@MidnightNetwork I remember pausing when I first looked at Midnight’s token distribution chart, expecting to find the usual pattern—large early allocations to venture capital, vesting cliffs, and the familiar gravity those positions create in secondary markets. What stood out instead was how difficult it was to locate that center of pressure. It felt less like a cap table and more like a budget.

The common assumption is that every network quietly revolves around insider allocation. That early capital shapes liquidity, governance, and ultimately narrative. Midnight seems to resist that framing, or at least re-route it. The question is not whether insiders exist, but where their influence is embedded.

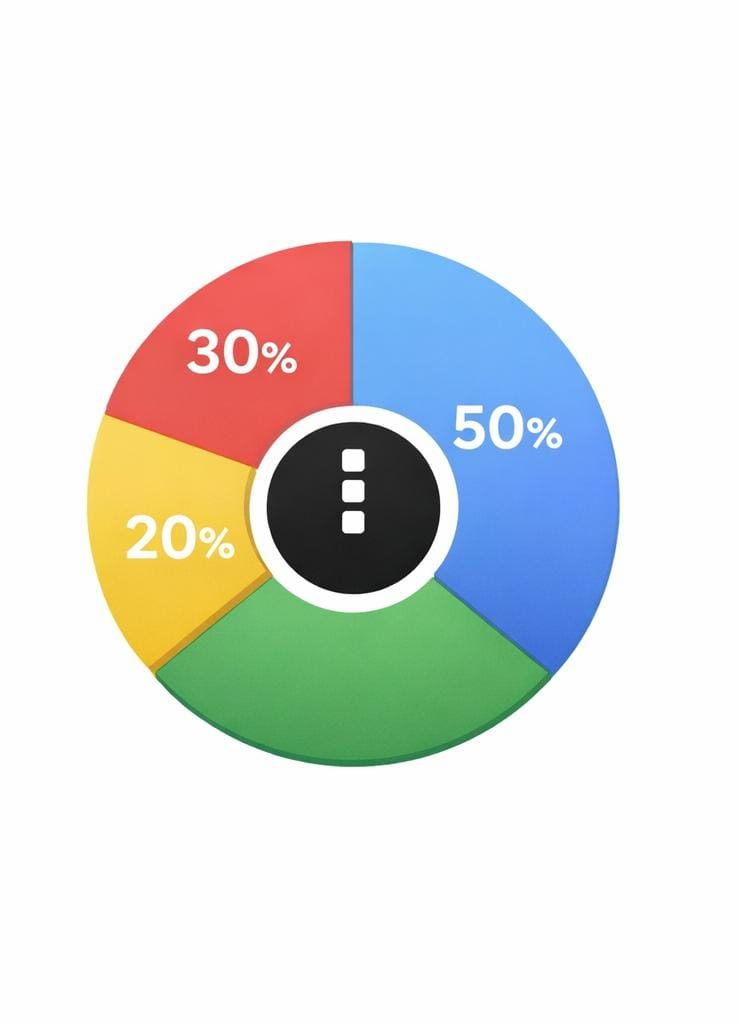

On the surface, the distribution looks unusually weighted toward system functions. Roughly 30% of supply flows into a treasury and close to 20% into block rewards. To most observers, that reads as infrastructure funding. Underneath, it is something closer to deferred distribution—tokens that enter circulation through usage rather than upfront ownership.

That distinction matters. If nearly 50% of supply is released gradually through validator incentives and treasury spending, then the network replaces immediate insider liquidity with time-based emission. It shifts the axis from “who owns” to “who participates.” But participation here is not neutral. It is structured.

Block rewards, for instance, are not just payments. At around 20% of total allocation, they define the pace at which new supply reaches the market. In a crypto environment where daily exchange volumes still fluctuate between $70B and $100B, that pacing determines whether a token quietly integrates into liquidity or destabilizes it. Slow emission can smooth price discovery. It can also delay real demand signals.

The treasury introduces a different layer. A 30% allocation is not small—it is effectively a long-term capital reserve embedded in protocol logic. Surface level, it funds development and ecosystem growth. Underneath, it acts as a counterweight to external capital. Instead of relying on venture firms to finance expansion, the network internalizes that function.

What this enables is a kind of controlled autonomy. Development does not immediately depend on external investors seeking returns within fixed time horizons. In theory, that reduces the pressure for early liquidity events or aggressive listings. But it also centralizes discretion. A treasury is still governed, even if on-chain.

This is where the absence of obvious venture allocation becomes more ambiguous. Midnight does not eliminate insider influence; it redistributes it across mechanisms. Treasury governance, validator participation, and emission schedules become the new sites of control. Influence becomes procedural rather than positional.

From a coordination perspective, this changes behavior. Validators are not just securing the network; they are primary recipients of circulating supply. If rewards are steady, they become long-term holders by default. That can stabilize the system, but it also concentrates exposure among a smaller set of actors.

There is also a quieter implication tied to Midnight’s dual-token structure. Users interact with DUST for execution while holding $NIGHT as the underlying asset. Observers see “free transactions.” Underneath, the treasury and block rewards subsidize that experience. In effect, token distribution is not just about ownership—it is about financing user behavior.

That financing model introduces subtle pressure. If the network absorbs transaction costs through its own reserves, then sustainability depends on how efficiently those reserves are deployed. A large treasury can mask inefficiencies for years. It can also delay the moment when real demand must justify ongoing issuance.

In current market conditions, where institutional capital is increasingly flowing through regulated vehicles like spot ETFs and avoiding direct exposure to smaller tokens, this design has mixed consequences. On one hand, reduced reliance on venture capital aligns with a broader skepticism toward insider-heavy distributions. On the other, it may limit early liquidity pathways that exchanges and market makers typically rely on.

Liquidity is not just a technical outcome; it is negotiated. Without concentrated early holders, it becomes harder to seed deep order books quickly. That can slow adoption, especially when traders expect tight spreads and immediate execution. A system designed for long-term alignment may struggle in short-term markets.

There is also regulatory ambiguity. By minimizing explicit insider allocations, Midnight positions itself differently from projects that resemble equity-like distributions. But a large on-chain treasury can still attract scrutiny. Control over funds, even if decentralized in theory, often becomes a focal point for regulators.

What emerges is a distribution model that shifts the location of power rather than removing it. Venture capital does not disappear; it is replaced by protocol-controlled capital. Insider advantage does not vanish; it becomes embedded in governance processes and emission timing.

The deeper pattern here reflects a broader trend in crypto infrastructure. Systems are moving away from visible concentration toward structural concentration. Instead of large wallets, influence is encoded in mechanisms—treasuries, reward schedules, and access to participation layers.

That shift feels quieter, but not necessarily simpler. It requires users to trust not just who holds tokens, but how tokens move. And movement, in this case, is governed by design choices that unfold over years, not quarters.

What Midnight seems to represent is an attempt to turn token distribution into a coordination system rather than a capital event. Whether that holds under real market pressure remains uncertain.

Because in the end, distribution is not about where tokens start. It is about who controls their path through time.#night