Here's a number most people miss.

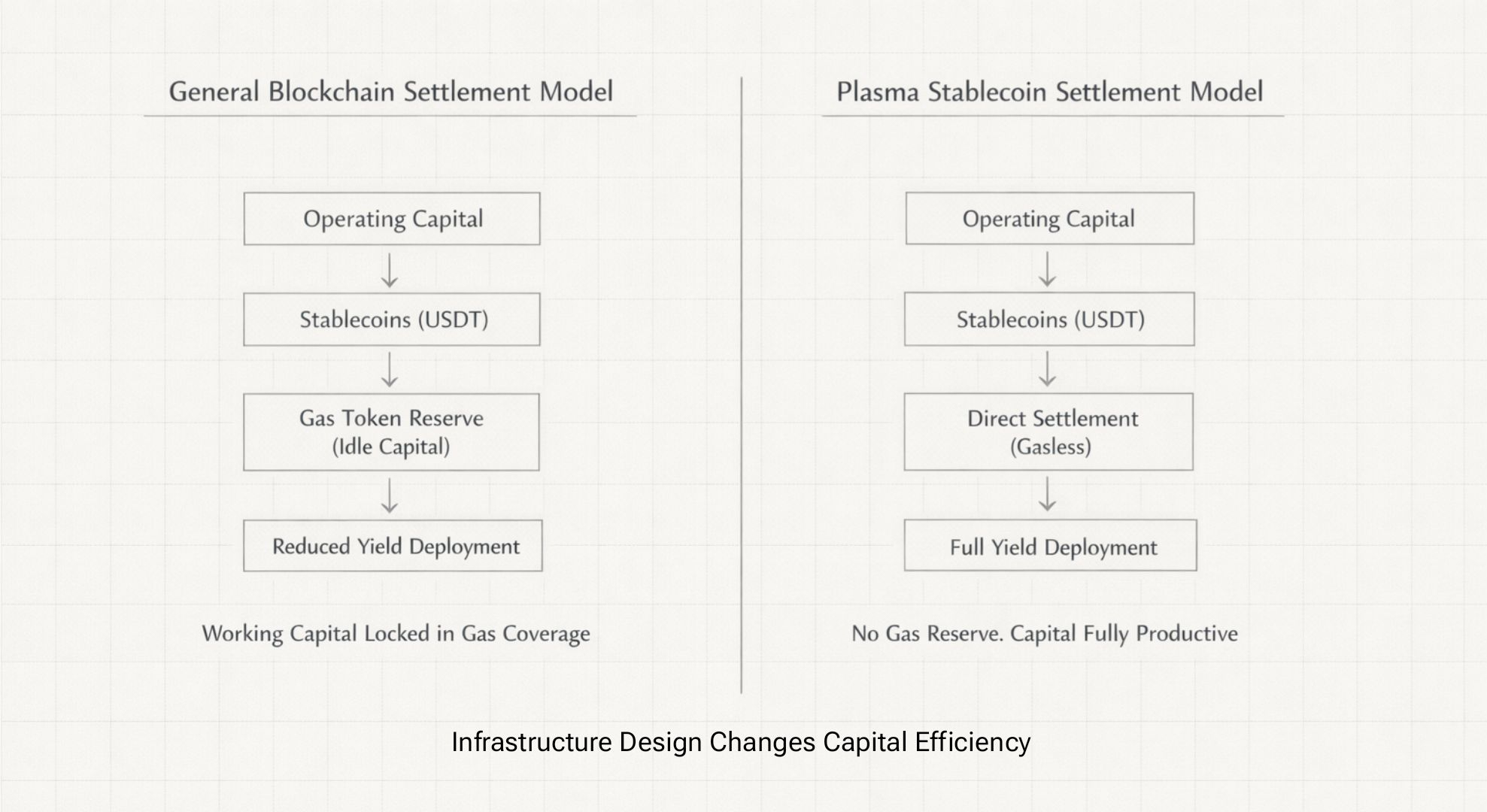

A treasury department managing $50M in monthly stablecoin operations on Ethereum keeps around $1.5M in ETH just sitting there for gas coverage. That's roughly 3% of their operating capital doing absolutely nothing, not earning yield, just exposed to ETH volatility so they can execute USDT transfers when needed.

I’ve actually seen finance teams hold volatile gas tokens purely as operational buffers, and the opportunity cost quietly dwarfs the transaction fees themselves.

If that capital earned 8% instead, you're talking $120K annual opportunity cost. For one treasury department.

Now scale that across the entire $200B+ stablecoin market. You're looking at something like $6 billion in capital locked into gas token reserves that could be earning yield or deployed productively elsewhere.

Plasma's gasless USDT model doesn't just make transfers cheaper. It collapses this entire working capital trap.

That's not a UX win, that's a structural cost advantage that changes how treasuries operate.

That's not a UX win, that's a structural cost advantage that changes how treasuries operate.

Why $1B Moved Into Aave This Fast

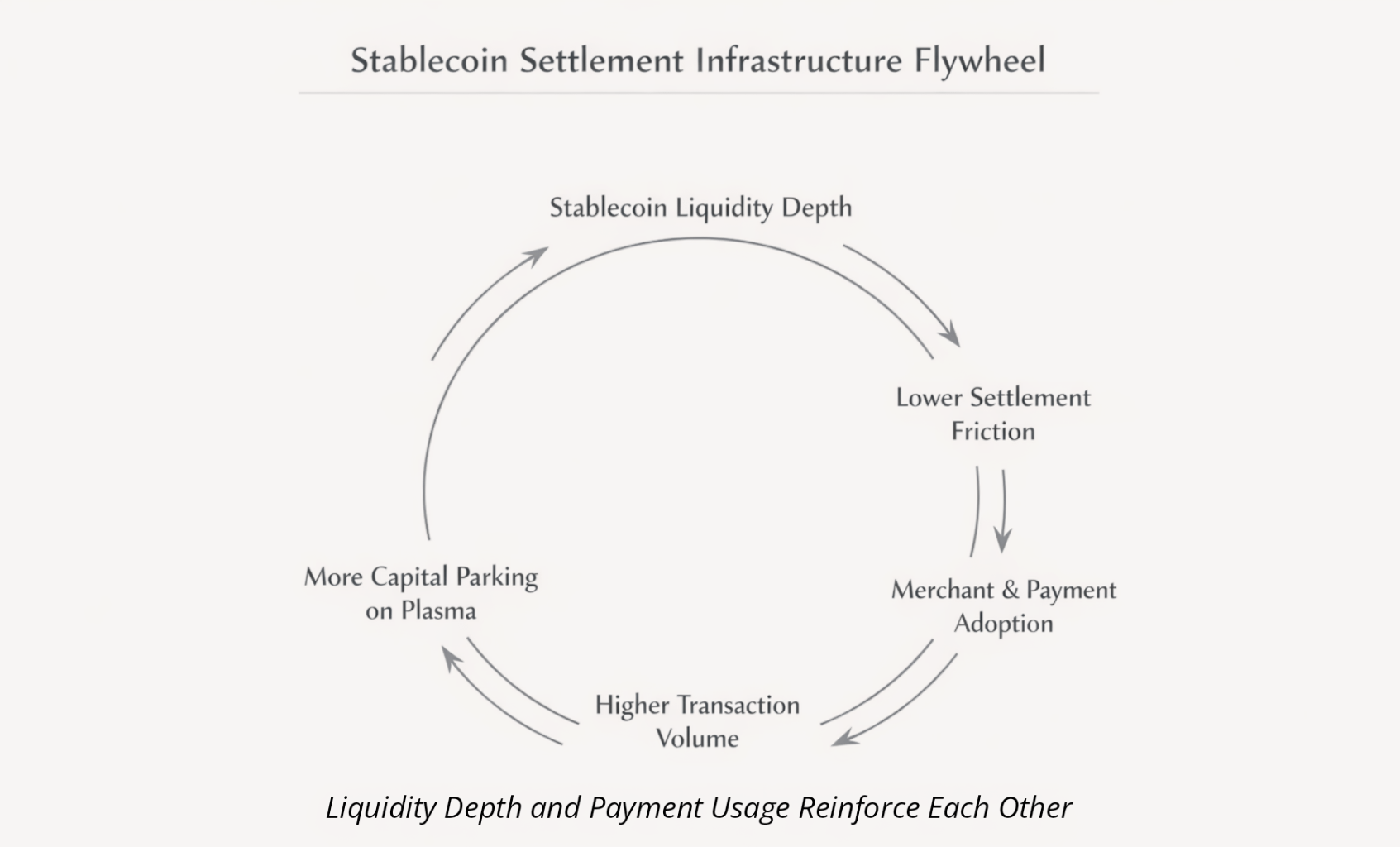

Aave's Plasma deployment hit second largest globally in a matter of months. Over a billion dollars in TVL now.

Institutional money doesn't move that quickly into new infrastructure because yields are 30 basis points better. It moves when the operational economics are categorically different.

Think about the mechanics for a second.

On Ethereum, if you're parking $100M in Aave, you still need maybe $3M in ETH reserves sitting around for potential withdrawals, rebalancing, whatever comes up. That $3M earns nothing while it's covering gas exposure.

On Plasma, zero gas reserves needed. You can deploy the full $100M at 8% yield. That's an extra $240K annually per hundred million in position just from eliminating gas friction.

When moving money in and out doesn't require maintaining a separate volatile asset, capital can rotate between DeFi yield and payment settlement without the operational drag.

That's why the TVL stuck around instead of rotating out like most new chain launches. Not higher returns, lower friction in the cost structure.

ConfirmoPay Is the Quiet Validation

$80M in monthly merchant settlement through ConfirmoPay doesn't sound massive compared to crypto native DEX volumes.

But it represents something way more important, production infrastructure that's been stress tested under actual compliance requirements where failure means real revenue loss.

Payment processors don't evaluate settlement rails the way DeFi traders do. They care about three things.

Cost predictability, can we actually forecast what Q2 expenses will look like, or will gas spikes blow up the budget?

Settlement finality, can we release funds to merchants immediately, or do we need to wait for multiple confirmations and introduce settlement risk?

Operational overhead, how much internal tooling and middleware do we need to build to make this work with existing systems?

Plasma's setup answers all three pretty cleanly.

Gasless USDT means a processor routing a billion dollars annually knows costs won't suddenly spike 400% because some NFT project launched and congested the network.

Sub second finality through PlasmaBFT means merchants get payment confirmation in under a second, basically matching credit card authorization windows instead of the 15 to 60 second waits on other chains. That's not a minor difference when you're standing at a register.

EVM compatibility means their existing accounting integrations don't require custom dev work. Standard Web3 libraries, existing reconciliation systems, no rebuilding middleware from scratch.

This is why ConfirmoPay chose Plasma over chains with way more TVL or bigger marketing budgets. The infrastructure just works better for the actual requirements.

The Margin Capture Math That Changes Everything

Visa processes something like $12 trillion annually at roughly 2% merchant fees. Call it $240 billion in annual revenue.

Now imagine a payment processor routes just 1% of that volume, $120 billion, through Plasma based settlement at 0.3% fees instead of 2%.

They capture about $2 billion in margin that legacy rails structurally can't match.

Here's how the competitive dynamic plays out.

Processor A switches to Plasma infrastructure, starts offering merchants 0.5% fees instead of Visa's 2%.

A merchant doing $5M in annual revenue saves $75K by switching. That's real money.

Processor A still captures around $600K in margin per $5M merchant compared to maybe $100K on legacy rails.

Now Processors B, C, and D are looking at losing market share unless they match.

This isn't some theoretical adoption curve. It's margin compression forcing infrastructure migration, the same dynamic that forced every brokerage to zero fee trading back in 2019 once Robinhood proved the economics worked.

Once one major processor demonstrates this works at scale, competition makes it inevitable for others.

Bitcoin Anchoring Solves a Question Nobody Asks Out Loud

When institutions are evaluating settlement infrastructure, they don't really ask "is this decentralized enough?"

The real question is, what happens when regulatory pressure targets your governance?

Every blockchain with a foundation in a specific jurisdiction, validator sets concentrated in certain regions, or core dev teams subject to particular legal frameworks, they all have to answer this somewhat awkwardly.

Plasma's security anchoring to Bitcoin gives a completely different answer.

Bitcoin has been running for 15 years across every kind of adversarial regulatory environment you can imagine. Multiple governments trying to control it, banking system pressure, jurisdictional conflicts, and it has stayed accessible, operational, neutral throughout.

That's not theoretical neutrality. That's empirical evidence of resistance to capture.

For a CFO deciding whether to route treasury operations through stablecoin infrastructure, Bitcoin anchoring answers a specific compliance concern, if geopolitical tensions escalate between jurisdictions we operate in, will our settlement rail still work?

With legacy correspondent banking, no, depends entirely on diplomatic relationships staying stable.

Foundation governed blockchain, maybe, depends where validators and governance happen to be concentrated.

Bitcoin anchored settlement layer, it inherits that 15 year track record of staying operational through regulatory conflicts.

This is what unblocks institutional pilots. Not because CFOs suddenly care about decentralization philosophy, but because they need infrastructure that won't become collateral damage in jurisdictional disputes they have no control over.

StableFlow Actually Matters for Large Treasury Operations

StableFlow integration enabling million dollar swaps with zero slippage isn't really built for retail traders.

It's viability proof for institutional treasury operations that move serious size.

Look at what happens when a corporate treasury needs to rebalance $50M between USDT and USDC on Ethereum.

Slippage on orders that large runs maybe 0.1 to 0.3%, so you're losing $50K to $150K right there.

MEV extraction from front running adds another 0.05 to 0.15%.

Gas costs during high volatility rebalancing windows.

You're looking at combined friction around $75K to $200K per large rebalancing operation.

Same operation on Plasma with StableFlow.

Zero slippage up to a million per swap. CoW Swap integration removes MEV extraction. Gasless execution for stablecoin operations.

That $50M rebalancing happens at near zero friction cost.

When institutions start realizing they're paying $150K in slippage and MEV for something Plasma executes basically for free, the infrastructure choice becomes pretty obvious.

The Market's Completely Mispricing This

$200M market cap for infrastructure that's holding over a billion in institutional deposits, processing $80M monthly in actual production merchant volume, running the second largest Aave deployment globally.

The market is pricing this like a speculative Layer 1 trying to compete for ecosystem size.

It should be pricing it like clearing infrastructure approaching critical adoption.

Visa market cap, $580B on $12T annual payment volume

Stripe private valuation, $65B on over $1T annual processing

Plasma right now, $200M on infrastructure that could technically handle equivalent volumes today

The gap exists because the market hasn't figured out yet that Plasma isn't really competing with Solana or Arbitrum for DeFi ecosystem dominance.

It's competing with Visa and SWIFT for settlement market share, on cost structure, finality speed, and capital efficiency.

Once payment processors start demonstrating actual margin capture, the valuation framework shifts completely. Not "blockchain project", but clearing house actively displacing legacy rails.

And that repricing will not be gradual. It will be structural.

What That $1.1 Billion Is Really Betting On

The capital sitting in Syrup and Aave, over a billion at this point, isn't speculative yield farming.

It's institutional money positioned for the working capital arbitrage play.

That capital already knows.

Plasma's architecture eliminates the gas token drag and unlocks that 3% working capital.

Sub second finality matches payment UX requirements merchants expect.

Bitcoin anchoring provides the regulatory neutrality hedge for compliance approval.

Production infrastructure is already validated with real merchant flow.

They're not waiting for Plasma to build better tech. They're waiting for the broader market to realize legacy payment rails are structurally obsolete.

When a CFO somewhere calculates they're burning $120K annually on ETH gas reserves that Plasma completely eliminates.

When a payment processor captures billions in margin by undercutting legacy fee structures.

When accounting platforms finally add the stablecoin settlement field to their software.

The efficiency gap becomes impossible to ignore anymore.

And the capital that positioned early at $200M valuation will not be selling at $200M.

The Bet

Plasma is not a blockchain racing for developer ecosystem growth. It is clearing infrastructure eliminating billions in working capital drag while letting payment processors capture margin legacy rails cannot touch.

The market is still pricing the first narrative. Smart money is positioning for the second.

That gap closes in 2026.