Every year governments allocate billions in subsidies, welfare payments, pensions, and emergency aid.

Most of it never reaches the people it was meant for.

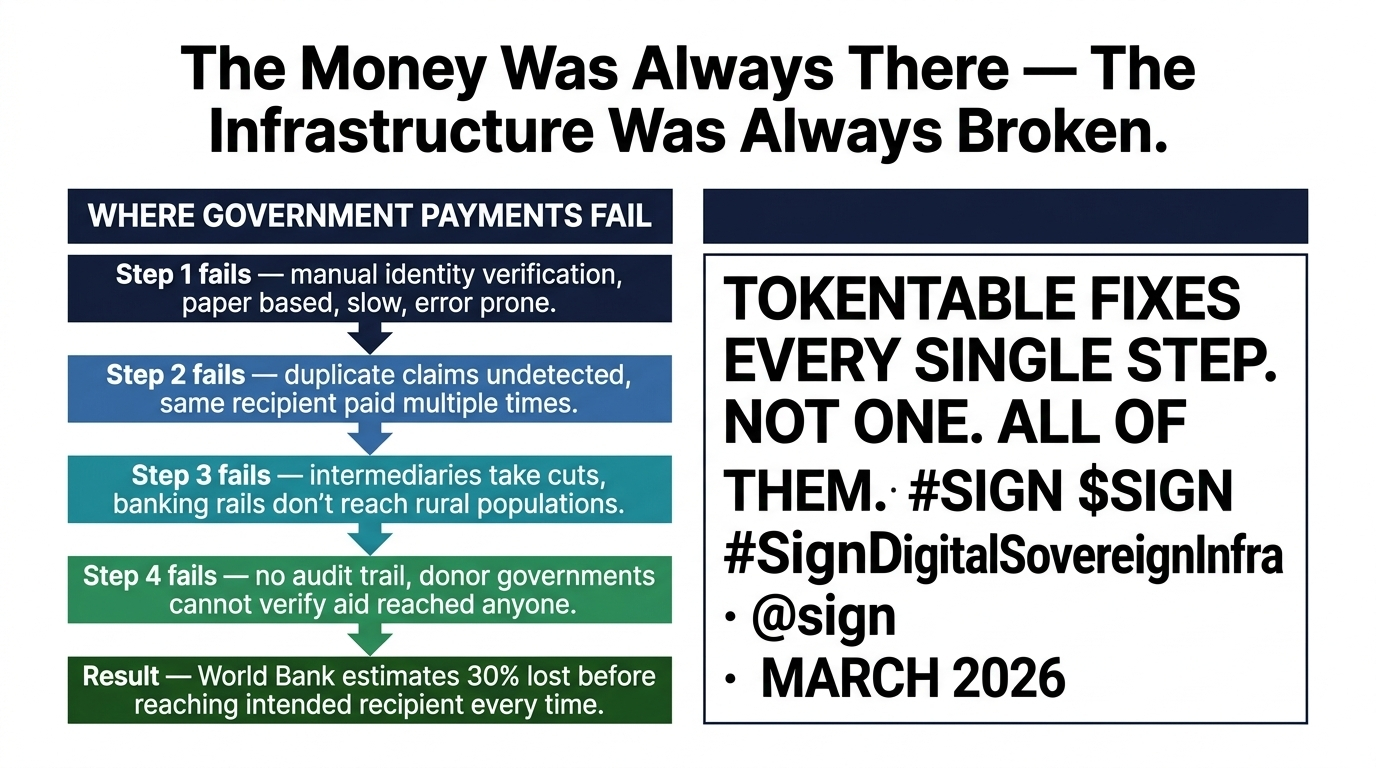

Not because the money disappears entirely. Because the infrastructure between the government and the citizen is broken at every step. Manual processing. Paper-based verification. Intermediaries taking cuts. Delays measured in weeks not hours. Duplicate claims going undetected. Fraudulent recipients collecting payments that should reach someone else.

The World Bank estimates that up to 30% of government benefit payments in developing economies are lost to leakage, fraud, and administrative inefficiency before they reach the intended recipient. That is not a rounding error. That is a structural failure baked into how governments move money.

TokenTable is built to replace that infrastructure entirely.

The numbers are not theoretical. TokenTable currently serves over 40 million users globally. That is not a pilot program. That is production-scale asset distribution running on real blockchain infrastructure for real government and institutional use cases.

Here is how it actually works.

A government allocating agricultural subsidies traditionally faces a multi-step problem. Identify eligible farmers. Verify their identity. Prevent duplicate claims. Process payments through banking infrastructure that may not reach rural populations. Audit the distribution afterward. Each step is a potential failure point. Each step introduces delay. Each step costs money that could have gone to the farmer.

TokenTable collapses that process. Identity verification happens through Sign Protocol attestations — the same on-chain identity layer that verified the citizen's digital identity in the first place. Eligibility rules are encoded directly into the distribution contract. Duplicate prevention is enforced technically — the smart contract simply cannot pay the same verified identity twice. Payment reaches the citizen's digital wallet directly. The entire distribution ledger is immutable and publicly auditable from the moment it executes.

The speed difference is significant. A traditional government payment cycle from allocation to receipt can take days to weeks depending on banking infrastructure. A TokenTable distribution to a verified address executes in seconds and finalizes immediately.

But the more interesting innovation is conditional logic.

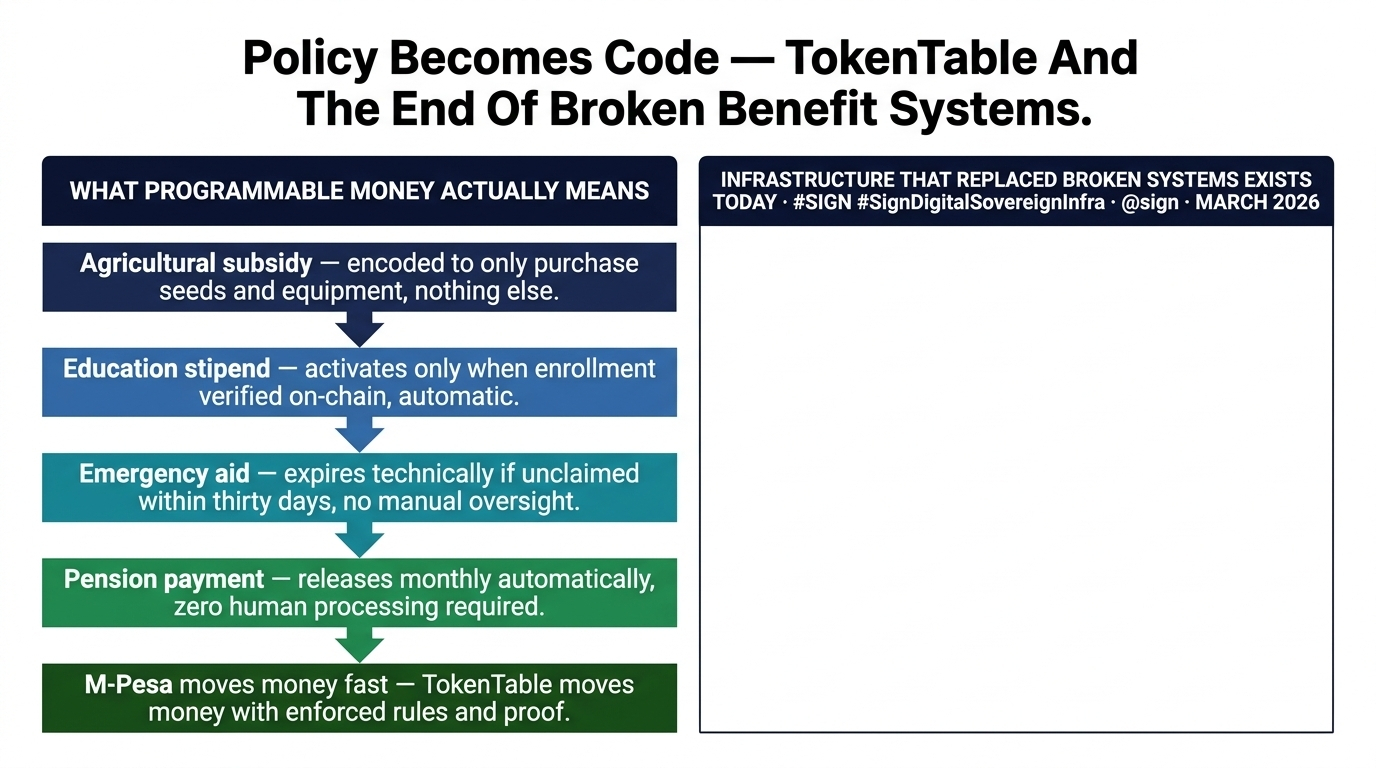

Governments do not just want to move money. They want to move money with rules attached. Agricultural subsidies that can only be spent on seeds and equipment. Education stipends that activate only when enrollment is verified. Emergency aid that expires if unclaimed within thirty days. Pension payments that release monthly without requiring manual processing. These are not complex requirements — they are standard government policy objectives. But current payment infrastructure cannot enforce them technically. The rules exist on paper. Compliance depends on human oversight.

TokenTable enforces them in code. The conditions are written into the smart contract. If the condition is not met the payment does not release. No human oversight required. No compliance team needed. The policy is the program.

The dual-chain architecture adds another layer of sophistication. Privacy-sensitive distributions — healthcare subsidies, mental health support payments, confidential assistance programs — route through Hyperledger Fabric X with zero-knowledge privacy. The recipient receives their payment. Nobody on the public ledger can see what the payment was for. Transparent distributions — public welfare, agricultural subsidies, education stipends — route through the public chain where anyone can verify the government allocated funds correctly and they reached the right people.

Same platform. Two privacy modes. Government chooses which applies to which program.

The competitive question here is honest and worth naming. Traditional fintech payment rails like M-Pesa in Kenya and GCash in the Philippines already serve hundreds of millions of people in developing economies with digital payments. They are fast, widely adopted, and require no crypto knowledge from users.

TokenTable's answer is programmability and auditability. M-Pesa can move money. It cannot enforce that the money is spent only on fertilizer. It cannot generate an immutable audit trail that proves to a donor government or international organization that every dollar of foreign aid reached its intended recipient. It cannot link payment to on-chain identity verification that prevents duplicate claims at protocol level.

Programmable money with enforced rules and immutable audit trails is a genuinely different product from fast digital payments.

Whether governments move fast enough to adopt it before traditional fintech consolidates around existing rails is the real question.

The infrastructure to replace broken benefit systems exists today.

The bottleneck is never the technology.

It is always the procurement cycle.