When we see an asset like silver lose nearly 30% in a single session, the natural reaction is to look for a fundamental cause. Yet, what happened recently shows that we are reliving the lessons of the past. What we observed was primarily a structural failure, a moment when the internal workings of the financial markets took over because, as with the Hunt brothers, the rules of the game changed mid-play.

⚠️ We must start with a key point that many underestimate: the global benchmark price for silver is determined by futures contracts traded on the COMEX within the CME Group. On these markets, you don't pay the full value of the metal you control. You deposit collateral, which allows you to use leverage. This system is at the heart of the liquidity of modern markets, but it is also their main point of vulnerability. As long as margin rules remain stable and volatility is contained, leverage acts as a performance amplifier, but as soon as the rules change, that same leverage becomes a stress amplifier.

📈 In mid-January, Sovanna_Sek and his associate warned investors of an initial rule change: the CME decided to switch from a fixed dollar margin system to a system where margin is expressed as a percentage of the contract value. In simpler terms, this means that the higher the price of silver rises, the higher the collateral required to maintain a position becomes. Following this, a second decision was made: faced with volatility, the CME repeatedly raised the required margin percentage. The result is a situation where, within a few days, the capital needed to maintain a long position in silver increases sharply, even without the price moving.

🤷♂️ Thousands of traders, funds, and trading desks had built long positions with a certain level of collateral in accordance with the previous rules. Overnight, these same positions become insufficiently hedged. As a result, brokers send margin calls, saying, "Either you provide additional cash or you reduce or close your positions." In an already strained environment, not everyone has unlimited liquidity. Many have no choice but to sell. These sales drive the price down, further worsening the situation for the most vulnerable accounts. New margin calls are triggered, and more sales follow, creating a self-perpetuating cycle because the lower the price falls, the more selling is forced.

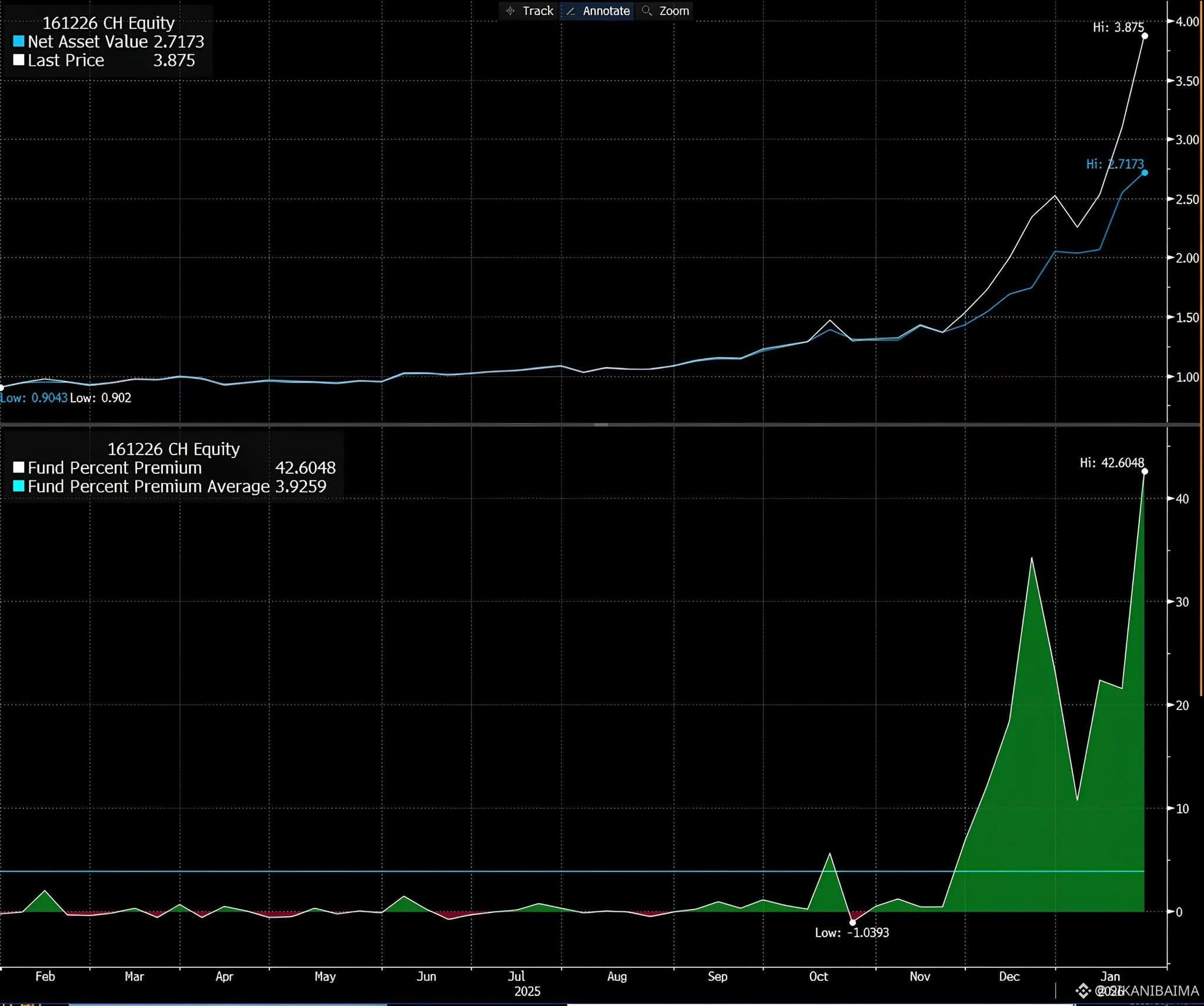

🇨🇳 Furthermore, direct access to Western futures and ETF markets is not as straightforward for Chinese investors. A significant portion of their silver exposure is therefore channeled through domestic products, notably a futures fund operated with UBS, which has become a central vehicle for gaining exposure to the metal over the months. However, local demand for silver exploded, and the supply of investment products capable of absorbing this demand remained limited. As a result, this fund began trading far above the value of its assets, with premiums of up to 40%. In other words, investors were willing to pay 1.40 for an asset that was economically worth 1. This demonstrates that people pay this type of premium when they are prepared to do anything to gain exposure, somewhat reminiscent of what happened recently with Bitcoin and MicroStrategy, for example, with the results we see today.

📉 The turning point came when the Shenzhen Stock Exchange decided to suspend trading of this fund for an entire day because Chinese investors were stuck. They held a product they couldn't sell, yet they remained exposed to silver, and many of them also had positions in international markets via COMEX futures. If they want to reduce their overall risk or obtain liquidity, the only solution is to sell what is still liquid elsewhere because these are the only remaining exit points. This results in two waves of selling, and when these two flows converge, the paper price plummets. The fundamentals clearly haven't changed. The rule changes have penalized the most aggressive and leveraged positions, just like when the Hunt brothers tried to corner the silver market.

It's always important to learn the history of finance.