Most people start investing with excitement. They see charts going up stories of fast money and numbers that look life changing. Fifteen percent sounds realistic. Twenty percent feels possible. Over time these numbers stop sounding aggressive and start feeling normal. That is where confusion begins.

The truth is returns are not just about the asset. They are about the investor. Two people can invest in the same market at the same time and still end up with very different results. The difference usually has nothing to do with intelligence. It comes down to patience timing and emotional control.

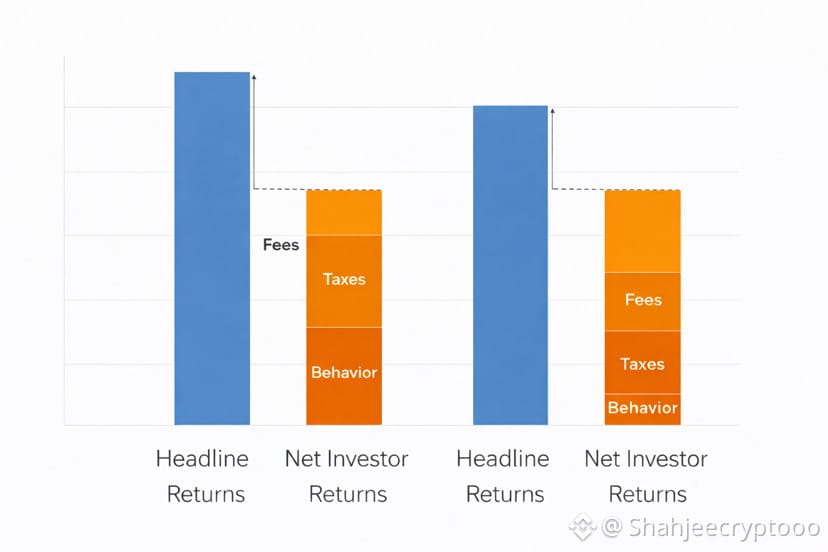

One of the biggest misunderstandings is the difference between theoretical return and lived return. Theoretical return assumes perfect behavior. Buy at the right time. Hold through every drawdown. Never panic. Never need liquidity. In real life none of this happens. People sell when fear peaks and buy when confidence returns. This gap between theory and reality quietly eats away at performance.

Costs play a bigger role than most people expect. Fees taxes spreads and slippage look small individually but compound over time. A strategy that looks attractive on paper can lose its edge once these frictions are included. This is why many advertised returns never match what investors actually experience.

Risk is another word that is commonly misunderstood. Many think risk only means price volatility. In reality risk is the inability to stay invested. If an investment forces you to make decisions during stressful moments it becomes risky even if the long term chart looks strong. The best investments are often the ones that allow people to remain calm.

Liquidity is also ignored during good times. Everything feels liquid when markets are rising. The real test comes when everyone wants to exit at the same time. Assets that promised steady income can suddenly become hard to sell. At that moment the true cost of chasing yield becomes visible.

Passive income is often marketed as easy money. In practice passive income requires active thinking upfront. You need to understand how income is generated who pays it and what happens when conditions change. Income that depends on constant inflows or leverage tends to be fragile. Income backed by real usage and long term demand tends to last.

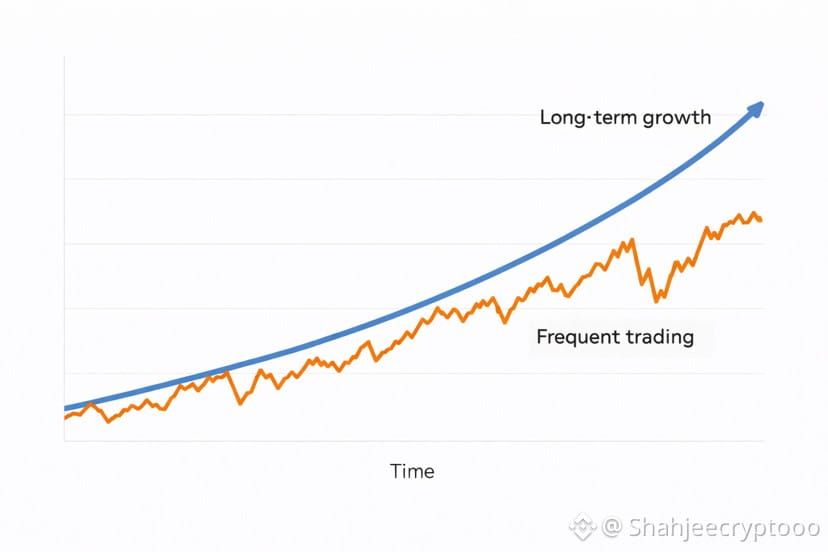

Another mistake investors make is constantly changing strategies. Switching feels productive but usually works against compounding. Every change resets the clock. Long term returns are built by staying invested through boring periods not by chasing excitement.

Time is the most underrated advantage an investor has. Not market timing but time spent invested. Markets reward consistency more than brilliance. The longer capital stays in the system the more forgiving mistakes become. Short term thinking removes this advantage completely.

In the end successful investing is less about finding the perfect asset and more about building a structure you can live with. A structure that survives stress slow periods and uncertainty. Wealth grows quietly when expectations are realistic and behavior is stable.

Most people do not fail because markets are unfair. They fail because expectations are misaligned. When expectations change outcomes often improve without changing the strategy at all.

#ZAMAPreTGESale #FedHoldsRates #WhoIsNextFedChair #TSLALinkedPerpsOnBinance #USIranStandoff