@Plasma Crypto has spent so many years acting like a casino that it’s easy to forget there’s a real plumbing problem underneath the noise. Most people don’t wake up hoping to “ape” into anything; they just want to move money without it getting lost, delayed, or shaved down by fees. Stablecoins have forced that truth into the open. A token that tries to behave like a dollar only matters if it can travel like a dollar. Plasma is interesting because it doesn’t pretend to be the whole future of finance. It’s narrowly focused on one job: making stablecoin transfers feel like payments, not like a scavenger hunt through wallets and bridges.

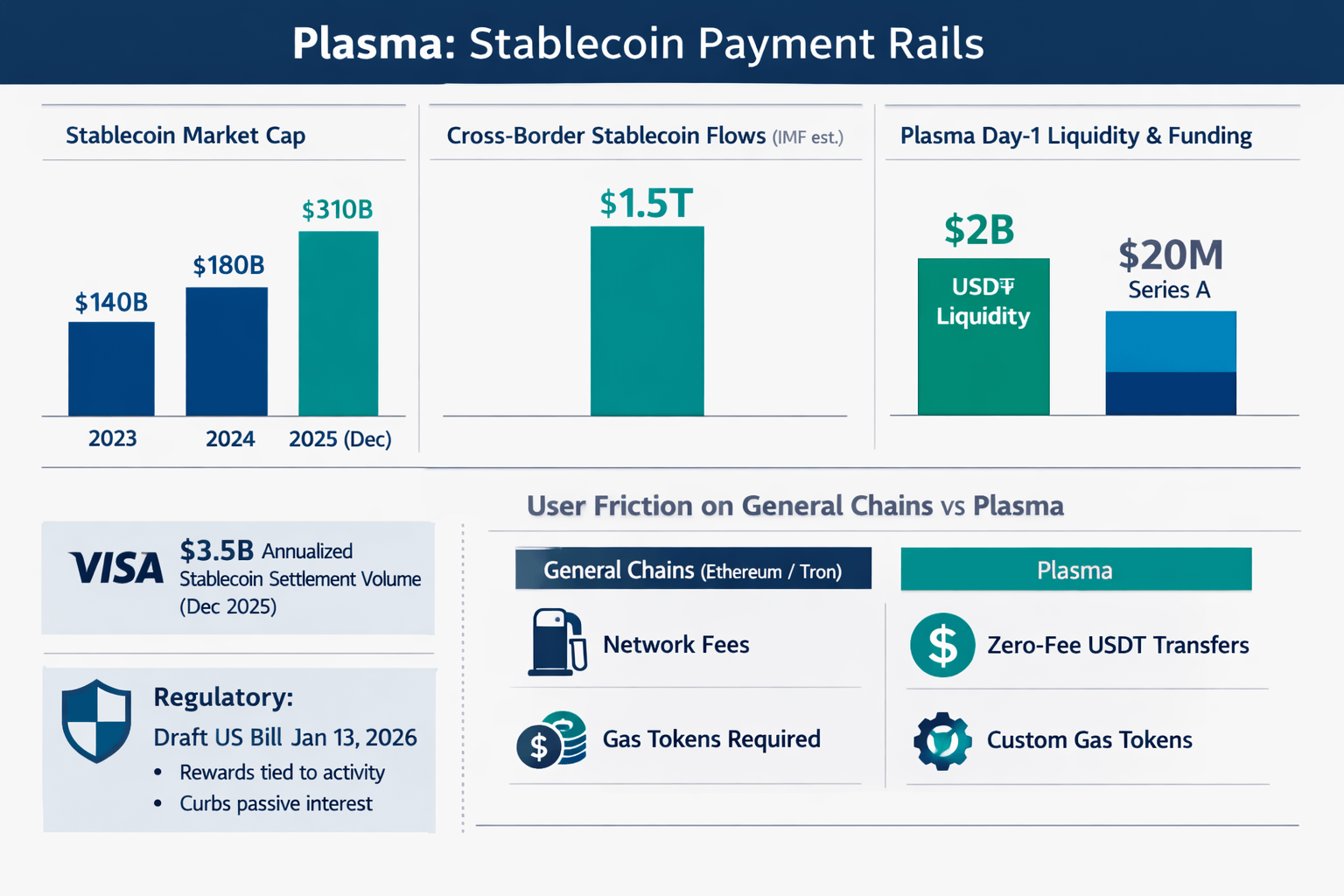

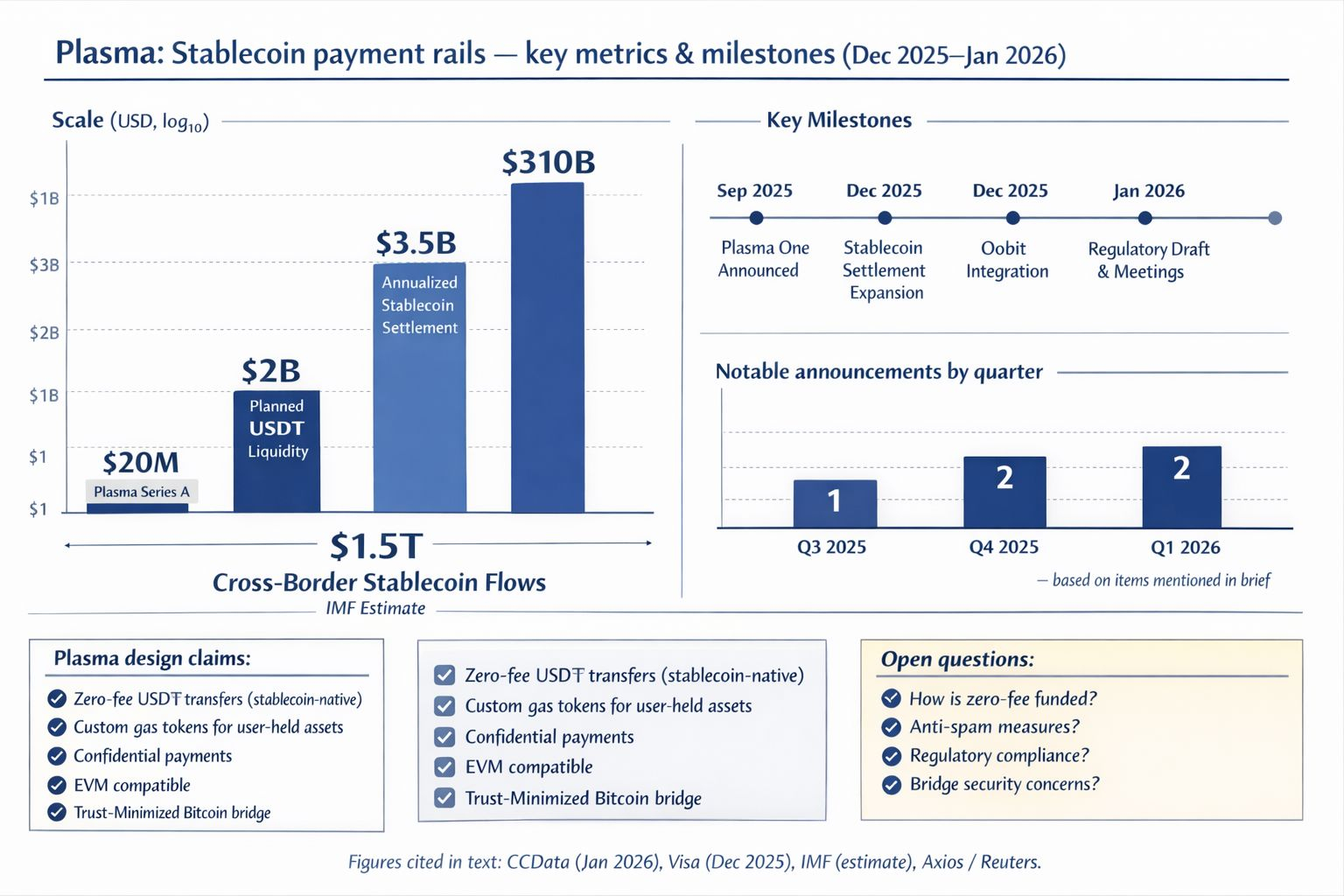

The lane is getting busy. CCData’s stablecoin report in January 2026 said the total stablecoin market reached about $310 billion in December 2025. Visa has been expanding stablecoin settlement, and in a December 2025 announcement it cited more than $3.5 billion in annualized stablecoin settlement volume as it brought USDC settlement to U.S. institutions. The regulatory push is getting louder too. Reuters reported a January 13, 2026 draft U.S. bill that would curb interest just for holding stablecoins while allowing rewards tied to activity. Days later, Reuters described a White House meeting that failed to resolve a stalemate between banks and crypto firms over stablecoin rewards.

That tension shows up in everyday user friction. A payment rail should be boring: clear costs, predictable timing, and minimal chance of surprise. But most stablecoins sit on general-purpose networks where payment traffic competes with everything else. An Axios report on Plasma noted Ethereum and Tron as the main platforms for stablecoins today, while highlighting that both have drawbacks. Anyone who has tried to send a “digital dollar” and then discovered they also needed a separate token to pay network fees understands the problem immediately.

Plasma’s approach is to put stablecoins at the center of the design. Plasma describes itself as a high-performance Layer 1 built for USD₮ payments. Its documentation says it provides stablecoin-native contracts for zero-fee USD₮ transfers, custom gas tokens so apps can keep users paying fees in assets they already hold, and confidential payments, while remaining EVM compatible. It also describes a native, trust-minimized Bitcoin bridge for moving BTC into its EVM environment. And it says it plans to launch with roughly $2 billion in USD₮ liquidity available from day one.

In crypto, talk is cheap, so I always look for the receipts. Plasma’s been trying to provide them, and fundraising is one of the clearer markers. According to Axios, it brought in $20 million in a Series A led by Framework Ventures. In September 2025, industry coverage described Plasma One as a stablecoin-native neobank and card built around USDT users who want smoother cash-out and everyday spending. In December 2025, Oobit announced an integration with Plasma to let users spend USD₮ held on Plasma at more than 100 million Visa merchants worldwide.

But the “rails” metaphor also raises the bar. Central bankers have been blunt that stablecoins don’t automatically qualify as good money, warning about integrity, resilience under stress, and misuse. At the same time, the BIS has acknowledged why people reach for stablecoins in high-inflation or restricted environments, especially for cross-border payments and trade settlement. The IMF estimates stablecoin cross-border payment flows at about $1.5 trillion, while stressing they’re still a small fraction of global cross-border flows.

Zero-fee is a great phrase, but it’s also the kind of phrase that makes cautious people lean back in their chair. Not because it’s impossible—just because it begs for specifics. Are costs covered through spreads? Are apps subsidizing the network? Are transfers being batched to keep expenses down? Whatever the answer is, Plasma will have to be upfront about it, and it’ll need serious anti-spam protection if it wants to handle everyday payments. Free works when it’s boring and reliable; when it isn’t, it breaks at the worst possible moment.

So the question I keep coming back to is simple: can Plasma be boring on purpose? That means surviving spam, keeping costs predictable even when markets get wild, and proving the “trust-minimized” pieces are more than a diagram. It also means fitting into regulation without turning into a walled garden. If Plasma succeeds, it won’t be because it replaces banks or card networks. It’ll be because it makes stablecoin dollars easier to move and easier to trust, and then it keeps doing that long after the hype cycle moves on.