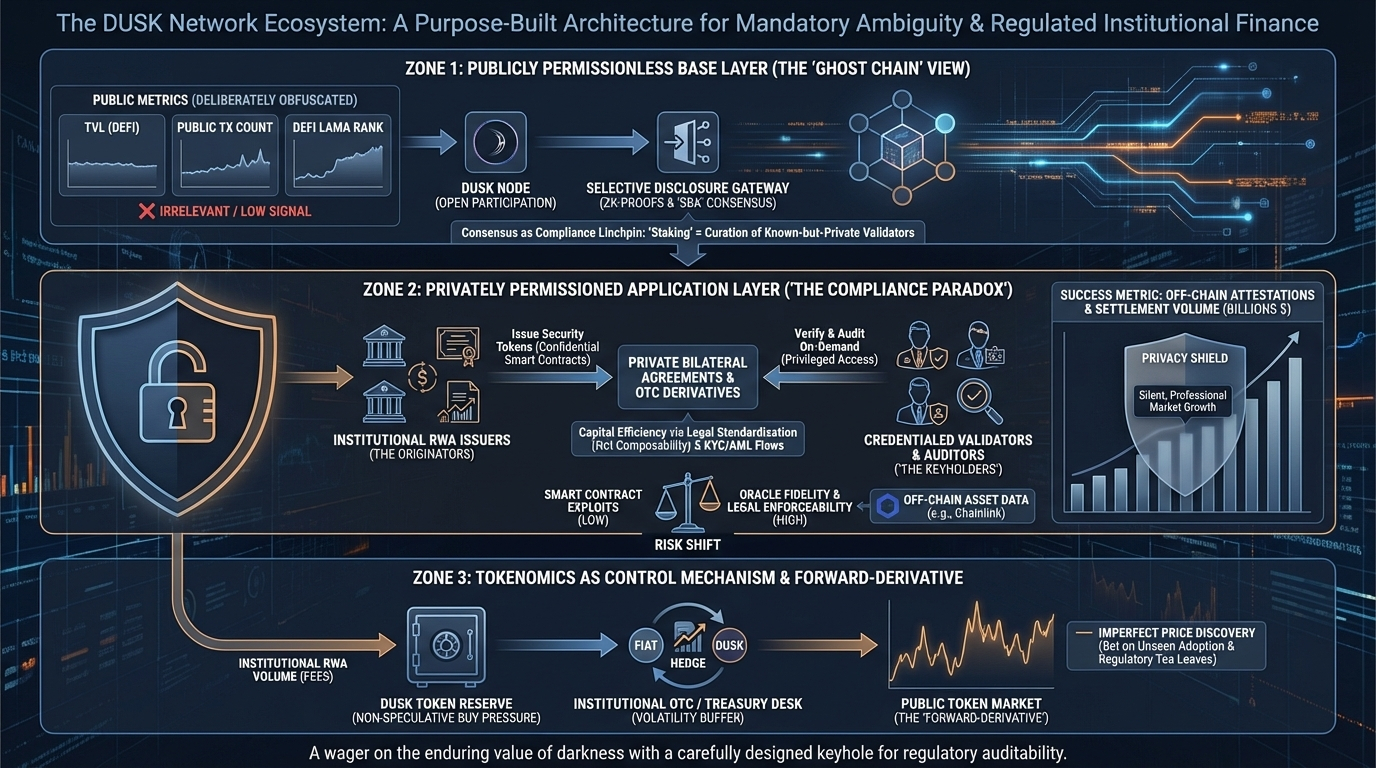

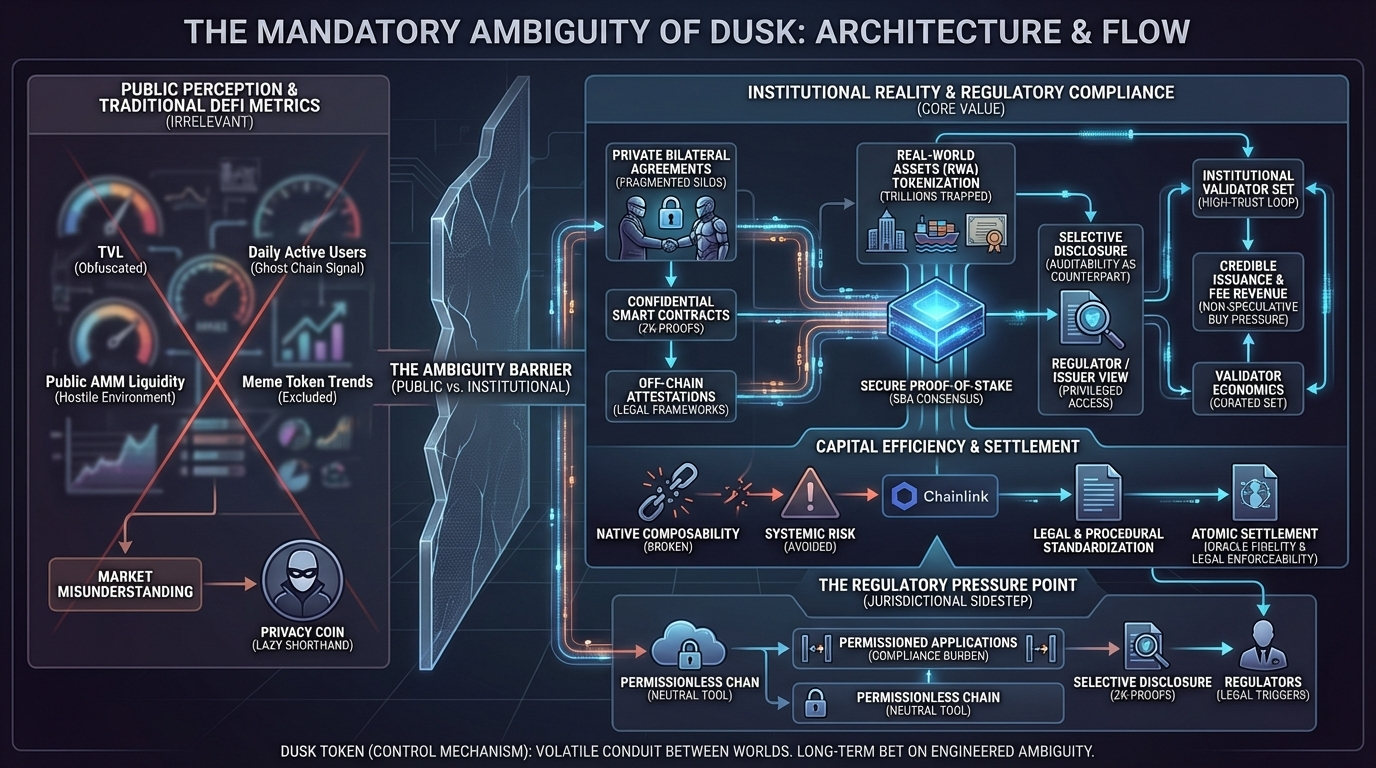

@Dusk is not a privacy coin in the conventional sense, and that is its only path to survival. The market, with its lazy shorthand, labels it as such a token for hiding transactions. This classification is a critical error in judgment, a misunderstanding that reveals a deeper market blindness to the only regulatory reality that matters: auditability is not the enemy of privacy; it is its necessary counterpart in any system that intends to interact with institutional capital. To analyze DUSK is to dissect a deliberately constructed paradox, a blockchain engineered for the specific, unglamorous tension between hiding value flows from the public and revealing them, on-demand, to a privileged, credentialed few. This is not monero for banks; this is a meticulous architectural play for the trillions trapped in pre-tokenized real world assets, and its success hinges on a validator economics model and a capital flow logic that is fundamentally alien to the DeFi-native crowd currently dominating sentiment.

Let's begin by dismanting the primary narrative. The instinct of a trader is to look for liquidity magnets the applications that pull in TVL, the speculative loops that bootstrap a token economy. DUSK’s architecture is purposefully hostile to this model. Its confidential smart contracts, built around zero-knowledge proofs and a notion of selective disclosure, are not designed for public leverage farming or transparent Ponzi schemes. They are designed for private bilateral agreements, for over the counter derivatives, for the issuance of a digital bond where the ownership ledger is opaque but instantly verifiable by the issuer and a regulator. The liquidity here does not pool in a public AMM; it exists in fragmented, permissioned silos. This means the on-chain metrics we typically fetishize TVL, daily active addresses in the naive sense, transaction count are not just irrelevant; they are deliberately obfuscated. A thriving DUSK ecosystem could look like a ghost chain to Dune Analytics, while facilitating billions in security token settlements. The first lesson is to unlearn our public chain metrics. Success for DUSK is measured in off-chain attestations, in the signing of legal framework agreements with stock transfer agents, not in trending on DeFiLlama.

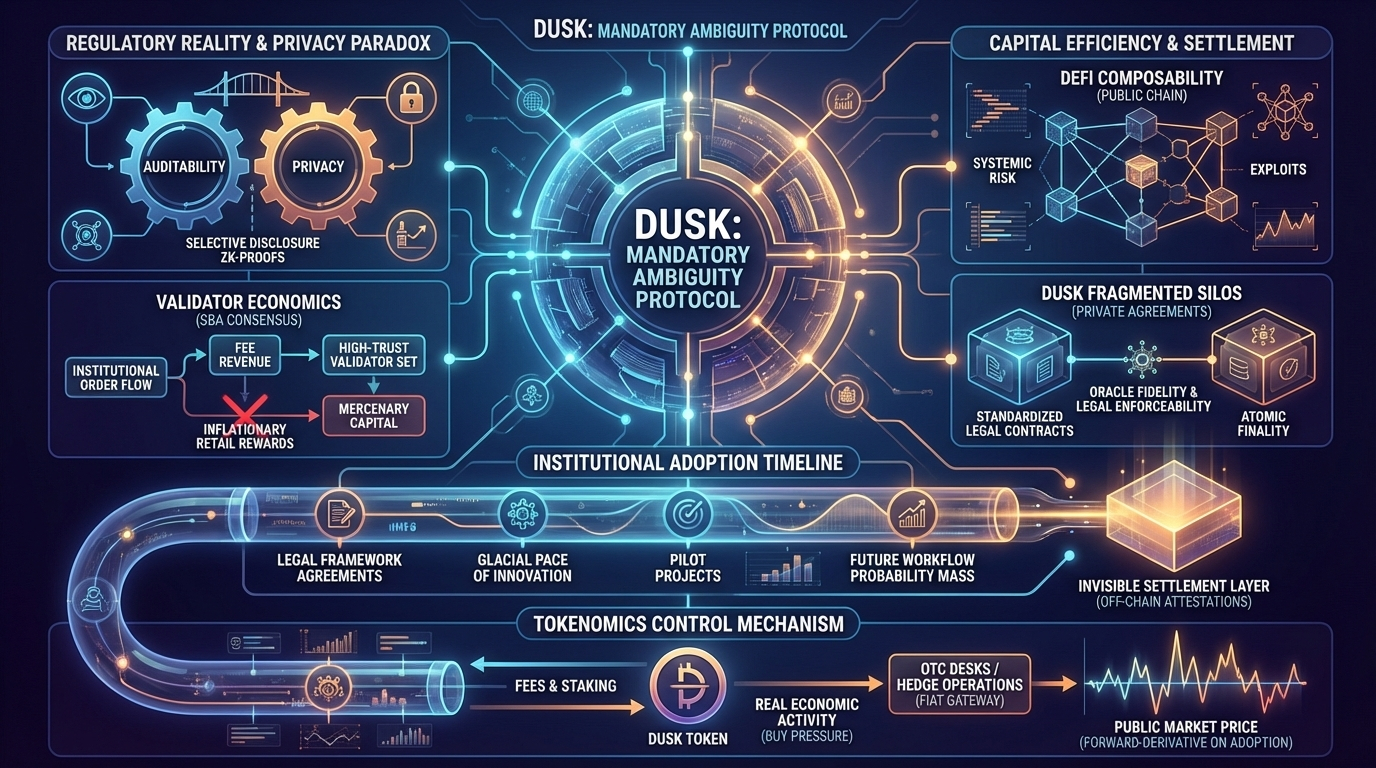

This leads to the core infrastructural gambit: DUSK’s Secure Proof-of-Stake consensus, or what they term the "SBA" (Succinct Blockchains Agreement) consensus. The market overlooks consensus as "solved," but here it is the linchpin of the compliance/priavcy trade-off. The "staking" in this system isn't just about securing the chain against Sybil attacks; it's about curating a permissioned set of known-but-private validators. The economic incentive is not merely inflationary token rewards; it is the fee revenue from settling private, high-value financial instruments. The validator set, therefore, is incentivized to attract not retail delegators, but institutional order flow. Their profit is a function of the real-world asset volume they can onboard, not the token price they can pump. This creates a cold-start problem of monumental proportions, but also a powerful flywheel if solved: credible validators attract credible issuance, which increases settlement fees, which attracts more credible validators, raising the security and prestige of the chain. It's a closed, high-trust loop that explicitly excludes the anonymous, mercenary capital that secures Ethereum or Solana.

Now, consider capital efficiency and settlement risk in this context. In a transparent DeFi system, efficiency is derived from composability the ability of one smart contract to trustlessly interact with another's state. This composability creates systemic risk, as we've seen in every cascade. DUSK’s privacy breaks native composability. A confidential security token cannot be seamlessly used as collateral in a public lending market without revealing its state, which defeats the purpose. Therefore, capital efficiency on DUSK is not achieved through on-chain lego bricks, but through legal and procedural standardization. Efficiency comes from having a standardized, legally vetted digital security contract template, from KYC/AML flows that work across multiple issuers, from a predictable regulatory interpretation. The settlement is atomic and final, but the "risk" shifts from smart contract exploits to oracle fidelity and legal enforceability of the off-chain rights the token represents. This is why their partnership with Chainlink for oracles wasn't a buzzword play; it was a foundational necessity to bring off chain asset data into the confidential envelope. The trade off is stark: you exchange the 24/7, wild west composability risk for the slower, but potentially far more vast, world of traditional finance's operational risk.

The regulatory pressure point is where DUSK’s thesis is most provocative. Most "compliant" chains take a binary approach: either full KYC for all participants (permissioned chains) or anarchy. DUSK attempts a third path: a publicly permissionless chain with privately permissioned applications. The base layer is open for anyone to run a node or send a private transaction. However, the applications built on top the security token issuance platforms can and must enforce their own gated access. The blockchain provides the tool (selective disclosure via zero knowledge proofs) for the application to prove compliance without exposing underlying data. This is a clever jurisdictional sidestep. The chain itself can argue it is a neutral tool, like TLS encryption for the internet. The compliance burden is pushed to the application layer, to the licensed entities who are already used to bearing it. This architecture is the only viable long-term design for surviving the coming regulatory clampdown on anonymizing systems. It doesn't fight regulation; it bakes in the levers for regulators to pull, but only in specific, legally triggered circumstances.

Institutional adoption, therefore, isn't constrained by DUSK’s technology, which is arguably fit for purpose. It is constrained by the glacial pace of financial legal innovation and the prisoner's dilemma of being first. A major bank can't tokenize a fund on DUSK until their lawyers, their regulator, and their execution counterparties all agree on the digital representation. This is a sales and education cycle measured in quarters and years, not crypto natives' weeks. The capital flowing into DUSK tokens today is not pricing in next quarter's "product launch"; it's making a multi year bet on the convergence of a specific regulatory attitude and this specific technical stack. This is why the token often exhibits periods of profound stillness followed by violent re-ratings on news that seems minor to the public a pilot with a European small-cap exchange, a whitepaper update detailing a new zk-proof circuit. The market is trying to price the unpriceable: the probability mass of future institutional workflow.

Finally, look at the tokenomics not as a reward schedule, but as a control mechanism for this long, fraught journey. The DUSK token is required for fees and staking. If the primary fee payers are intended to be institutions issuing assets, they must acquire DUSK, likely from the open market. This creates a direct, non speculative buy pressure tied directly to real economic activity on the chain. However, this also makes the token volatile and potentially expensive for their target users a problem. The likely, unspoken endgame is for major issuers or validators to run OTC desks or treasury operations to hedge their DUSK exposure, effectively creating a stable, institutional facing fiat to DUSK gateway that insulates them from crypto volatility. The public market token, then, becomes a forward derivative on the adoption of that private, institutional settlement layer. Its price discovery is forever imperfect, based on our noisy guesses about a silent, professional market forming in the shadows.

What we are left with is a project whose success looks nothing like the crypto we know. A successful DUSK means a bustling, private institutional settlement layer that is largely invisible to us, with its native token acting as a volatile, hard to value conduit between our world and that one. It is a bet on ambiguity as a product, on regulated privacy as an oxymoron that can be engineered into existence. Trading it requires not chart patterns, but a deep reading of financial regulatory tea leaves, of the hiring patterns of traditional finance digital asset teams, and the courage to sit through epochs of irrelevance while the real-world, non-crypto narrative infrastructure is painstakingly laid, brick by legal brick, in the dark. In a market obsessed with transparency and public spectacle, DUSK is a wager on the enduring value of darkness with a carefully designed keyhole.