@Plasma When I think back on my last trip through Southeast Asia — Thailand especially — it’s not the landmarks or skyline that linger in my mind. It’s a small, almost forgettable moment that ended up saying more about money than any chart ever could.

At the airport, I stood in line for what felt like forever just to exchange cash. By the time I reached the counter, the rate I was offered felt quietly hostile — trimmed by fees, spreads, and the unspoken understanding that travelers don’t negotiate. I accepted it without protest. That’s just how cash works, I told myself. That’s travel.

Later that evening, walking through a crowded night market alive with noise, smoke, and movement, I stopped at a stall selling fresh coconuts. Nothing fancy. Just a man, a knife, and a pile of green shells. I reached for my phone without thinking — cards, wallets, apps, stablecoins — and then paused.

Cash only.

I stood there for a second, almost laughing at the absurdity of it. I could send eight figures across borders on-chain in seconds, yet I couldn’t pay for a coconut sitting right in front of me. Surrounded by technology, liquidity, and access — and still completely stuck.

That was the moment it clicked: cash may still be king, but it’s also one of the heaviest, most inefficient chains we’re still dragging around.

For small and mid-sized businesses across Southeast Asia, this friction isn’t an occasional annoyance. It’s structural. High transaction fees. Slow settlement times. Currency volatility that eats margins overnight. Money leaks out daily — not because businesses are mismanaged, but because the rails themselves are broken.

That same feeling surfaced again when I came across the YuzuMoneyX case shared by @Plasma. Suddenly, the headline figure — $70 million in TVL — stopped feeling abstract. It wasn’t just capital sitting somewhere on-chain. It was money trying to move.

This isn’t about yield farming or speculative positioning. It’s about letting value function in the real world.

What YuzuMoney is building feels like the exact thing I wished existed that night at the market: a clean bridge between digital dollars and everyday commerce. It’s not a DEX. It’s not another DeFi experiment chasing attention. It’s a neobank — designed around how money actually behaves in emerging markets.

By using Plasma’s zero gas fees and near-instant finality, Yuzu offers on-chain USD accounts tailored for Southeast Asian SMEs. Merchants can accept payments that settle directly on Plasma, convert smoothly into USDT, protect themselves from local currency swings, and even earn yield while capital sits idle. When funds are needed off-chain, withdrawals move through traditional banking or card rails — quietly, reliably, without friction.

This is where Plasma’s real advantage starts to show.

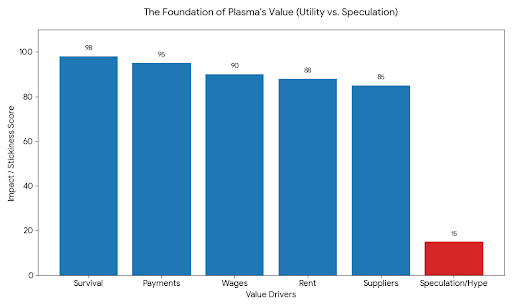

For years, blockchains have been judged by how much value they lock. TVL became the scoreboard. But YuzuMoney points toward a more meaningful measure: how much real economic activity a chain actually settles.

If Plasma becomes the default path for turning cash into digital USD across Southeast Asia, its value won’t come from speculation or hype cycles. It will come from being the invisible layer beneath daily life — payments, wages, suppliers, rent, survival.

That kind of value doesn’t spike. It compounds. It’s quieter, stickier, and far more durable than any lending loop.

And if, sometime soon, someone can scan a QR code and pay a single digital dollar at a street stall in Bangkok or Jakarta, Plasma won’t feel like “another blockchain” anymore. It will be infrastructure — unseen, uncelebrated, and impossible to live without.

@Plasma Maybe then, buying a coconut won’t feel harder than moving $100 million across the world.