Executive overview

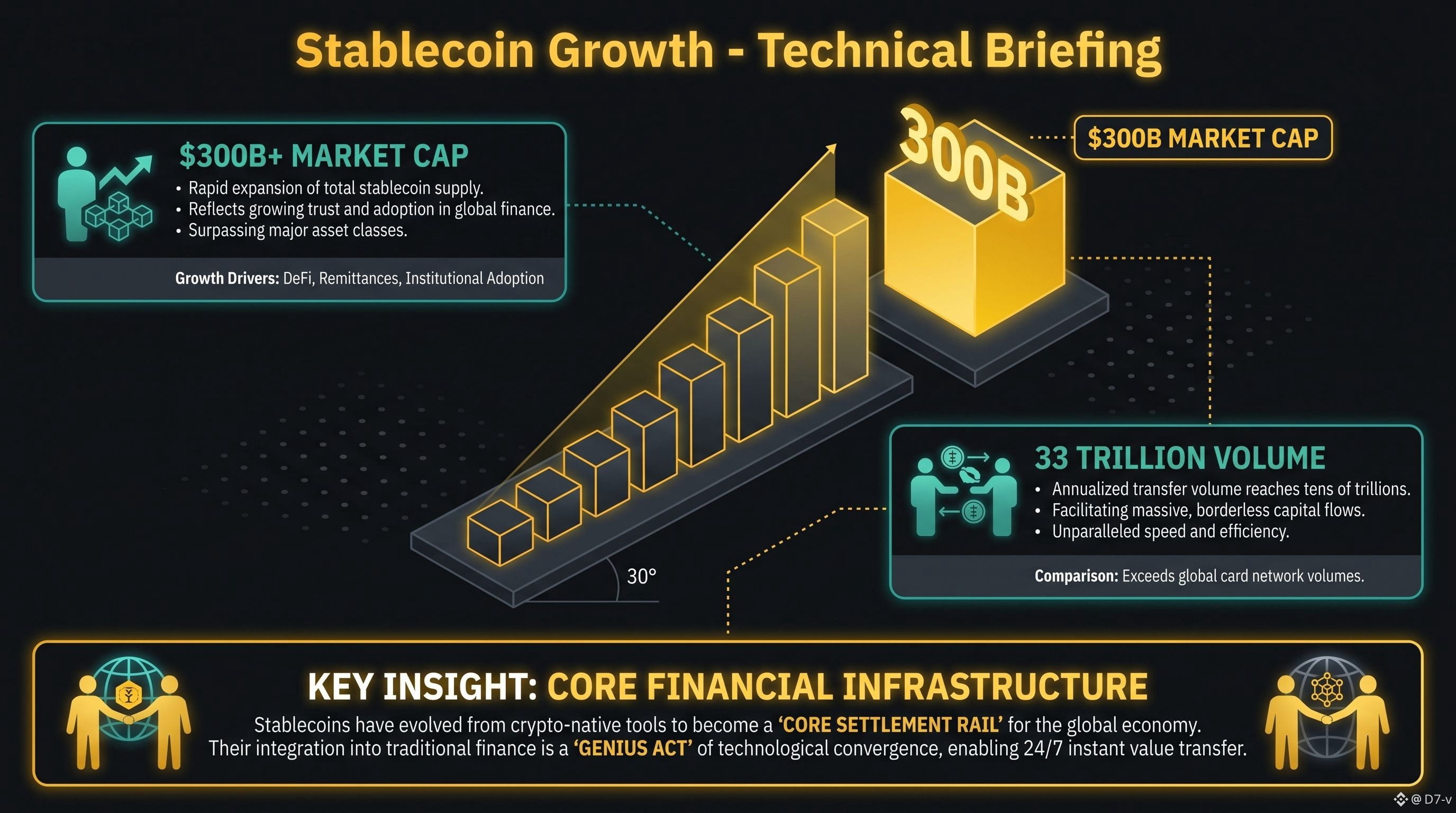

The stablecoin market has decisively moved past the proof‑of‑concept phase: total circulating supply has cleared the 300 billion mark, with multiple data providers placing market cap in the 300–310 billion range in early 2026. Transfer volumes are now measured in the tens of trillions of dollars annually, signaling that stablecoins already function as a core settlement rail inside the crypto ecosystem and increasingly in traditional finance.

At the same time, regulation has flipped from uncertainty to structured regimes in the U.S. (GENIUS Act), European Union (MiCA), and several Asian hubs, all converging on a model of fully‑reserved, redeemable “payment stablecoins.” This legal clarity is unlocking a new growth wave centered on payments, payroll, cross‑border settlement, and embedded finance, rather than just trading and DeFi yield.

1. From trading chips to financial plumbing

1.1 Market cap and volumes beyond speculation

Multiple independent sources confirm that total stablecoin market capitalization moved above 300 billion between late 2025 and early 2026, with DeFiLlama and other trackers cited at roughly 301–309 billion and Binance commentary pointing to about 310 billion as of January 2026. One trend report estimates total stablecoin transfer volume at around 33 trillion in 2025 alone, depending on methodology, underscoring the scale at which these tokens already clear value.

The 2026 Stablecoin Momentum Report from infrastructure provider zerohash characterizes this shift as moving from “crypto‑native experimentation into core financial infrastructure,” highlighting that active stablecoin usage and transaction volumes on their platform grew triple‑ to high‑triple‑digit percentages year‑over‑year. In parallel, survey data and market analyses show that stablecoins are now used for brokerage funding, cross‑border settlement, global payroll, and treasury operations alongside trading and DeFi.

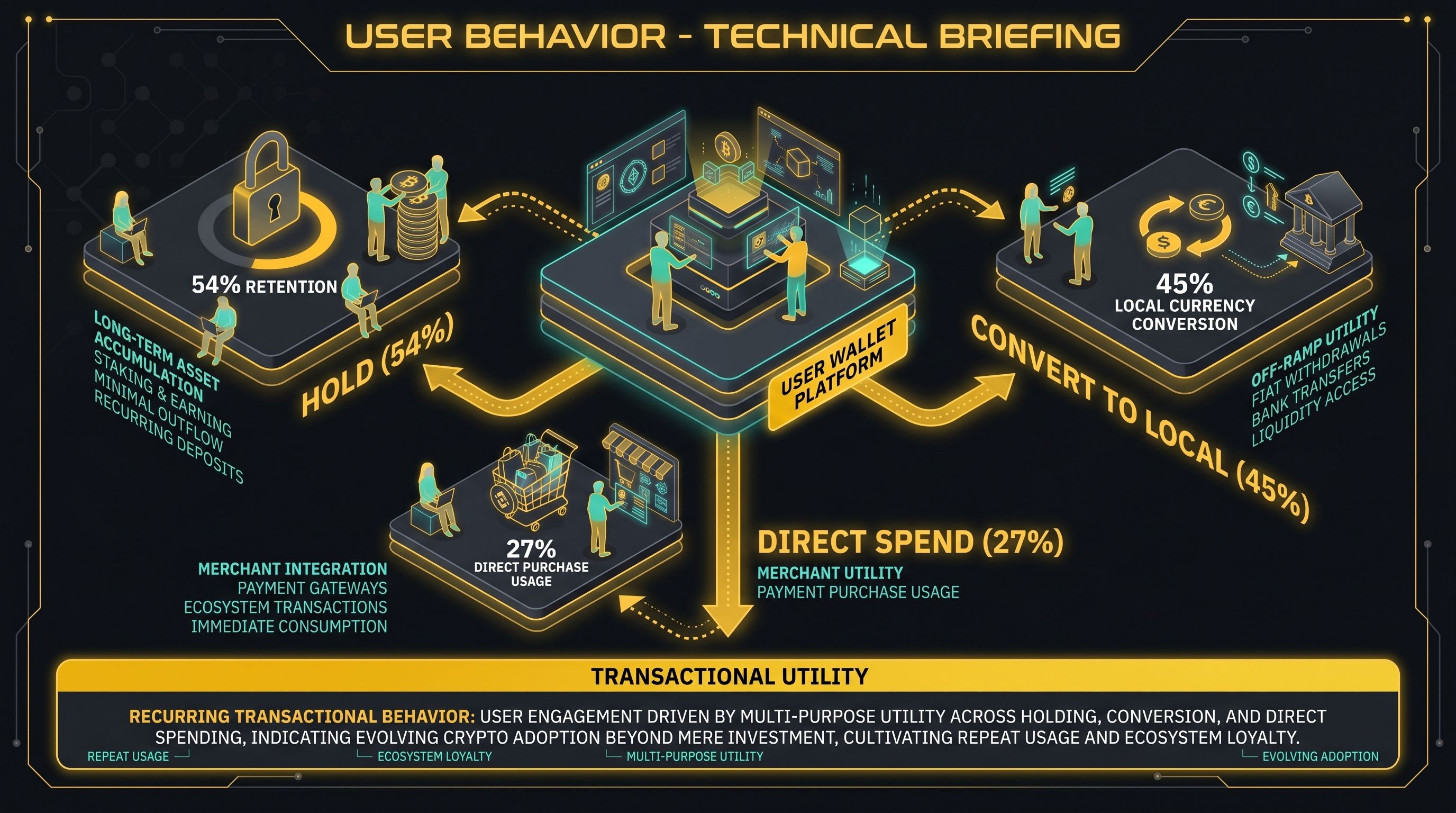

1.2 User behavior: hold, convert, or spend

Survey work in early 2026 suggests that stablecoins are becoming embedded in everyday financial activity, not just speculative portfolios. In one “Stablecoin Utility Report 2026” based on a 15‑country survey of more than 4,600 adults, 54 percent of respondents had held stablecoins in the past year and 56 percent of current holders planned to increase usage. Among these users, 45 percent reported converting stablecoins to local currency, while 27 percent used them directly for purchases of goods and services, and 28 percent converted or spent within days of receipt, indicating transactional rather than purely savings behavior.

Another survey from BVNK and YouGov found that 39 percent of respondents now receive payments in stablecoins and that roughly half increased their holdings in the previous year. Crucially for the “embedded” thesis, 77 percent said they would open a crypto or stablecoin wallet inside their existing bank or fintech app if offered, suggesting that banks and super‑apps adding stablecoin rails can tap latent demand rather than having to recruit entirely new user cohorts.

2. The regulatory flip: GENIUS, MiCA, and beyond

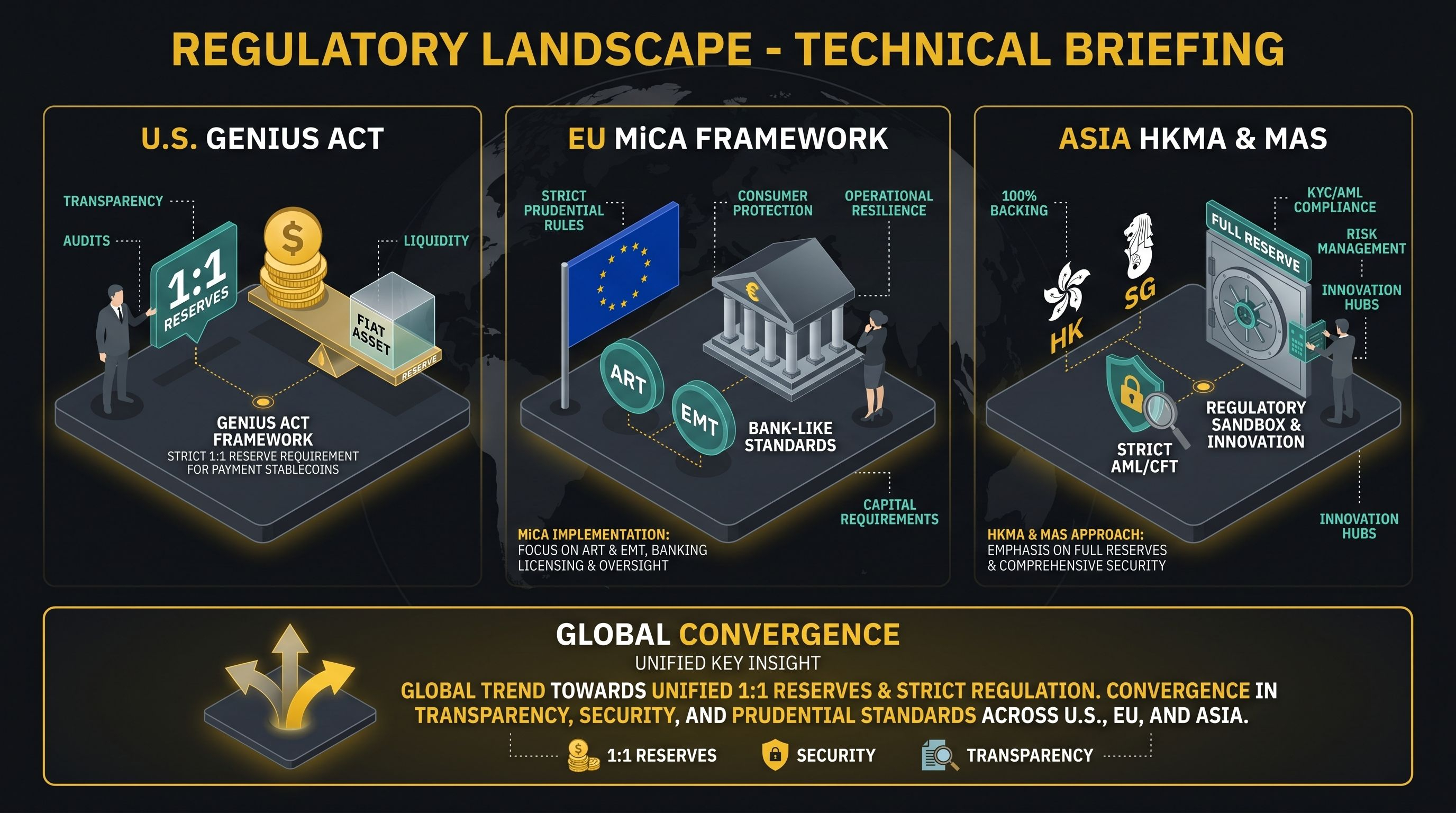

2.1 The GENIUS Act: U.S. payment stablecoins

The U.S. GENIUS Act (Guaranteeing Essential National Infrastructure in U.S. Stablecoins) is the first comprehensive federal framework specifically targeting payment stablecoins. It requires issuers to:

Maintain 1:1 reserves in high‑quality, liquid assets such as cash, Treasury bills, and certain repurchase agreements, subject to regular audits.

Provide monthly reserve disclosures and CEO/CFO certifications, alongside clear redemption policies.

Operate as regulated financial institutions (insured depository institutions or OCC/state‑chartered entities) and comply fully with Bank Secrecy Act, AML, and CFT rules.

The Richmond Fed’s guidance notes that the GENIUS Act formally defines payment stablecoins, distinguishes them from securities and commodities, and prohibits interest‑bearing consumer stablecoin products, reflecting regulators’ preference for narrow‑purpose, money‑like instruments rather than investment products. Policymakers and Treasury officials have publicly suggested that under this framework, the U.S. stablecoin market could expand to well over 2 trillion in coming years, implying an order‑of‑magnitude scale‑up if adoption continues.

2.2 MiCA: Europe’s ART/EMT regime

In the European Union, the Markets in Crypto‑Assets (MiCA) framework is fully in effect, with its strictest rules targeting stablecoins, classified as Asset‑Referenced Tokens (ARTs) and E‑Money Tokens (EMTs). MiCA requires issuers to be authorized credit institutions or e‑money institutions, maintain fully backed, segregated reserves, and provide redemption rights, while imposing capital, transparency, governance, and recovery‑and‑resolution requirements that resemble bank prudential standards.

MiCA’s stablecoin provisions (Titles III and IV) have applied since June 30, 2024, and effectively prohibit algorithmic stablecoins that lack 1:1 liquid backing. Market commentary notes that CASPs in Europe have rotated toward MiCA‑compliant euro and dollar stablecoins, with over 90 firms authorized as crypto‑asset service providers and a diversification of e‑money token issuers, including more traditional financial institutions entering the market under the harmonized rulebook.

2.3 Asia and global coordination

Beyond the U.S. and EU, several Asian jurisdictions are rolling out or refining dedicated stablecoin regimes. Hong Kong’s Stablecoin Ordinance, passed in 2025, requires stablecoins backed by the Hong Kong dollar to be fully reserved, licensed by the Hong Kong Monetary Authority, and subject to strict AML/CFT, audit, and disclosure requirements. Singapore is similarly finalizing stablecoin legislation to sit alongside its broader digital asset rules, and global bodies such as the Financial Stability Board and FATF are preparing additional guidance on risk management, recovery planning, and cross‑border supervision.

Chainalysis highlights that even where rules exist, supervisors still see gaps around capital buffers, risk management, and resolution planning, suggesting a continued tightening cycle through at least 2026–2027. However, the overriding picture is convergence: most major hubs now treat payment stablecoins as a regulated form of money, not as unregulated crypto tokens, which reduces legal risk for banks, corporates, and fintechs that want to integrate them.

3. Why the next wave is payments, not trading

3.1 Structural shift in use cases

Historically, stablecoins grew as a hedge against exchange volatility and a base asset for spot and derivatives trading. By 2025–2026, the data shows a clear broadening into payments, payroll, and treasury. The zerohash report notes that stablecoins now underpin brokerage funding, cross‑border settlement, global payroll, and day‑to‑day treasury operations in addition to trading. Survey evidence that 39 percent of respondents receive income in stablecoins and that more than a quarter spend or convert within days indicates recurring, payroll‑like patterns rather than intermittent speculative flows.

The high proportion of users willing to access stablecoins directly inside banking and fintech apps (over three‑quarters in one survey) implies the next growth leg will be distribution through existing financial front‑ends, where users already keep balances and transact frequently. That is a fundamentally different dynamic from the 2017–2021 cycle, which relied on users opening specialist crypto accounts primarily for trading.

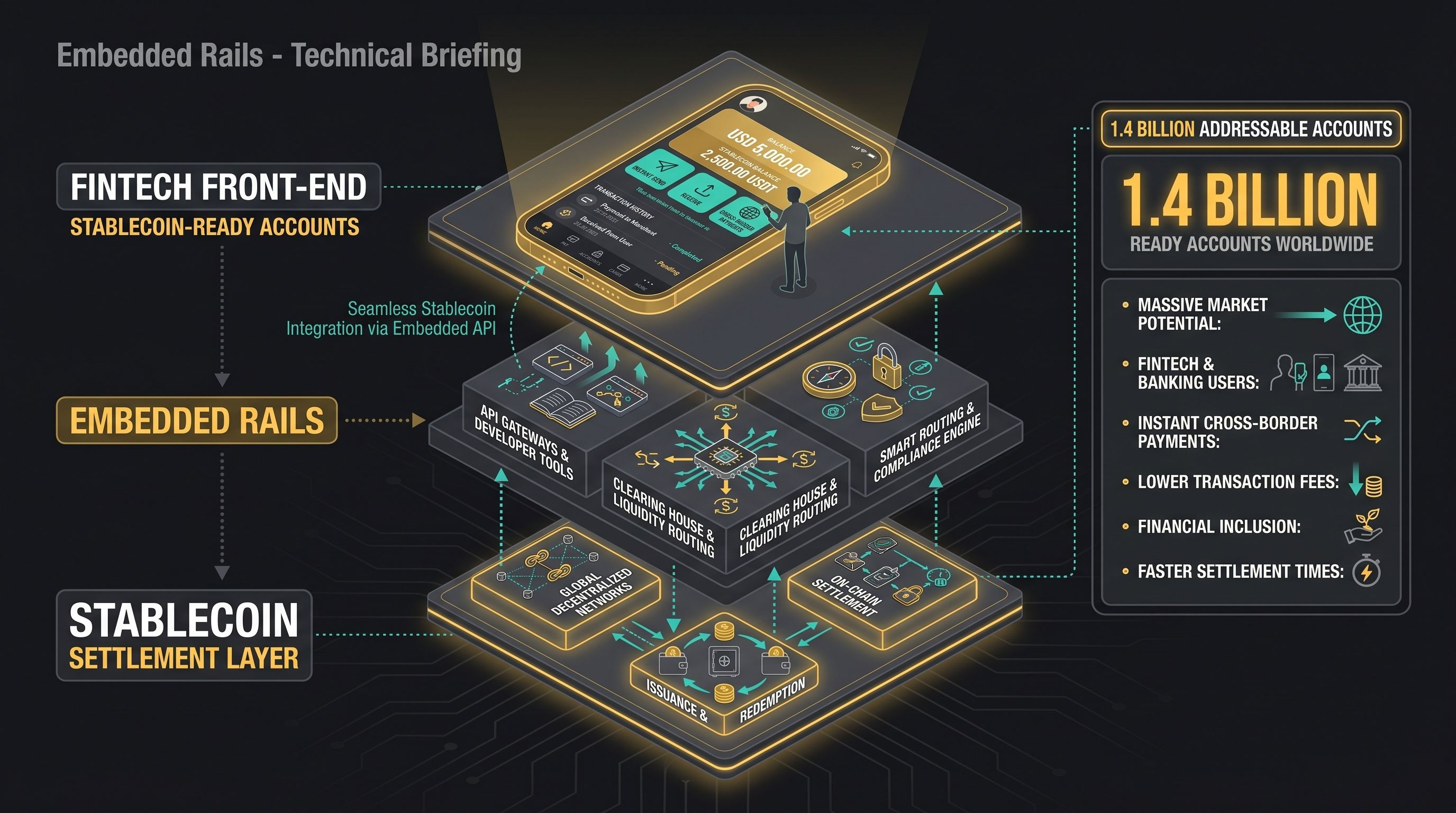

3.2 Embedded rails and “stablecoin‑ready accounts”

zerohash introduces the concept of “Stablecoin‑Ready Accounts” (SRAs): consumer accounts on mainstream platforms where stablecoin functionality is live or being enabled. The firm estimates more than 1.4 billion such accounts globally, suggesting that the addressable base for stablecoin‑powered payments is already at near‑internet scale if product teams choose to switch it on.

Within this footprint, active stablecoin usage grew 146 percent year‑over‑year while transaction volume expanded 690 percent, implying both higher frequency of use and movement into larger‑ticket flows such as B2B settlement and treasury operations. The report also notes a sharp increase in RFIs related to stablecoins from enterprises and financial institutions, reflecting demand to embed stablecoin rails into existing workflows.

3.3 Regulatory clarity reduces counterparty risk

The GENIUS Act’s requirement for full, audited reserves, clear redemption rights, and strict AML/CFT compliance reduces the legal and credit risk that previously limited banks and corporates from touching stablecoins. MiCA’s similarly stringent framework for ARTs and EMTs gives European institutions a harmonized, pan‑EU rulebook, while Hong Kong and other Asian regimes offer regional clarity.

Chainalysis points out that Europe has already seen a rotation into MiCA‑compliant stablecoins, including more euro‑denominated options, and that the GENIUS Act’s implementing regulations will further institutionalize payment stablecoins in the U.S. by 2027. Together, these regimes transform stablecoins from a “gray area” tool into a recognized form of electronic money, enabling their inclusion in corporate treasury policies, payment network rules, and regulated financial products.

4. Binance and reserve‑backed stablecoins as infrastructure

4.1 Reserve transparency and FDUSD

Binance’s public communications emphasize full reserve backing and independent attestation as non‑negotiable for the stablecoins it supports at scale. In 2025, Binance reported that FDUSD’s reserves stood at just over 2.05 billion dollars as of March 1, 2025, held in U.S. Treasuries and overnight fixed deposits, exceeding the token’s circulating supply and confirming its ability to redeem 1:1 for dollars. Earlier communications stressed that reserves were strategically held in high‑quality, liquid assets, including U.S. Treasury bonds and overnight deposits, with attestation reports verifying that reserves exceeded circulating supply.

Third‑party coverage likewise notes that Binance confirmed FDUSD could be fully supported with a 1:1 reserve, meaning each unit is backed by an equivalent dollar asset. This model closely mirrors the GENIUS and MiCA expectations for payment stablecoins—high‑quality reserves, clear redemption, and audited transparency—and positions such tokens as compliant building blocks for payments infrastructure.

4.2 How exchanges become payment hubs

As regulatory regimes mature, large exchanges and brokerages are moving from pure trading venues to multi‑product financial platforms. Binance’s own commentary on the stablecoin market crossing 310 billion frames stablecoins as the “financial backbone” of the crypto ecosystem, supporting trading, DeFi, and an expanding range of payment and settlement use cases.

When exchanges combine:

Deep stablecoin liquidity across spot, derivatives, and on‑chain liquidity pools;

Reserve‑backed, compliant stablecoins that meet GENIUS/MiCA‑style requirements;

Consumer products like P2P, merchant tools, and card programs;

they effectively function as global FX and settlement hubs between fiat banking systems and always‑on stablecoin rails. This allows users and businesses to treat stablecoins as working capital and settlement currency, not just as trading collateral.

5. Key payment‑driven growth verticals

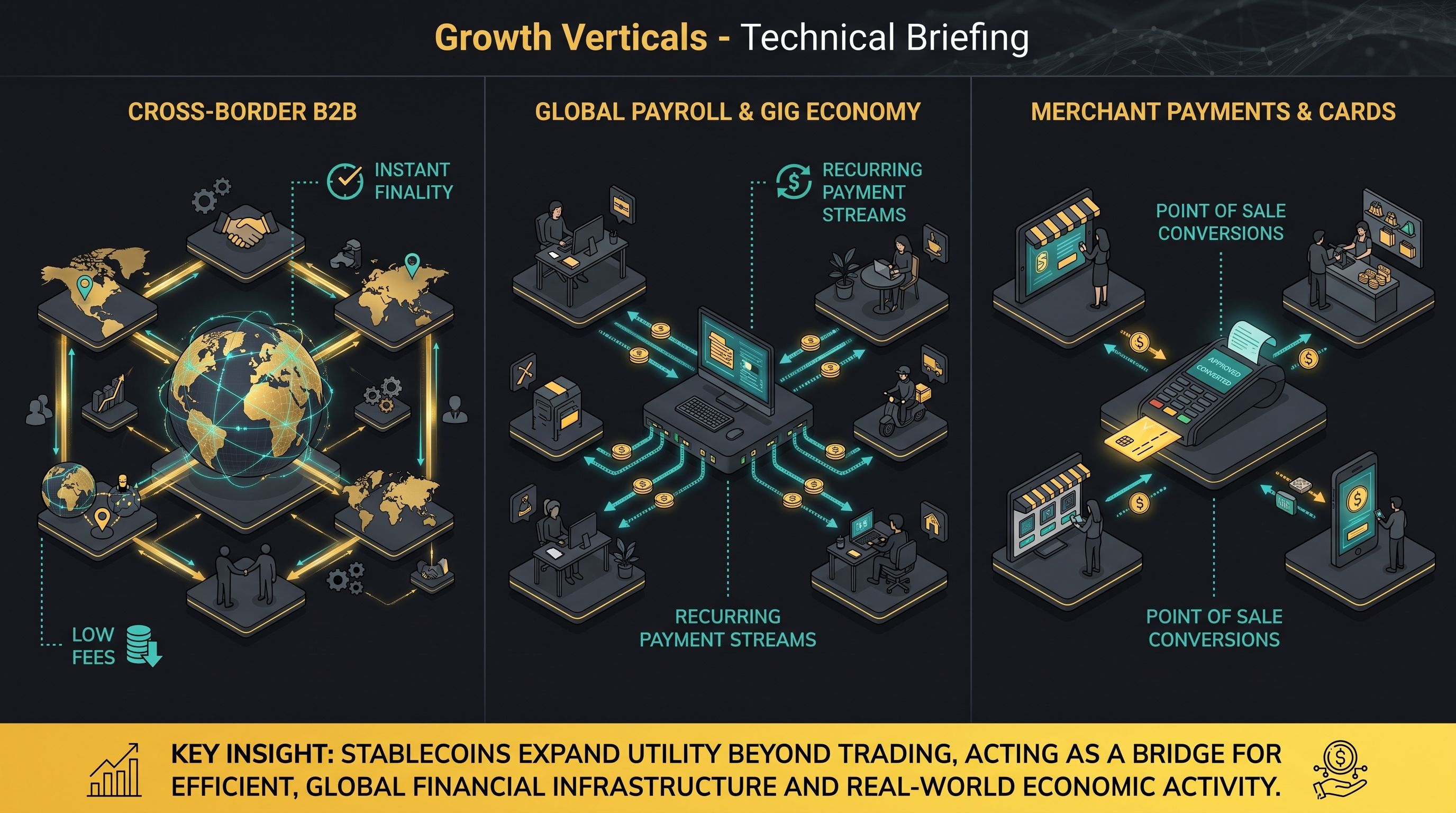

5.1 Cross‑border remittances and B2B settlement

Stablecoins are structurally well‑suited for cross‑border remittances: 24/7 availability, near‑instant finality, and low network fees compared with wire transfers or legacy remittance channels. Industry reports now explicitly highlight the role of stablecoins in cross‑border flows, with user surveys showing significant adoption of stablecoins to receive income and make purchases internationally.

On the B2B side, infrastructure providers report that stablecoins are used for cross‑border settlement between brokers, fintechs, and corporates, with volume growth far outpacing simple user‑count growth. This pattern is consistent with enterprises moving larger flows—such as supplier payments, treasury rebalancing, and inter‑affiliate transfers—onto stablecoin rails once initial pilots prove reliable.

5.2 Payroll, gig economy, and global talent

Survey data indicating that roughly 39 percent of respondents receive payments in stablecoins, combined with evidence that many spend or convert shortly after receipt, strongly suggests payroll and gig‑economy usage. This is particularly compelling for globally distributed teams, freelancers, and creators whose income sources span multiple jurisdictions.

Platforms that integrate stablecoin payouts can reduce friction and fees for cross‑border compensation, while workers can choose between holding dollar‑pegged balances or converting into local currency, often at better FX rates than those offered by traditional rails. As “stablecoin‑ready accounts” expand inside mainstream neobanks and brokerages, this payroll use case is likely to scale quickly.

5.3 Merchant payments and cards

The Stablecoin Utility Report 2026 finds that 52 percent of surveyed users have made a purchase specifically because a business accepted stablecoins, and 71 percent would be likely to use a debit card linked to their stablecoin balance, rising to 78 percent in low‑ and middle‑income economies. This points to both direct on‑chain payments (e.g., QR or address‑based) and card‑based experiences where stablecoin balances are converted at point of sale.

For merchants, stablecoin acceptance can reduce chargeback risk, settlement time, and FX complexity, especially for cross‑border e‑commerce. For users, paying from a stablecoin balance turns crypto wallets and exchange apps into everyday spending accounts, deepening engagement beyond sporadic trading.

6. Design implications for builders

6.1 Product principles for payment‑first stablecoins

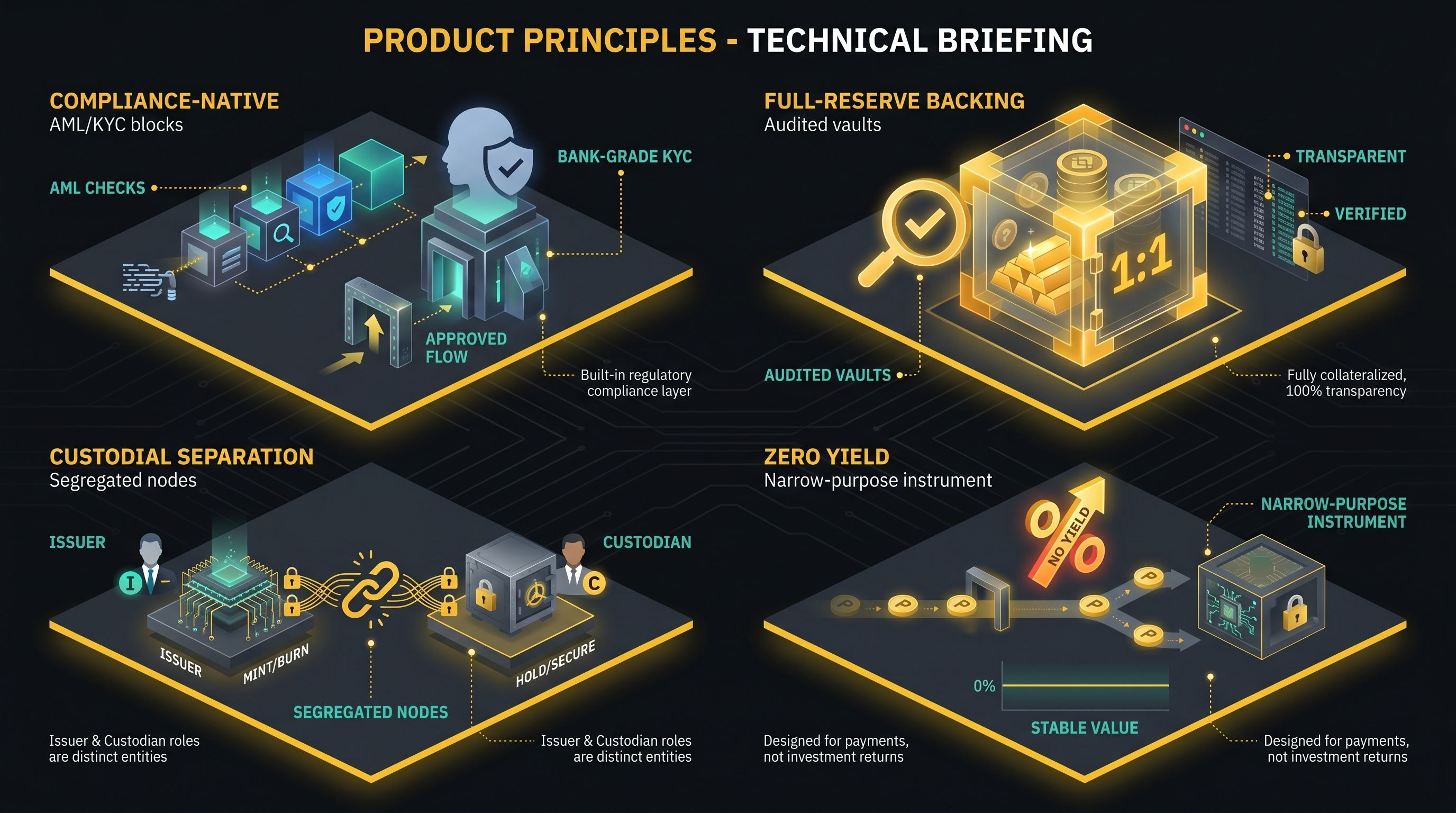

The regulatory and usage data suggest several design principles for payment‑focused stablecoin products and apps:

Compliance‑native architecture: GENIUS, MiCA, and Hong Kong’s regimes all assume bank‑grade KYC, AML, and Travel Rule compliance, with clear issuer accountability.

Full‑reserve, transparent backing: Monthly attestations, independent audits, and granular reserve reporting will be table stakes, not differentiators.

Issuer and custodian separation: MiCA explicitly requires reserves to be held by independent, regulated custodians, limiting commingling and operational risk.

No yield on payment coins: Both MiCA and GENIUS prohibit paying interest on core payment stablecoins, forcing yield‑seeking designs into separate, clearly labeled products.

Builders who bake these assumptions into their technical and legal architecture from day one will find it easier to integrate with banks, PSPs, and regulators than projects that treat compliance as an afterthought.

6.2 UX: hiding the crypto, highlighting the benefits

Survey evidence that users want stablecoin functionality embedded in existing bank or fintech apps points to a key UX principle: the crypto should be invisible. Users care about faster, cheaper, and more reliable payments, not about token standards or chain names.

Winning products will likely:

Show balances and transactions in familiar fiat terms while using stablecoins under the hood;

Automate on/off‑ramping and FX, so users never see order books or swap screens;

Offer familiar primitives—accounts, cards, invoices, payroll—backed by stablecoin settlement.

This is already visible in how some exchanges and fintechs describe stablecoins as “digital dollars” or “borderless cash,” emphasizing utility over crypto branding.

7. Strategic outlook: toward a stablecoin settlement layer

7.1 Macro trajectory

Stablecoin market capitalization has moved from near zero a decade ago to more than 300 billion in early 2026, while transfer volumes have grown to tens of trillions annually. Regulatory clarity is spreading across major jurisdictions, and both survey data and infrastructure reports show rising adoption in payments, payroll, and B2B flows.

Against this backdrop, several policymakers and industry observers now frame stablecoins as the backbone of a future global settlement layer: always‑on, interoperable dollar (and euro/other fiat) rails that sit alongside domestic banking systems rather than replacing them. Exchanges, fintechs, and banks that position themselves as conversion and liquidity hubs into and out of these rails stand to benefit disproportionately from the next growth wave.

7.2 What could derail the thesis

Key risk factors include:

Regulatory overreach or fragmentation: Divergent rules, caps on stablecoin size, or restrictive licensing could limit scale in key markets.

Major depeg or failure: A large stablecoin “breaking the buck” remains a core concern for regulators, who see it as a potential trigger for broader financial instability.

Infrastructure incidents: Smart‑contract exploits, chain outages, or custodial failures could undermine trust, particularly if they affect regulated, widely used tokens.

Regimes like MiCA and GENIUS are explicitly designed to mitigate some of these risks via prudential standards and recovery plans, but execution quality by issuers and custodians will ultimately determine real‑world resilience.

8. Takeaways for market participants

For traders and DeFi users, the shift toward payments does not reduce the role of stablecoins as collateral; instead, it anchors their value in real‑economy demand and regulated frameworks, which can make them more resilient over cycles. For builders and institutions, the message is clear: the largest remaining opportunity is not creating yet another trading‑centric stablecoin, but wiring existing financial flows—remittances, payroll, B2B settlement, and merchant payments—onto the stablecoin rails that already exist.

As stablecoins scale beyond 300 billion in supply under increasingly bank‑like regulation, the line between “crypto infrastructure” and “financial infrastructure” is disappearing. The next wave of growth will belong to those who treat stablecoins not as tokens to be speculated on, but as programmable, interoperable money that can quietly power the world’s payments behind the scenes.