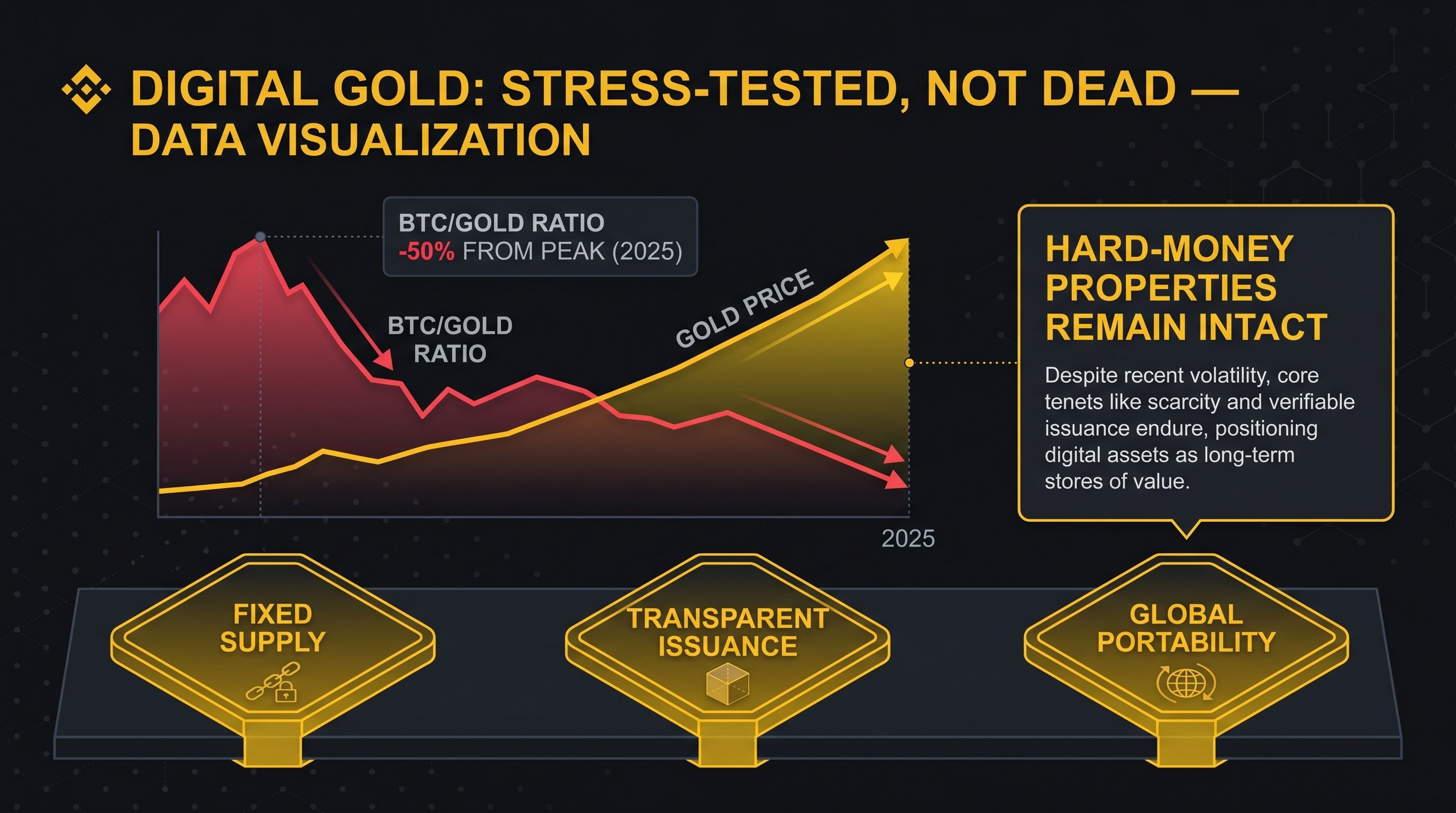

Digital gold narrative: stress‑tested, not dead

Bitcoin’s “digital gold” framing has taken hits, especially in periods where gold outperforms while BTC trades more like a high‑beta tech asset. In 2025, for example, the BTC‑to‑gold ratio fell more than 50% from peak levels even as gold logged strong gains, forcing allocators to re‑evaluate the safe‑haven claim. Analysts and empirical work have noted that Bitcoin has not yet behaved like a classic crisis hedge, with drawdowns often exceeding those of equities and correlations spiking in risk‑off regimes. But the hard‑money properties—fixed supply, transparent issuance, global portability—remain intact, and many portfolio frameworks now treat Bitcoin as a long‑duration, asymmetric “hard money” bet alongside, not instead of, gold.

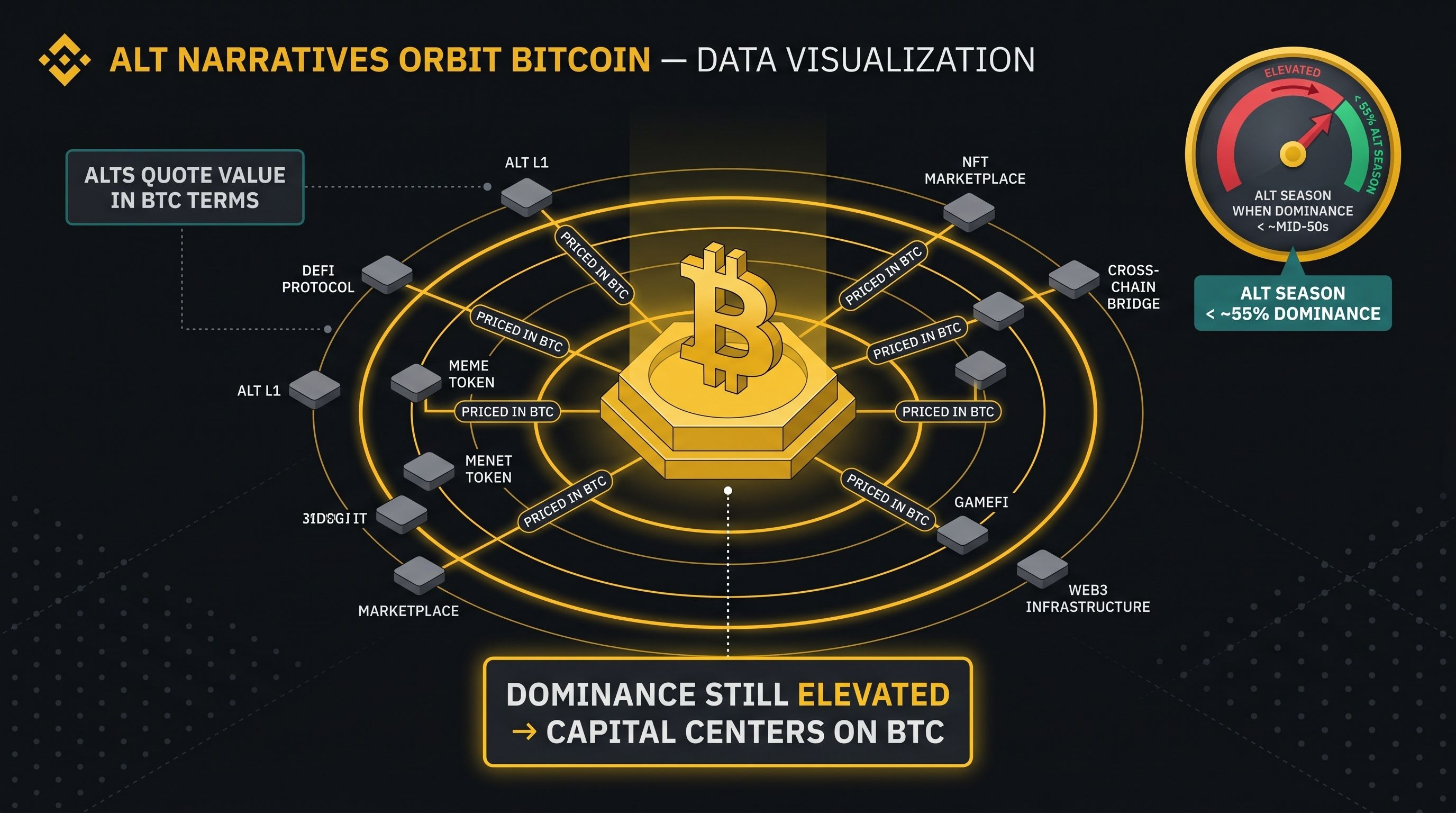

Why alt narratives still sit on Bitcoin’s shoulders

Most alternative L1s and DeFi protocols ultimately quote value in BTC terms or are heavily influenced by BTC cycles, even when their local narratives focus on throughput, modularity, or real‑world assets. Market structure data shows that strong “alt seasons” generally emerge when Bitcoin dominance falls below the mid‑50s, yet current dominance remains elevated by historical standards, signaling that capital still reflexively centers on BTC in uncertain environments. Meanwhile, Bitcoin’s own narrative surface is expanding—from passive store‑of‑value to yield‑generating collateral and base money for Layer 2 ecosystems—without requiring changes to the underlying monetary policy.

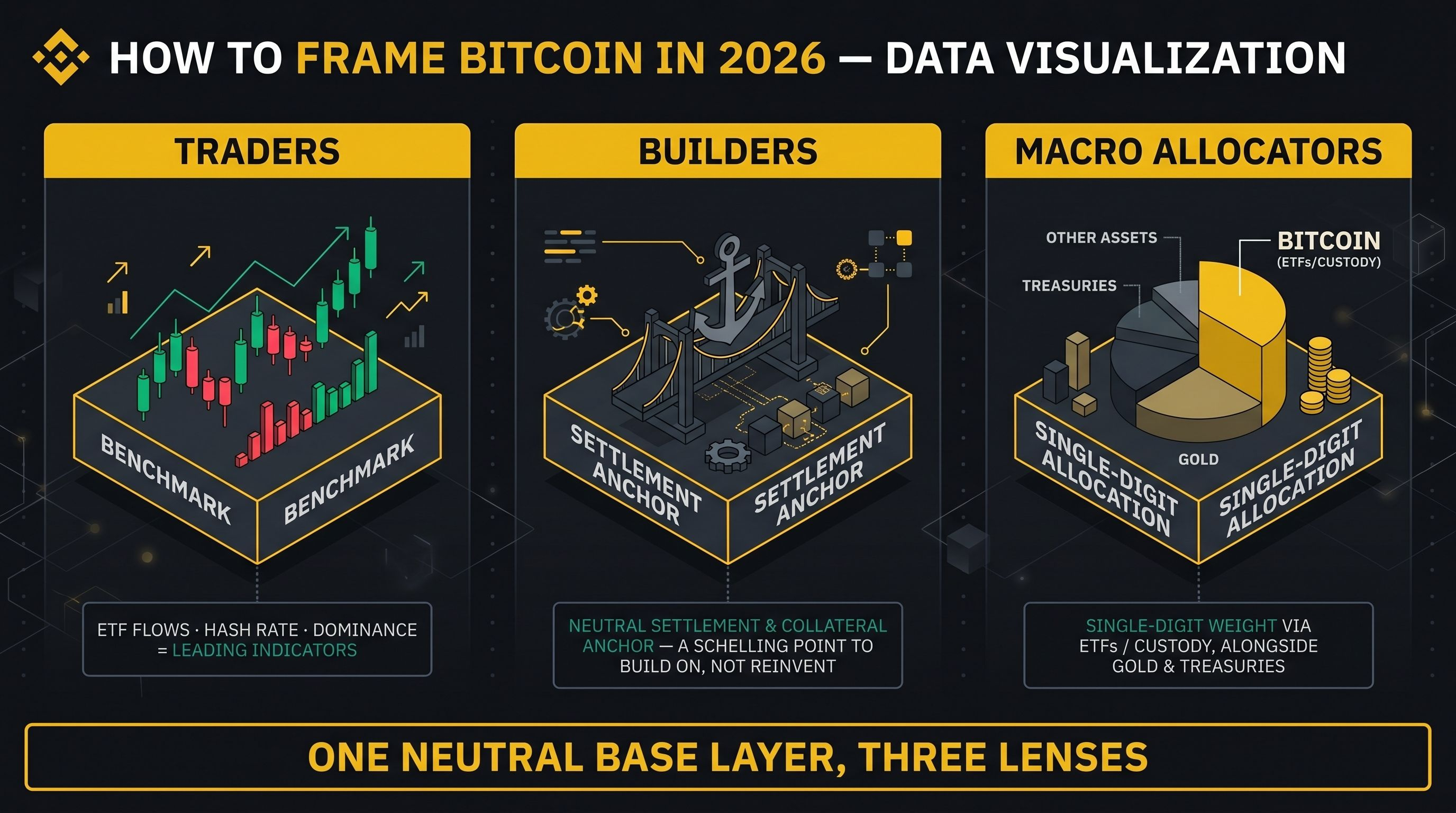

How to frame Bitcoin in 2026

For traders, Bitcoin is the benchmark asset that defines regime shifts: ETF flows, hash rate trends, and dominance levels are leading indicators for broader crypto risk appetite. For builders and protocol designers, Bitcoin is the neutral settlement and collateral anchor that can be integrated, bridged, or built on top of, but not casually reinvented, giving the ecosystem a Schelling point for value even as experimentation continues elsewhere. For macro allocators, it is increasingly a structured allocation—often single‑digit portfolio weight—expressed via ETFs or custody solutions, sitting alongside gold and Treasuries as part of a “hard‑money plus risk” sleeve rather than a fringe speculation.