If you have ever looked at a storage protocol and wondered, “Where does the yield actually come from, and who is paying for it?”, Walrus is a good case study. Its incentive model is not built around short term farming rewards. It is built around a delegated proof of stake committee that gets paid for doing real work: storing data, proving availability, and serving it back when needed. The tokenomics of WAL is basically a set of rules that tries to keep three groups aligned over time: storage node operators, WAL stakers, and the apps and users who pay to store data.

Walrus is tightly integrated with the Sui blockchain for coordination, payments, and object based accounting. Storage space and stored blobs are represented on chain, and the smart contracts on Sui are the layer that mediates staking, epoch changes, and reward distribution. This matters for traders because it means the “business model” of the token is not abstract. WAL is used to delegate stake, to help select the storage committee, and to pay for storage. At the end of every epoch, rewards for storing and serving blobs are distributed to storage nodes and to the people who staked with them. So the basic return source is not inflation alone. It is also the flow of storage fees moving through the system.

The cleanest date to anchor Walrus’s token lifecycle is March 27, 2025. DefiLlama’s unlock schedule shows a major event on that date, including the Walrus User Drop allocation. Walrus’s own staking guide is also dated March 27, 2025, which lines up with the period the protocol started pushing staking as a core activity. In other words, that window is effectively the launch era that traders tend to treat as the start of the live token economy.

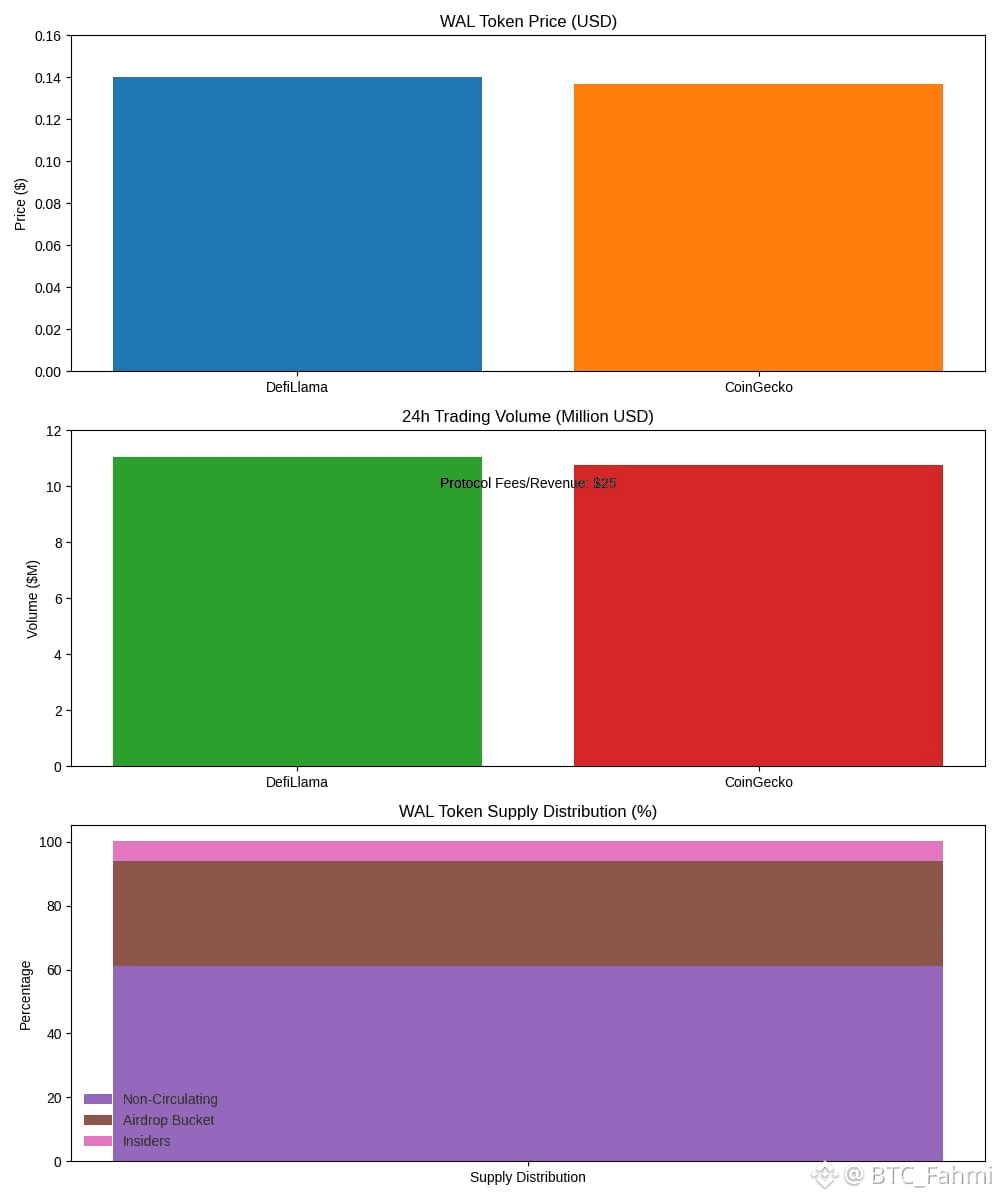

From a supply and distribution point of view, the big thing to understand is that WAL is not mostly circulating yet. DefiLlama’s unlock page shows the current state as 61 percent non circulating, with 32.9 percent attributed to the airdrop bucket and 6.2 percent insiders at that snapshot in time. The same page also shows a “final” target view where insiders reach 30 percent and private sale reaches 7 percent. That does not mean insiders suddenly receive 30 percent tomorrow. It means over time, vesting and unlocks move the system toward that final allocation. For investors, this is one of the most practical parts of tokenomics: if you are trading WAL, you are trading an asset that still has a large portion of supply scheduled to enter the market over time.

Now to the incentive model itself, because that is what really drives behavior. Walrus is operated in epochs. In each epoch, a committee of storage nodes is selected, influenced by how much stake is delegated to them. Users delegate WAL to storage nodes, which helps determine committee selection and shard assignments, roughly proportional to delegated stake. The incentive is simple: nodes want stake because stake increases the chance of being selected and earning, and delegators want nodes that perform well because they share in the rewards funded by storage fees.

Withdrawal speed is an important risk control detail, and Walrus is explicit about it. Unstaking is not instant. If you request a withdrawal before the midpoint of an epoch, funds can become available at the start of the next epoch. If you request after that midpoint, you may need to wait until the following epoch. Since Walrus staking rewards are calculated per epoch, and at least one guide notes epochs are about two weeks, this effectively means you should mentally model withdrawals as taking roughly one to four weeks depending on timing. For traders, that delay is not a minor footnote. It creates a liquidity constraint during volatility, and it is part of how the protocol reduces sudden stake flight.

The next part of risk control is slashing and burn mechanics. Walrus uses economic penalties to discourage bad behavior and short term stake hopping. Some sources describing Walrus mechanics point to churn fees when stakers move stake between nodes, plus slashing penalties on underperforming nodes, with part of those penalties being burned. Whether that burn becomes a meaningful long term supply sink depends on real usage, because the protocol’s main economic loop is still storage demand.

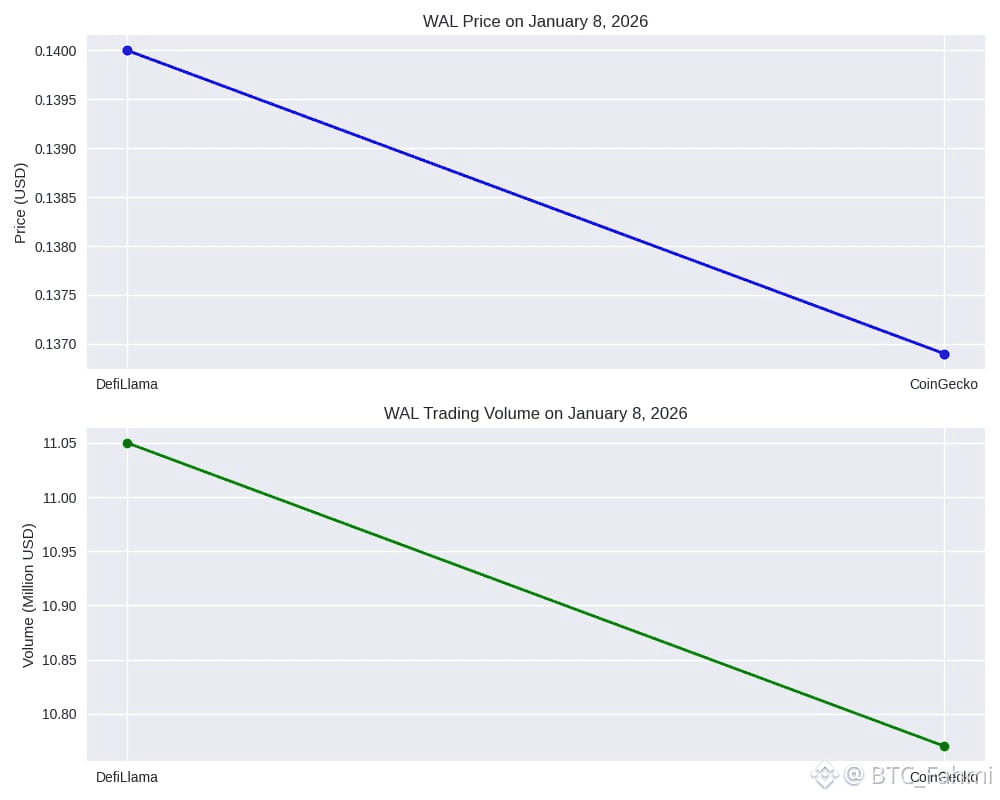

So what do today’s live numbers look like for market activity. On January 8, 2026, DefiLlama shows WAL price around $0.14 with a 24 hour token trading volume of about $11.05 million, split between centralized and decentralized activity in their breakdown. CoinGecko’s live tracker on the same date shows WAL at about $0.1369 and 24 hour trading volume around $10.77 million, which is broadly consistent given data source differences. DefiLlama also reports protocol fees and revenue, which is the closest thing you can treat as “fundamentals” in the incentive model. In the last 24 hours, DefiLlama shows Walrus Protocol fees and revenue at about $25. That is small relative to market volume, and that contrast is a useful reality check: WAL’s trading activity can be far larger than the underlying fee flow on some days, which is common in early stage infrastructure tokens.

About TVL, there is a nuance traders should not ignore. Walrus is a storage protocol, not a lending or liquidity protocol, so TVL is not always the main metric or even consistently reported the way it is for DeFi apps. DefiLlama’s Walrus Protocol page focuses on fees, revenue, earnings, and token stats rather than presenting a headline TVL figure. If you see a “TVL” label on third party dashboards, it is often measuring something closer to staking deposits or contract balances rather than user liquidity in the classic DeFi sense. When you are analyzing Walrus’s incentive model, the more direct on chain value signals are storage fee generation, delegation concentration, committee performance, and unlock schedules.

The most important trend to watch going forward is whether real storage demand grows enough to make fee funded rewards a meaningful portion of returns. DefiLlama’s methodology notes that fees come from users paying for data storage, and revenue is locked and distributed over time to storage providers. That is a real economic loop, but it scales only if apps consistently pay to store data on Walrus. If usage grows, the incentive model becomes more self sustaining and less dependent on emissions. If usage is slow, traders should expect staking yields to lean more heavily on token emissions while the market digests ongoing unlocks.

From a neutral investor standpoint, Walrus’s incentive model has a straightforward long term logic: stake selects the committee, the committee stores and serves data, users pay storage fees, and fees are distributed through epochs to nodes and delegators. The key risks sit in three places: unlock driven supply increases over time, withdrawal delays that limit liquidity during stress, and adoption risk where real fee flow may lag speculative interest. If you track those three consistently, you will understand the real incentives better than most traders who only look at price and volume.