The nomination of as the next Chair of the is not just another Washington headline. It is a signal that the entire policy framework markets have relied on since the post 2008 era could be entering a transition phase. Investors are not reacting to a person alone. They are reacting to what his arrival could represent for rates liquidity balance sheet policy and central bank independence.

This is why the reaction across bonds equities currencies and crypto has been fragmented rather than cleanly bullish or bearish. The Warsh nomination opens two competing paths and markets are struggling to decide which one dominates.

Why this nomination matters more than usual

Kevin Warsh is not an academic outsider or a symbolic political pick. He served as a Fed Governor from 2006 to 2011 and was directly involved during the global financial crisis. That period shaped his views and those views differ meaningfully from the post crisis consensus that dominated central banking for more than a decade.

Unlike the era associated with , which emphasized flexibility large scale asset purchases and market stabilization tools, Warsh has repeatedly argued that the Fed leaned too far into balance sheet expansion and blurred the line between monetary policy and fiscal support.

Markets understand this difference. That is why the nomination is being treated as a possible regime change rather than a routine leadership swap.

The political backdrop amplifying market sensitivity

The nomination comes at a time when central bank independence is already under scrutiny. The fact that publicly criticized Fed policy during his presidency adds another layer of complexity. Even if Warsh positions himself as independent the market must still price political pressure risk.

Senate resistance delays and procedural uncertainty matter because markets hate undefined timelines. A smooth confirmation would allow investors to quickly recalibrate expectations. A prolonged political standoff keeps volatility elevated and encourages defensive positioning particularly in duration sensitive assets.

This political fog is part of why the initial reaction has been choppy rather than directional.

Understanding Warsh’s policy mindset

To understand whether this nomination is bullish or bearish you have to separate short term rate expectations from long term liquidity dynamics.

Warsh has consistently questioned the long term consequences of quantitative easing. He has warned that oversized balance sheets distort price discovery inflate asset values and reduce policy credibility. That does not automatically make him a hawk but it does mean he may prioritize balance sheet normalization more aggressively than markets are used to.

At the same time he has also acknowledged that policy should respond to real economic conditions. If growth slows or disinflation accelerates he could support rate cuts earlier than expected. This is where the contradiction emerges and where markets are split.

The yield curve is the real battlefield

The cleanest way to see how investors are interpreting the nomination is through the Treasury yield curve.

Many participants are positioning for a steepening curve. This reflects expectations that short term rates may fall while long term yields remain elevated or even rise. That combination is powerful and dangerous at the same time.

If short rates fall because policy becomes more accommodative that is typically supportive for risk assets. But if long rates rise due to higher term premium or reduced central bank demand for bonds financial conditions can tighten even as the Fed cuts.

This is why the Warsh narrative is not a simple dovish or hawkish story. It is a mixed liquidity story.

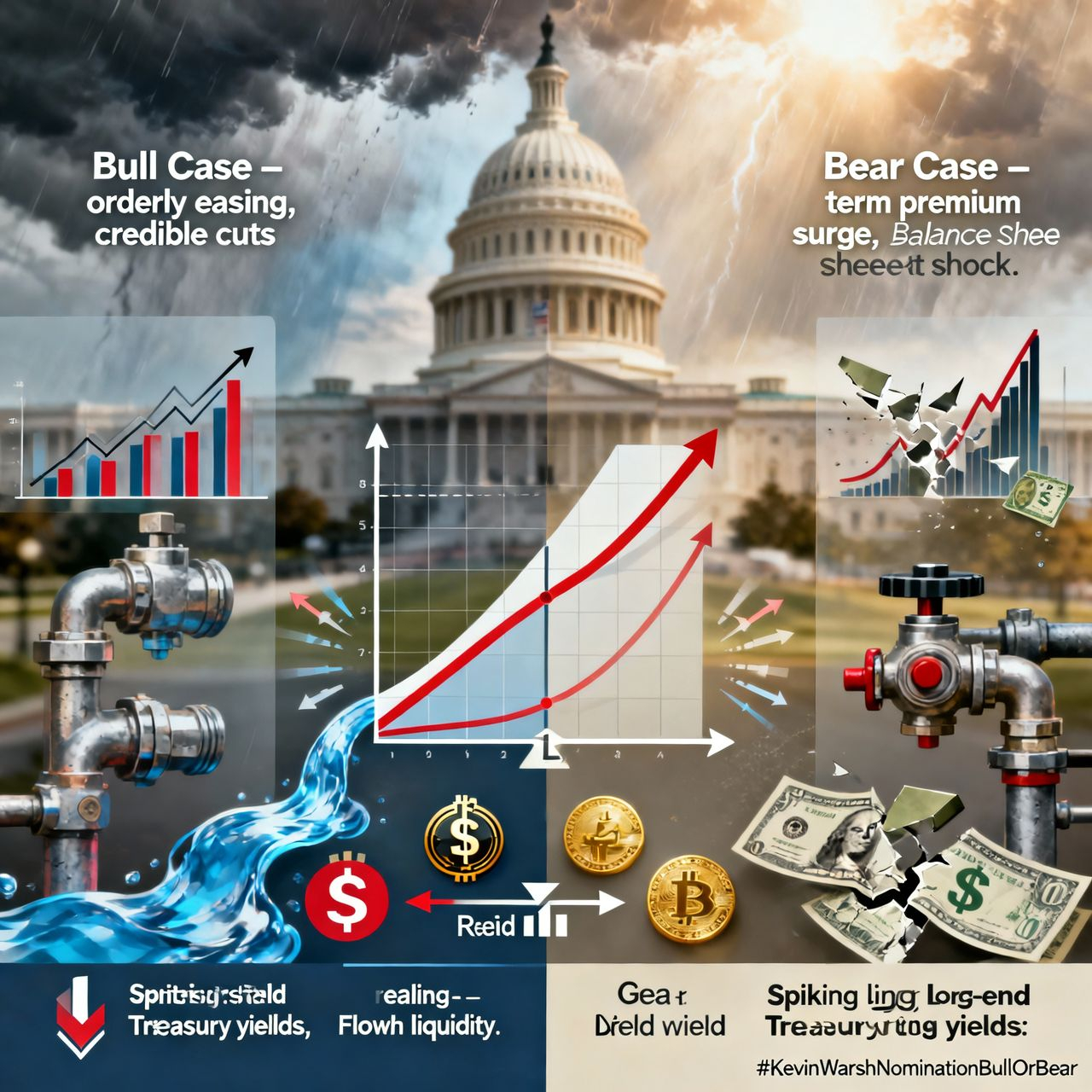

The bullish interpretation

The bullish case assumes three things align.

First Warsh supports earlier or clearer rate cuts once inflation is under control. Second he communicates a disciplined but gradual approach to balance sheet policy rather than a shock driven unwind. Third the confirmation process resolves cleanly reducing institutional uncertainty.

Under this scenario equities benefit from lower discount rates credit conditions ease and risk appetite improves. Crypto also tends to respond positively when real yields fall and liquidity expectations stabilize. The dollar may soften which further supports global risk sentiment.

This is the version of Warsh that markets would eventually embrace as constructive.

The bearish interpretation

The bearish case focuses less on rates and more on structure.

If the nomination fuels doubts about Fed independence investors may demand a higher term premium for holding long dated US debt. That pushes yields higher regardless of short term policy moves. Higher long yields weigh on equity valuations housing affordability and leveraged sectors.

At the same time if balance sheet runoff is emphasized too aggressively liquidity could drain faster than markets expect. This creates funding stress risk especially in periods where growth is already slowing.

In this scenario even rate cuts fail to produce a sustained rally because financial conditions tighten through other channels.

How different assets are likely to respond

US equities sit at the center of this debate. They benefit from lower rates but suffer from higher long term yields. That makes the direction of the curve more important than the headline policy rate.

Treasuries may see front end support while the long end remains volatile. This reinforces curve steepening trades and increases sensitivity to inflation and fiscal headlines.

The US dollar faces opposing forces. Easier policy weakens it while higher yields and risk aversion support it. Expect choppy price action rather than a clean trend

Gold reacts primarily to real yields. If long rates rise faster than inflation gold struggles. If policy easing dominates gold benefits.

Crypto is highly sensitive to liquidity narratives. It performs best when easing is credible and orderly. It performs worst when volatility spikes or when tightening emerges unexpectedly through non rate channels.

The real conclusion bull or bear depends on execution

The Warsh nomination is not inherently bullish or bearish. It is conditional.

It becomes bullish if policy signals are coherent independence is respected and liquidity withdrawal is paced carefully. It becomes bearish if political pressure raises term premiums or if balance sheet tightening offsets rate cuts.

Right now markets are pricing both outcomes at once. That is why volatility has risen and why curve dynamics have become the focal point rather than equity headlines.