I have been trying to figure out what actually separates Sign Protocol from every other attestation project that shows up in my feed every few weeks. Most of them tell a clean story. Decentralized trust, verifiable credentials, the future of identity. Fine. But clean stories are cheap in crypto. What I kept coming back to was one number that nobody seems to want to dwell on for very long.

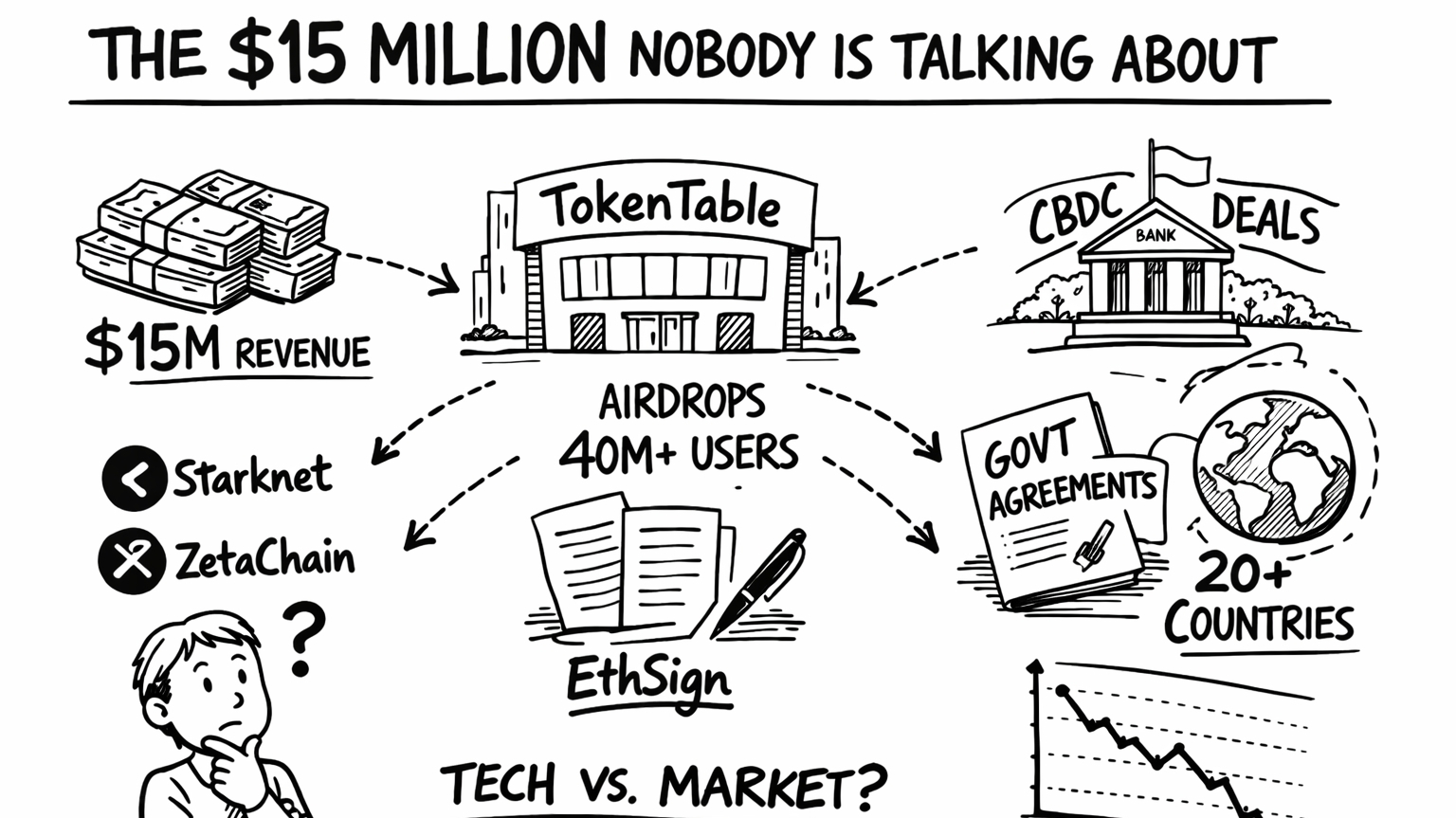

$15 million in real revenue. In 2024. From TokenTable alone.

That is not a grant. Not a VC check. Not a token treasury getting liquidated. That is actual money coming in from actual clients paying for an actual service. In a market full of infrastructure projects that have impressive whitepapers and zero users, that number sits differently. It changes how I read everything else about Sign.

TokenTable has facilitated over $4 billion in token airdrops across more than 40 million users and over 200 projects including names like Starknet and ZetaChain. Think about that for a second. When those projects distributed tokens to their communities, they trusted TokenTable to handle the mechanics. The vesting schedules, the unlock logic, the distribution rails. And they paid for it. That is not a narrative play. That is a business.

Here is what I find interesting about how this fits together. Most projects in the attestation space start with the protocol and then try to figure out the use case. Sign basically did it backwards. EthSign came first on-chain agreement signing, real users, real documents. Then TokenTable, which became the backend infrastructure for a significant chunk of crypto's token economy. Sign Protocol is the evidence layer that now sits underneath all of it, shared across sovereign and institutional workloads. The revenue was already there before the protocol became the main story. That sequencing matters.

But I am not going to pretend the picture is entirely clean. Because it is not.

SIGN hit an all-time high around $0.128 in September 2025 and has since dropped more than 75% from that peak. That is a brutal drawdown by any measure. And I have seen this pattern before in infrastructure tokens. The market prices in the vision early, the unlock pressure starts building, and suddenly the fundamentals that were supposed to be the floor do not hold the price where people expected. Right now, SIGN is unlocking roughly 96 million tokens on a recurring basis , which is consistent sell pressure hitting a market that is already digesting a lot. Whether the revenue growth absorbs that or not is genuinely an open question. I do not have a confident answer.

What I keep returning to is the government side of this, because that is where Sign is doing something I have not seen many protocols actually execute on rather than just announce. In October 2025, Sign signed a technical service agreement with the National Bank of the Kyrgyz Republic for the development of Digital SOM, the country's own CBDC. A few weeks later, they signed an MoU with Sierra Leone's Ministry of Communication, Technology, and Innovation to develop blockchain-based Digital ID and stablecoin payment infrastructure. These are not blog posts about potential partnerships. These are signed agreements with national governments who have specific infrastructure problems they need solved.

Sign products are now deployed in the UAE, Thailand, and Sierra Leone, with plans covering more than 20 countries and regions. When I first read that I was skeptical. Twenty countries feels like the kind of number you put in a pitch deck to make things sound bigger than they are. But the individual deal disclosures are specific enough that I find it hard to dismiss entirely. National banks do not sign technical service agreements with protocols on a whim. There is due diligence involved, legal exposure, institutional reputation on the line. The fact that these deals are getting done suggests the product is at least meeting a minimum bar for enterprise reliability.

The $25.5 million follow-on round in October 2025, again led by YZi Labs , is another signal I keep coming back to. YZi Labs backed the Series A and then came back in for more at a larger check. That is not standard behavior for investors who are just managing their existing position. It suggests they looked at the government pipeline, the revenue trajectory, the sovereign infrastructure thesis, and decided the bet warranted more capital. Could be wrong. But it adds weight.

The honest question underneath all of this is whether sovereign infrastructure is a real category or just a narrative that sounds important. I genuinely do not know. Governments move slowly. They procure differently than enterprises. They have compliance requirements that can stall even excellent technology for years. And the CBDC space specifically is one where national politics can completely override technical merit. A project can have the best attestation architecture in the world and still lose a government contract to a local vendor with worse technology and better relationships.

Sign's own documentation is refreshingly honest about this — the path to real infrastructure is never linear, and deployments evolve with policy, adoption, and interoperability constraints while remaining governable and auditable. That kind of language from a project's own docs is actually rare. Most teams will not write that clearly about deployment complexity because it does not help with token price.

So where does that leave me. I think the revenue story is real and it is underappreciated. I think the government deals are real and they are hard to replicate. I think the token pressure is also real and it creates a gap between the fundamental progress and the price action that may take a while to close, if it closes at all. Sign is building something that looks like it belongs in the long-term infrastructure stack of a more verifiable internet. Whether that is worth holding through the unlock schedule is a different conversation entirely.

The question is not whether the technology works. It clearly works well enough for 200 projects and multiple national governments to use it. The question is whether the market will care at the right time.