I've been staring at this token for three weeks and I'm genuinely still not settled on it, which is actually why I decided to write about it. The projects I feel completely certain about rarely produce interesting analysis. The ones that keep pulling me back even when I'm trying to move on, those are usually the ones worth thinking through carefully.

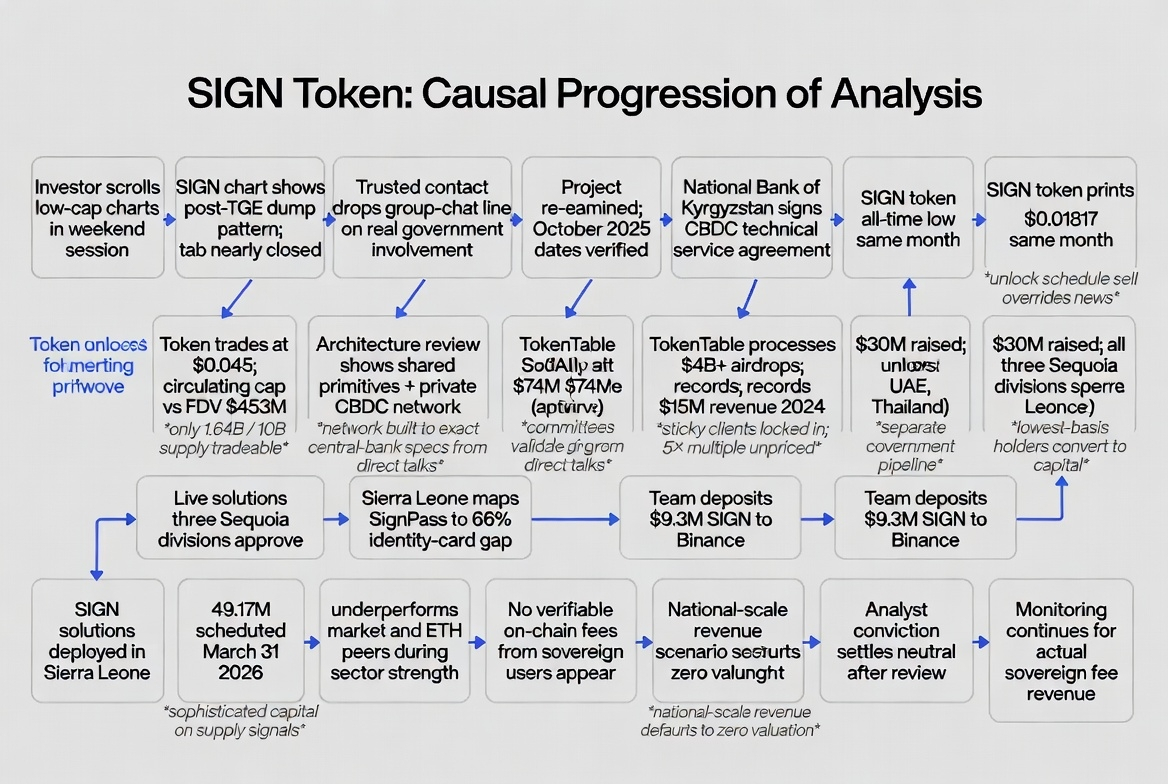

SIGN first crossed my radar during one of those late weekend rabbit hole sessions where you're just scrolling through low caps trying to find something that feels different from the usual noise. I spent about four minutes on the chart, saw the classic post-TGE dump pattern, saw the float structure, and almost closed the tab immediately. Nothing about the surface level picture looked particularly interesting.

But then someone I actually trust dropped a single line in a group chat. Something along the lines of "the government stuff here is actually real, not the usual crypto fake partnership." That kind of comment from that kind of person makes me go back and look harder. So I did. And here we are.

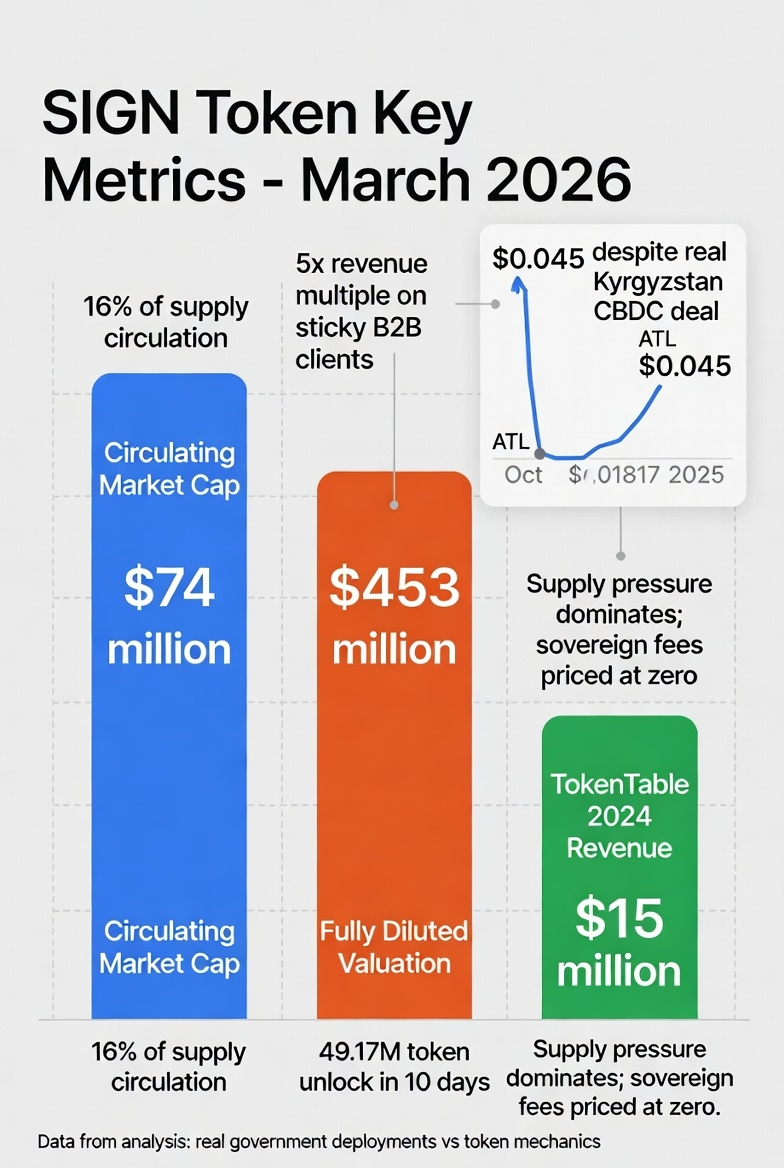

The first thing that genuinely confused me was the chart behavior around October 2025. SIGN hit its all-time low of $0.01817 on October 10, 2025. I want you to sit with that date because that same month the team signed a technical service agreement with the National Bank of Kyrgyzstan for their central bank digital currency project. A real government. A real signed legal agreement. A real CBDC pilot entering active testing. And the token responded by printing its lowest price in its entire existence.

I genuinely thought I had the dates wrong when I first noticed this. I checked multiple times. The dates are right. What I eventually understood is that the unlock schedule was so aggressive at that point that no positive news could compete with the raw sell pressure coming from early holders distributing into whatever liquidity was available. The government deal was real. The selling was also real. Both things were simultaneously true and driven by completely separate forces that had nothing to do with each other. That dynamic is still the central tension in this token and I do not think most people writing about SIGN have fully sat with it.

Today SIGN sits at around $0.045, with a circulating market cap of roughly $74 million against a fully diluted valuation of $453 million. Only 1.64 billion of the 10 billion maximum supply tokens are currently tradeable. Which means you are buying approximately 16% of the eventual float and paying $74 million for it while the remaining 84% enters the market on a schedule you have zero control over. I want to be genuinely clear that this is a serious structural problem and not something you can narrative your way out of. The supply is coming regardless of how compelling the product story sounds. Anyone who tells you otherwise is either not doing the math or not being straight with you.

What kept me from closing the tab permanently despite that math is what I found when I actually read what the product architecture does rather than relying on the generic "blockchain credential verification" framing that appears in almost every write-up about this project. S.I.G.N. describes the sovereign system architecture, and Sign Protocol is the evidence layer used across sovereign and institutional workloads, while TokenTable and EthSign are standalone products that use the same core primitives and can be integrated into S.I.G.N. deployments when appropriate. In plain language what that means is that every product in the SIGN ecosystem, the token distribution tool, the identity layer, the document signing product, all run on the same cryptographic foundation and were specifically designed to be dropped into a national government's existing infrastructure without requiring the government to rebuild everything from scratch. The Sign Stack has a dual blockchain architecture consisting of customizable Layer-2s built on public Layer-1 networks and a private network specifically for CBDC operations.

That private CBDC network is the detail that made me sit up. You do not build a private network specifically architected for central bank digital currency operations because you think it would be a cool whitepaper feature. You build it because central bank officials sat across a table from your team and told you precisely what their regulatory requirements, operational constraints, and IT infrastructure limitations were, and your team went home and built exactly that. That level of product specificity does not come from speculation about what institutions might eventually want. It comes from real conversations with institutions who were seriously evaluating whether to actually buy your stack.

Underneath all of this sovereign infrastructure ambition there is also a real commercial business generating real money right now that I think is almost completely ignored in the market's current pricing. TokenTable generated $15 million in revenue in 2024, processing over $4 billion in token airdrops including over $2 billion distributed to 40 million users in the TON ecosystem alone, with verified clients including Starknet, ZetaChain, DOGS, Mocaverse, Notcoin, and GAMEE. Fifteen million dollars in annual revenue against a $74 million circulating market cap is a five times revenue multiple on a B2B infrastructure business with genuine switching costs. When a project like Starknet routes its entire investor vesting schedule and community airdrop through your smart contracts, migrating away mid-cycle carries enormous operational and legal risk. These clients are functionally locked in during their distribution windows. That is sticky revenue and the market is pricing it like it barely exists.

I have also spent a lot of time thinking about the investor backing and what it implies about what those investors actually found when they looked carefully. Sign has raised over $30 million from YZi Labs, Sequoia Capital across the US, India, and China divisions, and other top investors. The Sequoia detail specifically is unusual enough that I think it deserves honest attention rather than being dismissed as name-dropping. All three Sequoia divisions operate with separate capital pools, separate mandates, and separate conviction requirements. Getting three independent investment committees to agree simultaneously on the same early-stage crypto infrastructure bet is genuinely hard. It tells me the diligence process surfaced something beyond a standard Web3 pitch, and that multiple teams of serious people looked carefully at the government contract pipeline and decided it was credible enough to write meaningful checks.

The government deployment track record is where my thinking gets most complicated because I have personally watched enough sovereign blockchain partnerships evaporate in this industry to be deeply skeptical of the category by default. The 2021 to 2022 cycle left a trail of announced government relationships that generated price pumps and then quietly died without delivering anything real. So when I found that Sign implemented solutions through live government partnerships in the UAE, Thailand, and Sierra Leone in 2025, my first instinct was to assume these were announcement-level relationships dressed up as deployments. But when I dug into the Sierra Leone situation specifically something landed differently for me. In Sierra Leone 73% of citizens have identity numbers on file but only 5% hold functional identity cards, meaning 66% of the population is excluded from formal financial services. That gap between documented and credentialed is exactly the infrastructure failure that Sign's SignPass product was built to close. The product-problem fit there is not manufactured for a pitch deck. It is a genuine national infrastructure crisis that maps directly to what the technology does.

What I cannot stop thinking about though, and what I keep trying to interpret honestly rather than conveniently, is that the Sign team deposited $9.3 million worth of SIGN tokens to Binance. I have been going back and forth on how much weight to give this for weeks. Teams convert tokens to operating capital all the time and it does not automatically mean anything alarming. But the people with the lowest cost basis and the largest allocations moving that much supply to an exchange is a directional signal I cannot just ignore to make the thesis feel cleaner than it is. It sits at the back of my head every time I find myself getting more constructive on the token and I think that discomfort is actually appropriate rather than something to reason away.

There is also a 49.17 million token unlock coming on March 31, 2026. Ten days from now. On its own that number is manageable. In the context of everything else it is another data point pointing in the same direction as the supply pressure that has been the dominant price force since the TGE.

Where I actually land after three weeks of sitting with all of this is genuinely in the middle, and I think that is the most honest place to be right now. The market has correctly identified the supply problem and is pricing on it. What the market has not done is price the scenario where a national-scale S.I.G.N. deployment begins generating verifiable on-chain fee revenue from millions of sovereign users. That scenario has no real comparable precedent in crypto and markets have no framework for what it would be worth, so they have defaulted to pricing it at zero. That default might be correct. It also might be leaving something real on the table.

SIGN is currently underperforming not just the broader market but also similar Ethereum ecosystem tokens, which have been running meaningfully stronger over the past week. That relative weakness during sector strength tells me that sophisticated capital that understands this project is either not adding or actively distributing, and I have to respect that signal even when the fundamental story is compelling.

The only thing that would genuinely change my conviction level here is seeing verifiable on-chain fee revenue from a live sovereign deployment. Not another country signing a memorandum. Not another pilot announcement. Actual transaction fees flowing through SIGN infrastructure from a national system with real daily users. The team's stated ambition for 2026 is reaching more national governments to demonstrate that blockchain-powered national digital infrastructure is no longer theoretical but actually deployable in the real world. I believe they can do that technically. What I need to see is the revenue that proves governments are actually paying for it at scale.

Until that happens the token mechanics are genuinely hostile to existing holders regardless of how good the underlying story sounds, and I am not willing to pretend otherwise just to make the thesis feel cleaner. If you came here looking for a confident directional call I genuinely cannot give you one. What I can give you is exactly where my thinking actually is, which is that SIGN is doing something real and unusual inside a token structure that makes it very difficult to profit from that reality in the near term. Sometimes that gap closes. Sometimes it does not. I am still watching to find out which one this becomes.

@SignOfficial #SignDigitalSovereignInfra $SIGN