Executive Summary

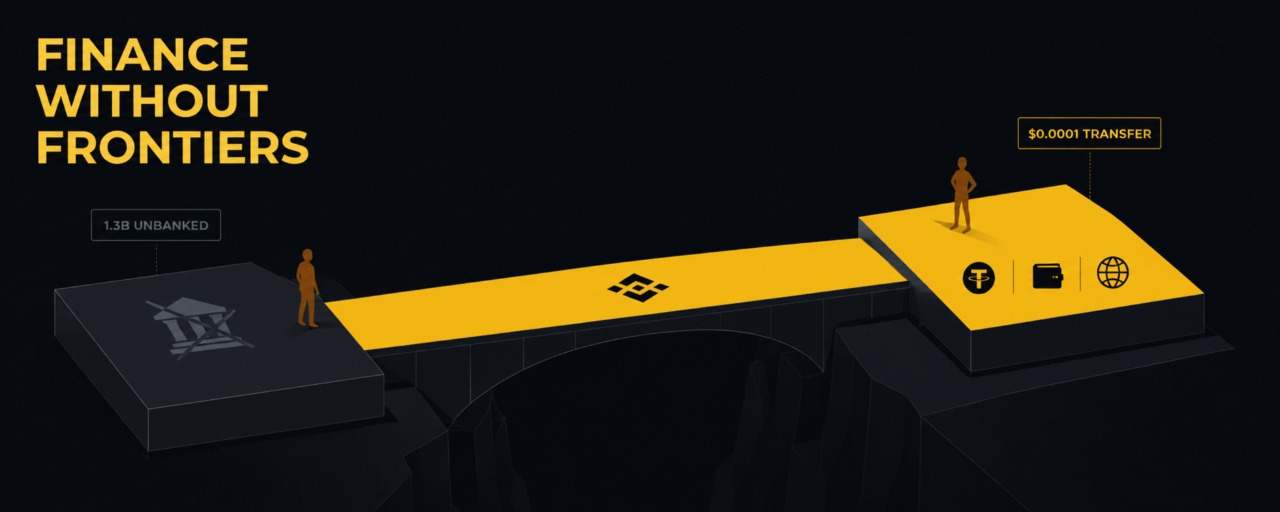

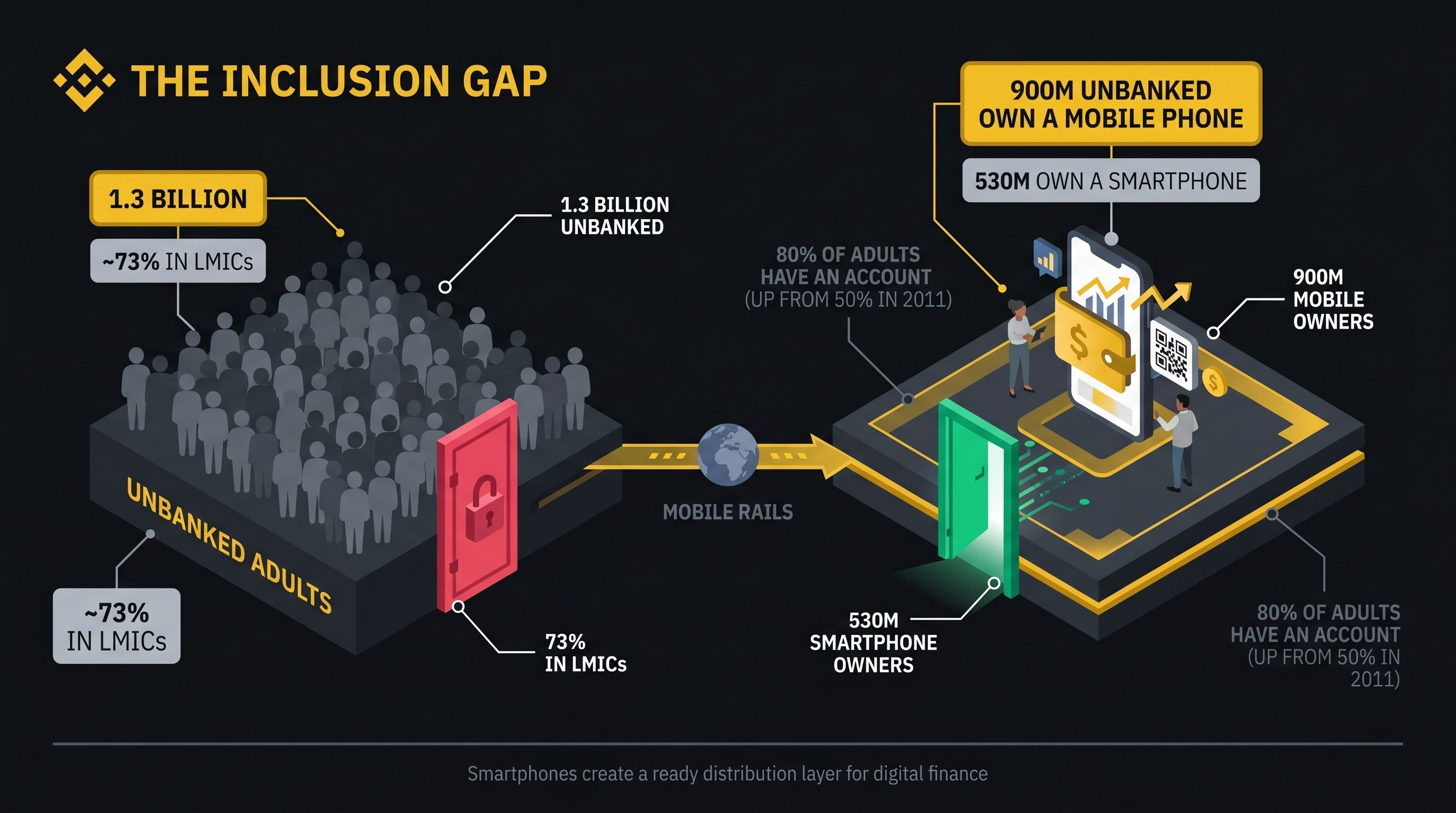

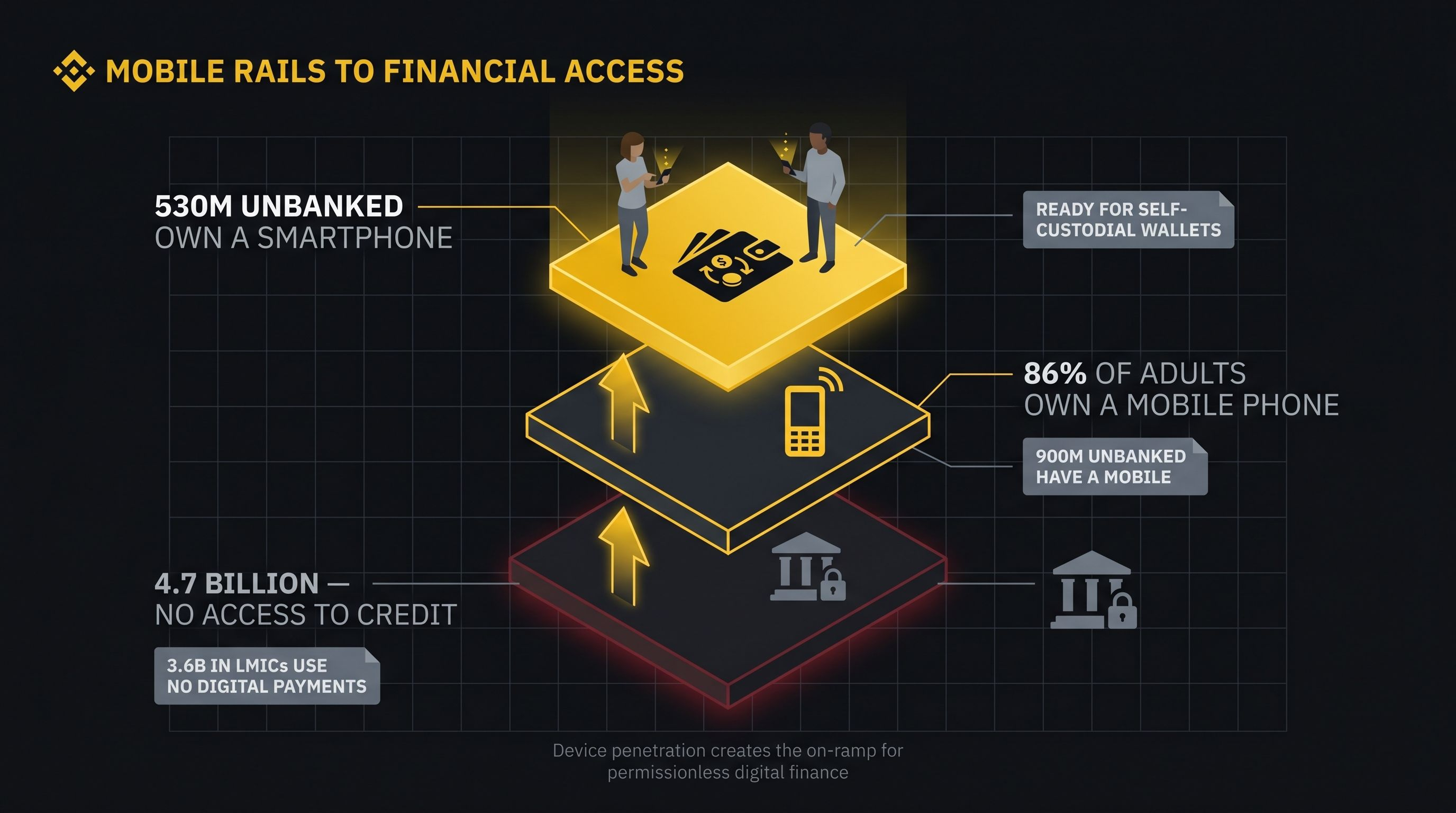

Global financial inclusion has improved over the last decade, yet around 1.3 billion adults still lack access to formal financial services, and billions more are underbanked. At the same time, mobile-phone penetration has surged: roughly 900 million unbanked adults own a mobile phone and over 500 million own a smartphone, creating a ready distribution layer for digital finance.

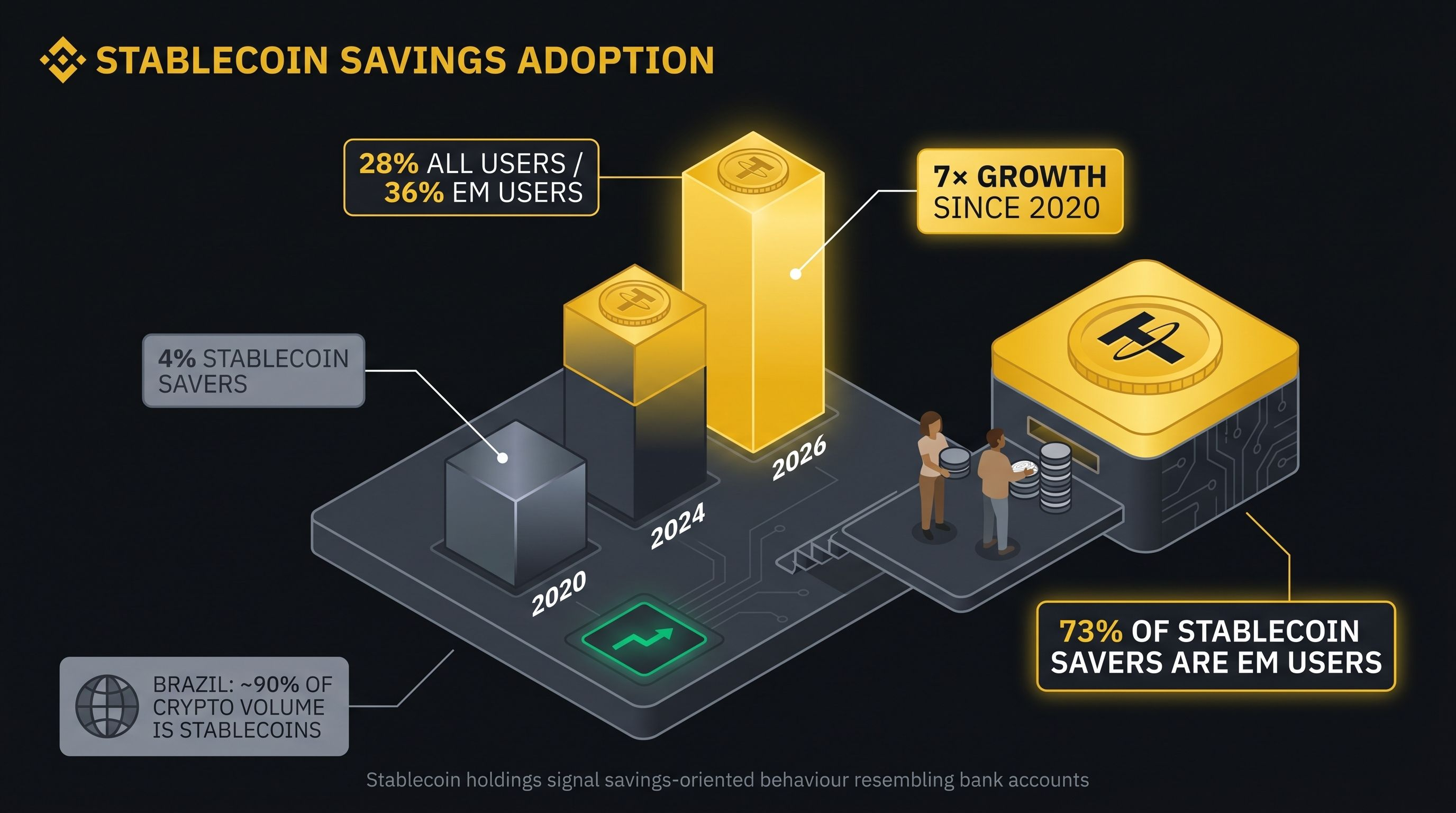

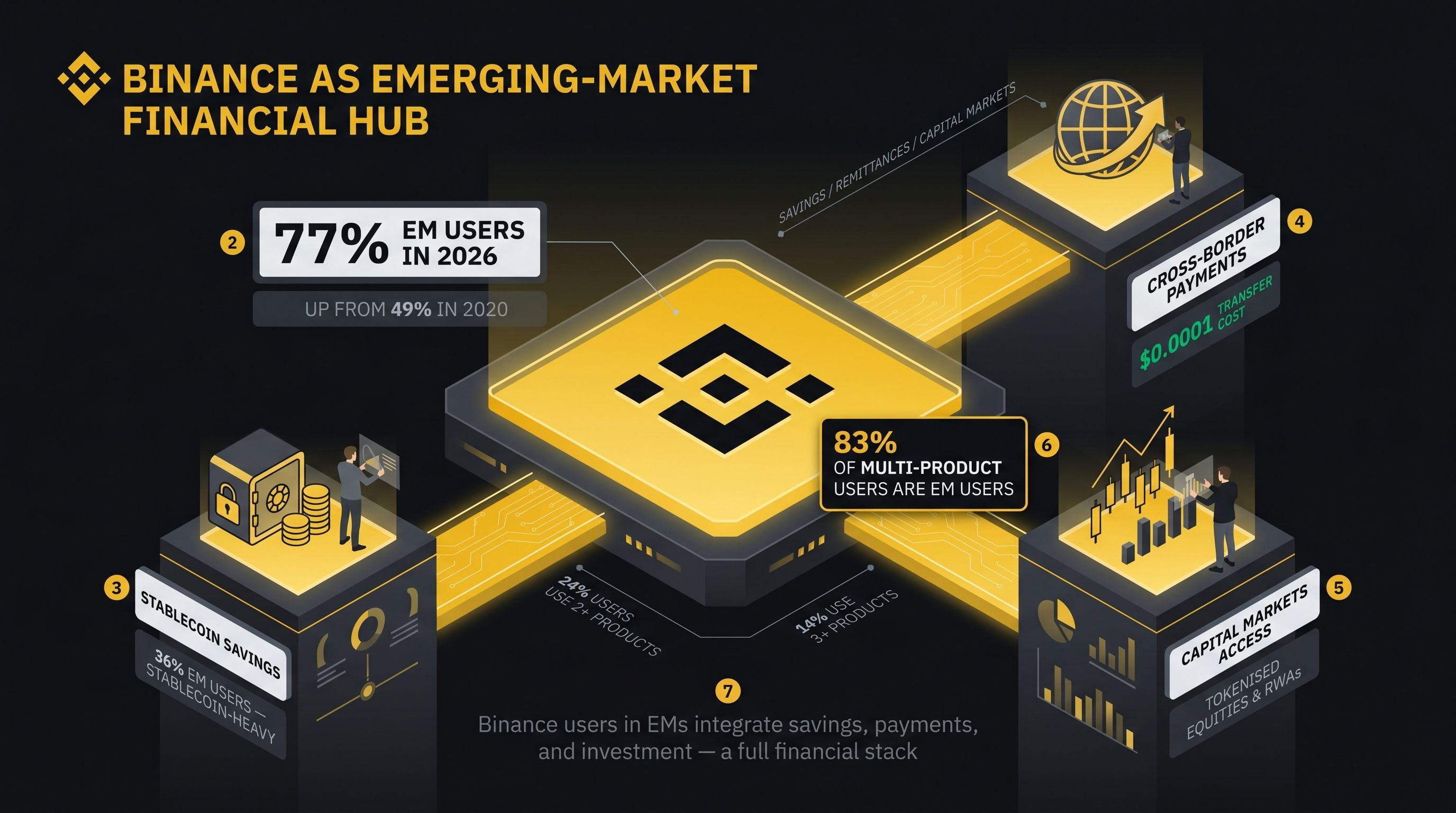

Binance Research argues that this device layer — combined with stablecoins and crypto exchanges — is now functioning as de facto banking infrastructure in many emerging markets (EMs). Emerging-market users account for 77% of Binance's user base in 2026, up from 49% in 2020, and they are using the platform primarily for savings, remittances, and payment-like behaviour rather than pure speculation. Stablecoins sit at the centre of this shift: a rising share of EM users hold at least half their portfolio in stablecoins, and 73% of all stablecoin "savers" on Binance are based in EMs — signalling savings-oriented usage that closely resembles bank-account behaviour.

The Inclusion Gap and Mobile Rails

Unbanked and Underbanked at Scale

The latest World Bank Global Findex data shows that nearly 80% of adults worldwide now have some kind of financial account, up from 50% in 2011 — but about 1.3 billion adults still lack access to formal financial services. The problem is not binary. Binance Research highlights that:

4.7 billion adults lack access to credit or loans.

3.6 billion adults in low- and middle-income countries (LMICs) do not use digital payments or cards.

1.4 billion savers in LMICs earn no interest on their deposits.

This underbanked cohort often holds nominal accounts but has limited access to credit, cross-border transfers, or yield-bearing savings.

The geographic concentration of exclusion is stark. Roughly 73% of unbanked adults live in LMICs, with more than half concentrated in just eight countries. Five of those eight countries also rank among the top twenty in the Chainalysis Global Crypto Adoption Index — suggesting that users in financially excluded markets are disproportionately turning to permissionless digital networks.

Mobile Phones as the New Branch Network

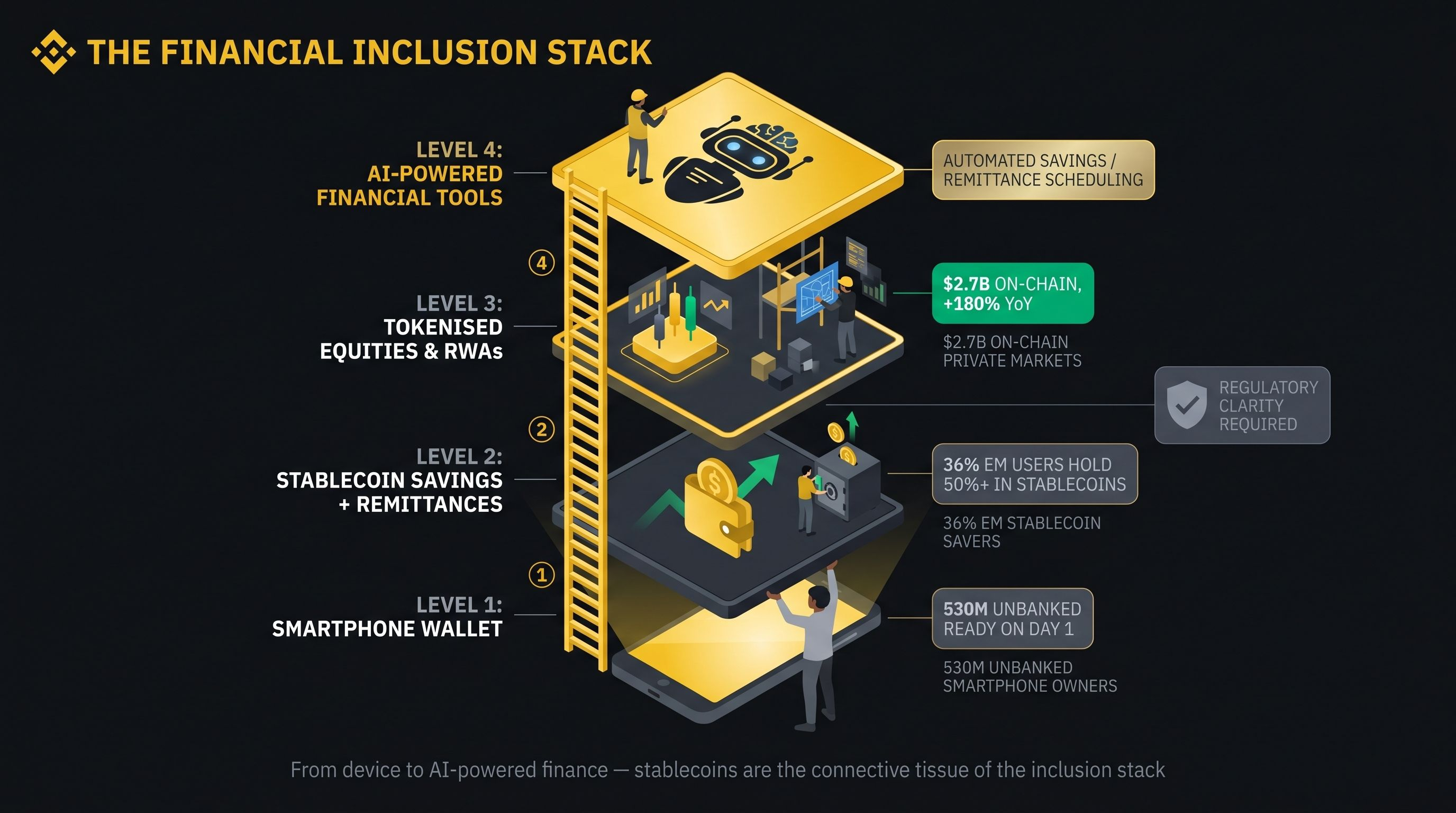

The Findex report and Binance Research converge on a key enabler: mobile devices. Globally, about 86% of adults own a mobile phone and 68% own a smartphone. Among the unbanked, around 900 million have a mobile phone and 530 million have a smartphone, meaning most people excluded from traditional banking already carry the hardware required for self-custodial wallets or exchange apps.

World Bank data shows that in developing economies, the share of adults saving in a financial account rose to 40% in 2024 — the fastest increase in more than a decade — with mobile-money accounts driving a five-percentage-point rise in mobile savings specifically. Earlier research on Kenya's M-Pesa ecosystem found that mobile money lifted about 2% of households out of extreme poverty, underscoring how device-mediated access to deposits, transfers, and savings can translate into real welfare gains.

Why Stablecoins Matter More in Emerging Markets

Cost and Speed Advantages in Remittances

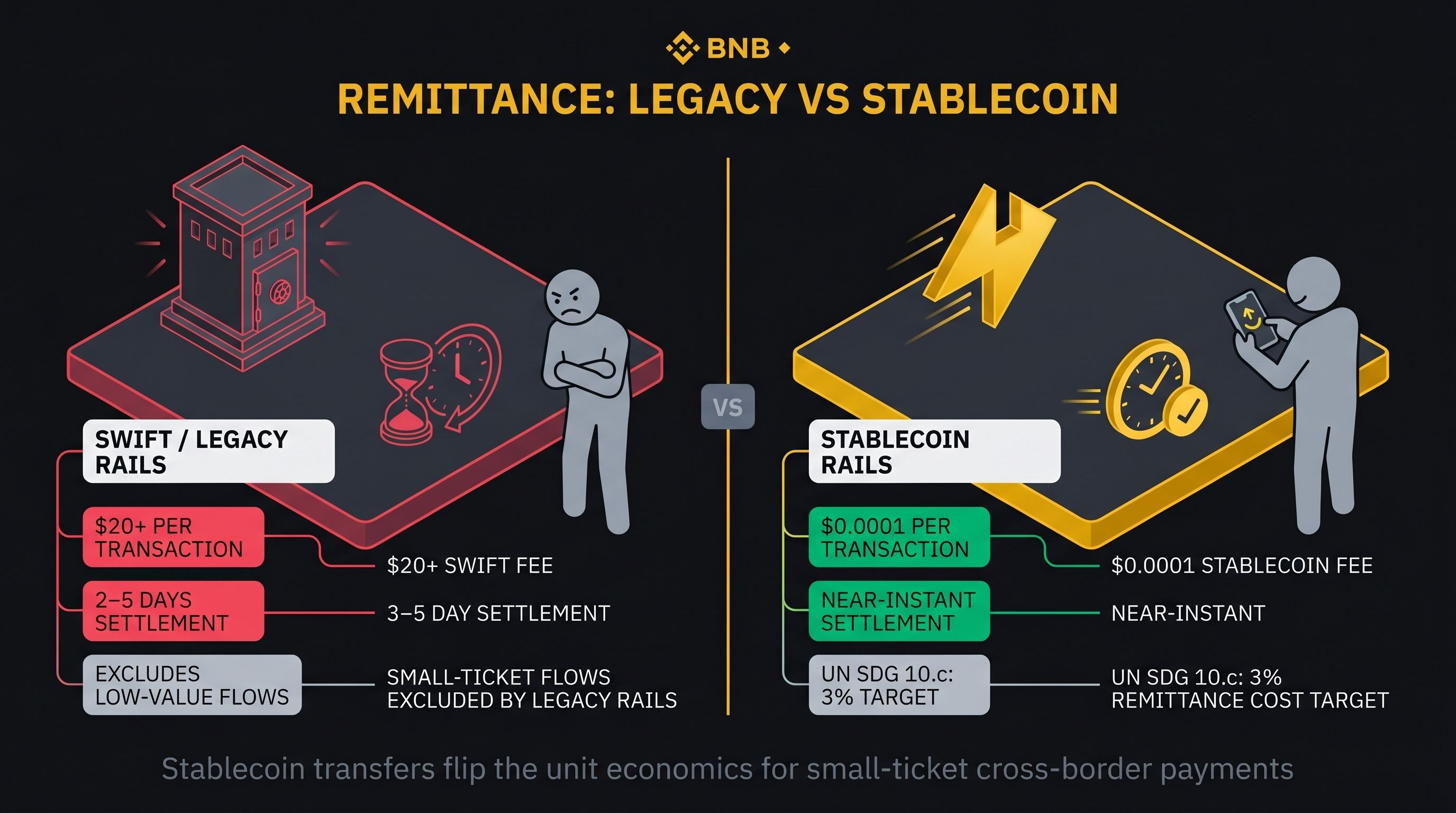

Cross-border payments via legacy rails such as SWIFT often cost at least $20 per transaction and settle in days — a fee burden that amounts to roughly 1% only for transfers above $2,000, effectively excluding most low-value remittance flows. Stablecoin transfers on high-throughput networks can cost as little as $0.0001 and settle in seconds, fundamentally flipping the unit economics for small-ticket cross-border payments.

This cost differential matters most in low-income corridors where beneficiaries are highly price-sensitive and transaction sizes are small. The UN Sustainable Development Goal 10.c targets a global average remittance cost of 3%, but many corridors remain well above that threshold. Stablecoins offer a credible path to meeting this goal by collapsing both fees and settlement times simultaneously.

Store-of-Value and Dollarisation Use Cases

In EMs with volatile local currencies and elevated inflation, stablecoins function as synthetic dollar bank accounts. Binance Research finds that about 28% of Binance users with balances of at least $10 hold at least half their portfolio in stablecoins — up from just 4% in 2020, a seven-fold increase. Among EM users specifically, 36% meet this threshold, and 73% of all stablecoin savers on the platform are based in EMs.

Brazil illustrates this pattern vividly: tax-authority statistics show that stablecoins account for roughly 90% of the country's total crypto transaction volume, reflecting dominant use for payments, remittances, and value storage rather than speculation. For retail users, a smartphone wallet holding stablecoins becomes a portable, transferrable, multicurrency savings account that works across borders.

Binance as a Substitute Bank Account

A Demographic Pivot Toward Emerging Markets

Binance's user base has undergone a structural shift since 2020. The share of users from emerging markets rose from 49% in 2020 to 77% in 2026. These users are not primarily using the exchange for short-term trading; instead, they are saving, sending remittances, and accessing capital markets in ways that mirror retail-bank behaviour.

Multi-product engagement reinforces this interpretation. Around 24% of active Binance users now use two or more platform products, and 14% use three or more. Of this multi-product cohort, 83% are based in emerging markets — indicating that EM users are integrating Binance into a broader personal financial stack spanning savings, payments, and investment, rather than treating it solely as a speculative venue.

Platform-as-Bank: What the Data Shows

The external framing of crypto exchanges as "shadow banks" or "banking apps" is increasingly backed by hard numbers. A smartphone plus a Binance account gives an EM user:

Savings — stablecoin holdings earning yield through on-platform products.

Payments & remittances — cross-border transfers at a fraction of SWIFT costs.

Investment access — exposure to global equities, tokenised RWAs, and capital markets previously inaccessible locally.

Always-on availability — 24/7 access not constrained by branch hours or local bank holidays.

In effect, the exchange plus a stablecoin wallet functions as an account that is multicurrency, cross-border, always-on, and often yield-bearing — a feature set that many incumbent banks in EMs cannot match.

Beyond Payments: Capital Markets and Tokenisation

Brokerage and Capital-Market Access Gaps

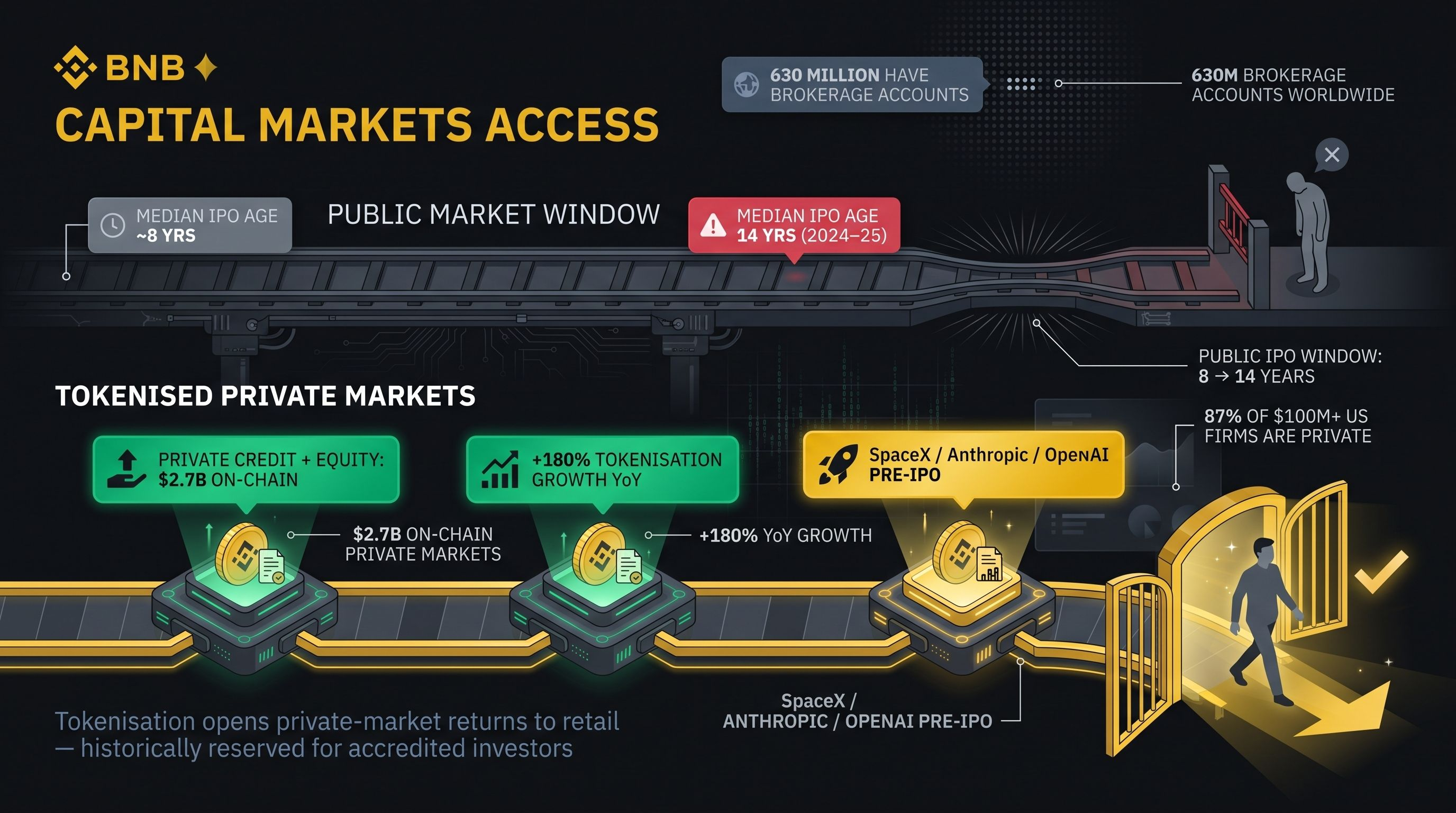

Traditional brokerage access remains severely limited relative to global market capitalisation. The World Federation of Exchanges estimates that about 630 million adults hold an online brokerage account worldwide, with an even smaller share enjoying direct access to US markets — despite the US accounting for roughly half of global equity market capitalisation.

For EM retail investors, local brokerage offerings can be expensive, narrow in product range, or entirely absent. Tokenised equities and perpetual contracts on crypto platforms partially address this mismatch by enabling 24/7 trading, fractional ownership, and cross-border access without requiring a domestic broker-dealer relationship.

Private-Market Democratisation via Tokenisation

Access gaps are even more acute in private markets. About 87% of US firms with revenue above $100 million are privately held (Altrata Billionaire Census), and the median age of companies at IPO climbed from roughly 8 years to 14 years between 2000 and 2025 (Apollo data), compressing the window during which retail investors can access early-stage value creation through public markets.

Tokenised private credit and private equity have reached approximately $2.7 billion on-chain — still small relative to the total private-market universe but growing rapidly, with tokenisation market value up roughly 180% over the past year. Pre-IPO contracts referencing firms such as SpaceX, Anthropic, and OpenAI appreciated by double-digit percentages in 2026, demonstrating the scale of returns historically captured exclusively by accredited investors.

Programmable Finance for Humans and AI Agents

On-Chain Primitives for Machine Participants

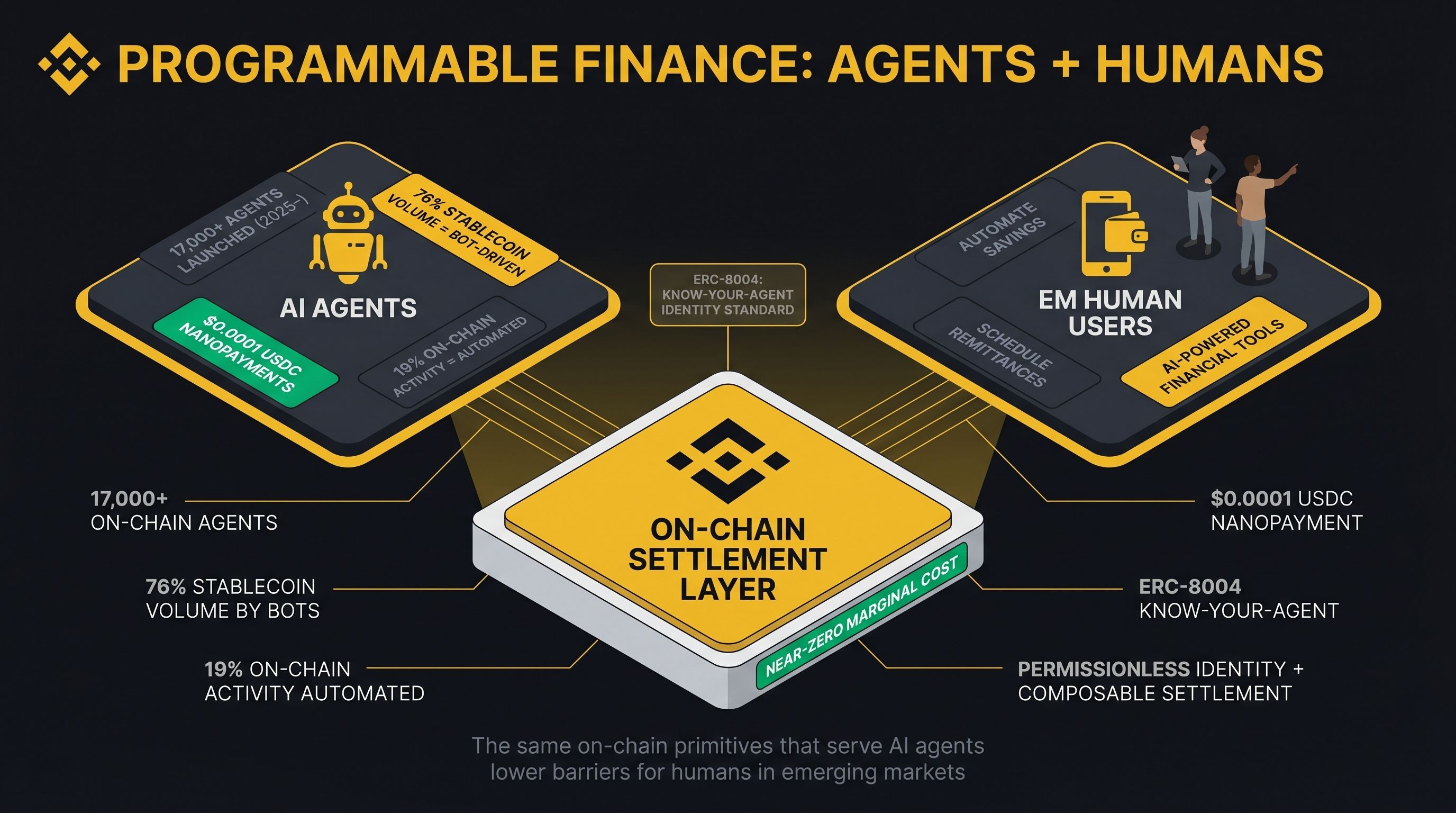

Binance Research extends the financial inclusion frame beyond human participants, arguing that AI agents also require accessible financial primitives. On-chain finance offers three properties in combination that are difficult to replicate off-chain:

Programmable money — USDC nanopayments can settle amounts as low as $0.0001, far below the ~$0.30 floor fee on conventional card networks.

Permissionless identity — emerging standards such as ERC-8004 provide "Know-Your-Agent" frameworks for autonomous actors.

Composable settlement — atomic cross-protocol transactions without intermediary clearing.

Empirically, more than 17,000 agents have been launched on-chain since 2025, with around 19% of on-chain activity now automated or agentic and 76% of stablecoin transfer volume driven by bots. These flows already represent a material share of network throughput.

Why This Matters for EM Users

The same infrastructure that enables agents to transact also lowers barriers for human users in EMs. Once a user connects a wallet or exchange account to a mobile device, they can automate savings (e.g., recurring stablecoin purchases), schedule remittance flows, or interact with AI-powered financial tools that would be inaccessible via local banks. The programmable nature of on-chain finance amplifies the inclusion gains unlocked by basic access — compounding benefits up the stack.

Regulatory and Systemic Risk Considerations

Monetary Sovereignty and Financial-Stability Concerns

While stablecoins and crypto exchanges are unlocking new forms of access, they raise legitimate macro-financial concerns. The IMF and Moody's have warned that large-scale stablecoin adoption in EMs can undermine monetary sovereignty, complicate capital controls, and introduce new contagion channels if major stablecoins fail or experience a significant de-peg event.

Regulators in multiple jurisdictions are responding with frameworks covering licensing, reserve transparency, and conduct-of-business rules for stablecoin issuers and exchanges. The World Bank simultaneously emphasises the need for robust consumer-protection regimes, secure digital-ID systems, and modernised payment infrastructure to ensure that digital finance improves welfare rather than amplifying fraud and cyber risk.

Platform Risk and Inclusion Durability

The substitute-bank model built around exchanges like Binance is powerful but platform-dependent. Users rely on a single intermediary for custody, on-ramp and off-ramp access, and often for yield — concentrating counterparty and operational risk. In the event of platform outages, regulatory actions, or security incidents, millions of EM users could lose access to what has effectively become their primary financial account.

Mitigating this risk likely requires a combination of:

Self-custodial wallets for direct on-chain ownership.

Regulated custodial solutions with transparent reserve disclosures.

Diversified stablecoin access venues to prevent single-provider dependency.

Interoperable identity and messaging standards to prevent vendor lock-in and improve user resilience across platforms.

Implications and Forward-Looking Themes

For Policymakers and Development Institutions

The data suggests that crypto rails — and stablecoins in particular — should now be treated as core components of the financial-inclusion toolkit rather than fringe experiments. Concrete integration points include:

Using stablecoins or tokenised deposits in government-to-person transfer programmes.

Enabling regulated stablecoin remittance channels with AML/KYC compliance built in.

Recognising on-chain savings products within prudential and consumer-protection regimes.

Development institutions already advocating for digital public infrastructure — digital IDs, instant-payment systems, interoperable wallets — can extend this work to on-chain settlement, ensuring low-income users benefit from the same cost efficiencies that AI agents and high-frequency traders already enjoy.

For Exchanges and Builders

For platforms like Binance, the report's findings reinforce a strategic pivot from pure trading venue to a multi-product financial super-app for EM users. Product roadmaps emphasising stablecoin savings, low-cost remittances, tokenised RWAs, and simple mobile-first UX will likely capture the fastest-growing segments of demand.

Key opportunity areas for builders include:

Remittance-optimised corridors — predictable fees and clear compliance pathways for the highest-volume low-income routes.

Simple savings vaults — yield-bearing instruments packaged behind stablecoin wrappers accessible to non-expert users.

Tokenised capital-market access — global equities, credit, and RWAs with regulatory-compliant KYC/AML tailored for EM contexts.

AI-assisted financial tools — automated savings, smart remittance scheduling, and personalised portfolio guidance for users with limited financial literacy.

For Users and Advocates

For users in EMs, the practical takeaway is direct: a smartphone plus a stablecoin-enabled wallet or exchange account can already replicate many functions of a bank account — storing value, sending and receiving funds globally, and accessing basic investment products that local banks cannot offer.

Advocates for financial inclusion can leverage this narrative — anchored in hard numbers on adoption, savings behaviour, and cost differentials — to argue for supportive, risk-proportionate regulation rather than blanket prohibitions.

Conclusion

The trajectory toward stablecoin-powered financial inclusion is not guaranteed. It depends on regulatory clarity, the resilience of stablecoin infrastructure under stress, and whether the cost efficiencies demonstrated on permissionless networks eventually force incumbents to match them. What the evidence does support, clearly and consistently, is that platforms like Binance are already operating as bank substitutes for tens of millions of people — and that stablecoins are the instrument making that substitution possible at scale.

The convergence of rising smartphone penetration, near-zero-cost on-chain settlement, and growing EM demand for dollar-denominated savings creates a structural opportunity that is unlikely to reverse. For the 1.3 billion still outside the formal financial system, that convergence may represent the most accessible on-ramp to economic participation the world has yet produced.