The financial markets witnessed a pivotal week between March 20 and March 26, 2026. While the broader cryptocurrency market often focuses on macroeconomic shifts and geopolitical forces, this specific week was defined by targeted regulatory developments in the United States. The spotlight turned intensely toward stablecoins.

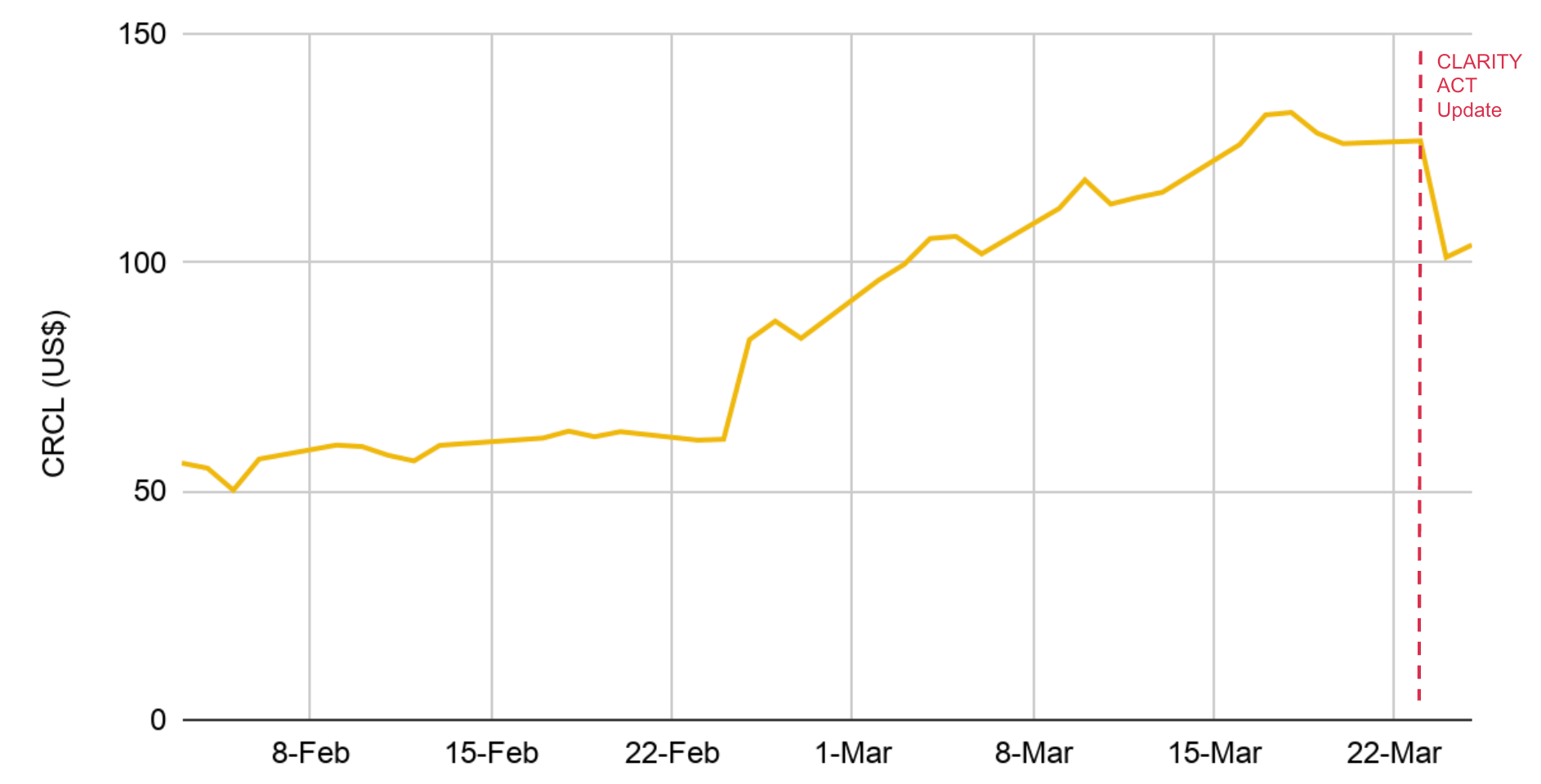

The catalyst for this shift was the introduction of the CLARITY Act and its proposed provisions regarding stablecoin yield. This legislative draft triggered immediate market reactions, most notably a historic 20% single-day decline in the stock price of Circle (CRCL) on March 24.

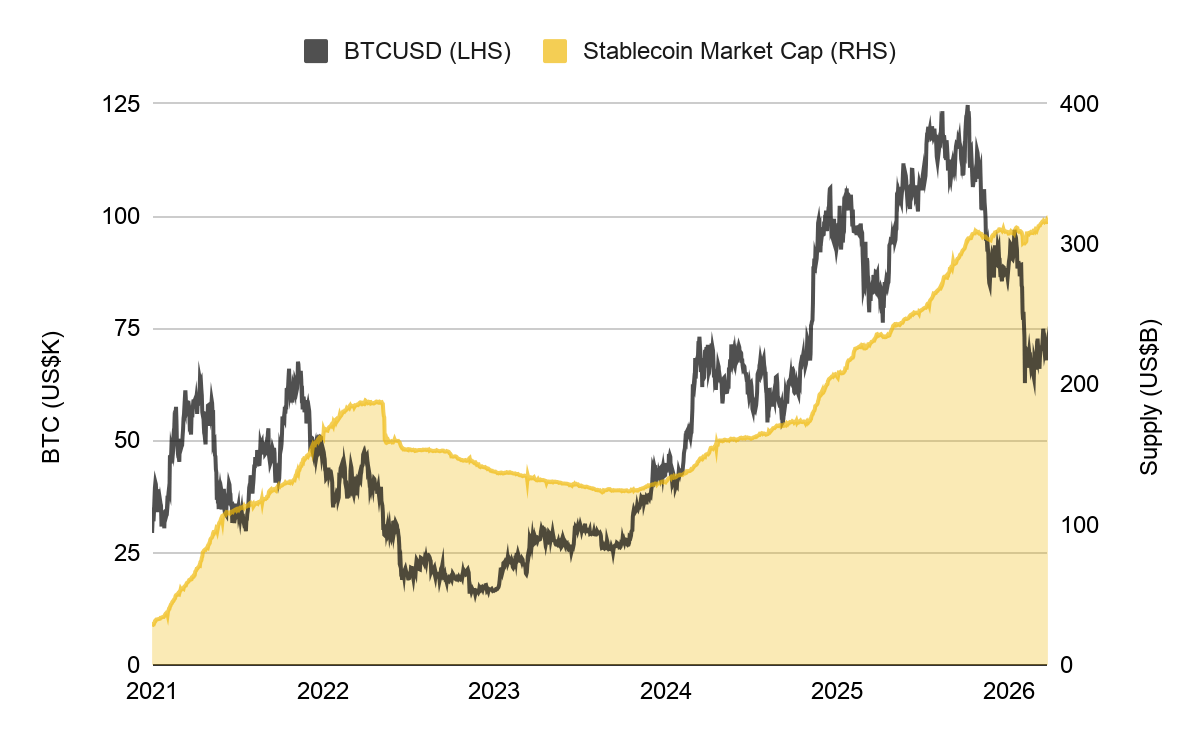

However, this market repricing reflects concerns over distribution economics rather than a drop in fundamental demand. The total stablecoin supply continues to climb, reaching an all-time high of approximately US$316 billion. This recap breaks down the intricate details of the CLARITY Act, its impact on traditional banking, the surprising decorrelation of stablecoins from Bitcoin, and the future of yield-bearing digital assets.

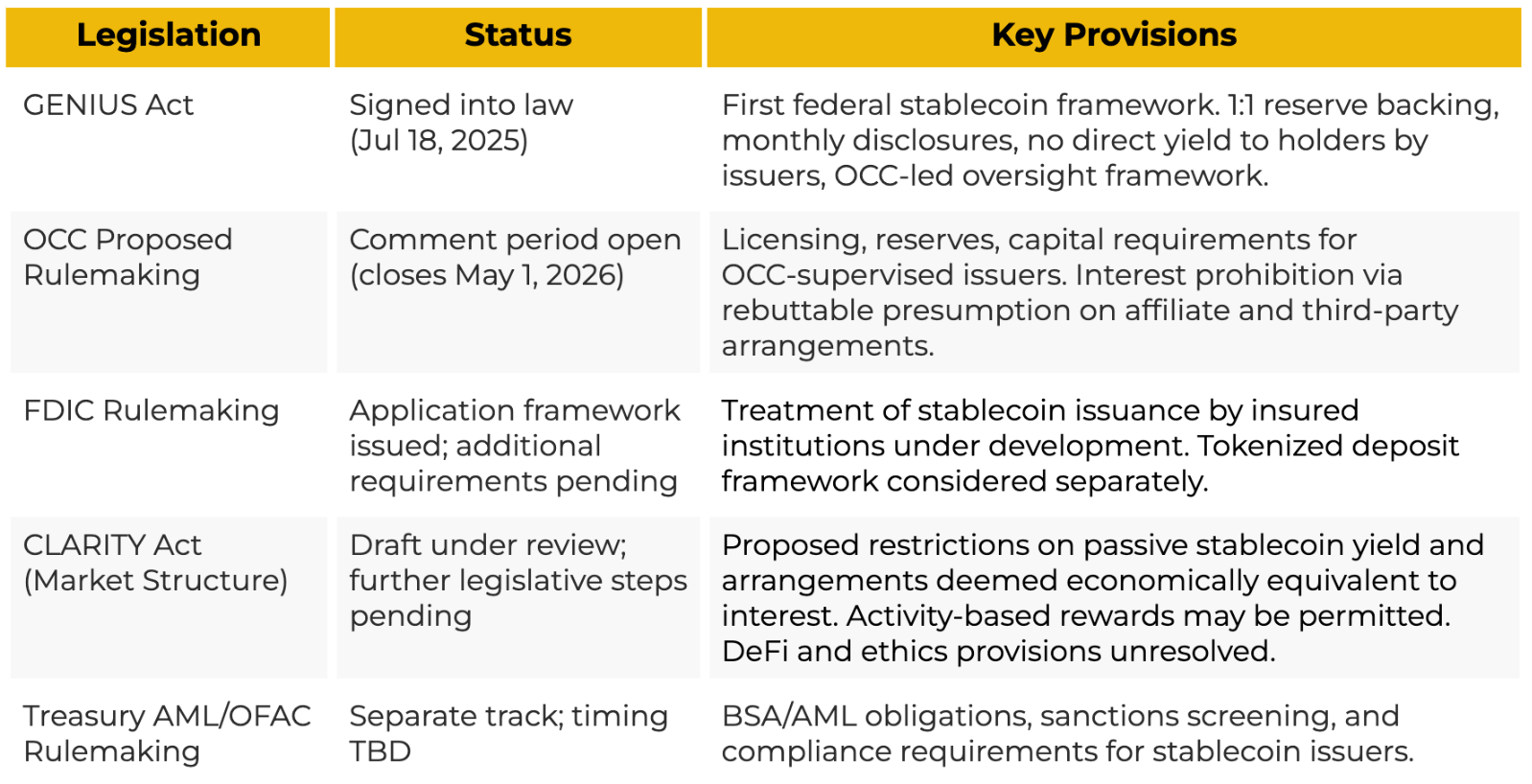

II. The Regulatory Landscape: From GENIUS to CLARITY

To understand the events of this week, we must look at the broader regulatory picture. The CLARITY Act does not exist in a vacuum. It builds upon the foundation laid by the GENIUS Act, which was signed into law last year. Together, these two pieces of legislation are shaping the federal framework for digital assets in the United States. On March 20, a bipartisan agreement regarding the yield provisions of the CLARITY Act was reached. By March 23, industry representatives were given their first look at the draft text.

The core issue within the proposed language is the sharp distinction drawn between passive yield and active yield. Under the new rules, simply holding a stablecoin balance to earn passive yield would face strict restrictions. Cryptocurrency exchanges, brokerages, and their affiliates would be barred from offering yield directly, indirectly, or in any format deemed economically equivalent to interest. However, using stablecoins for active ecosystem participation, such as payments or transfers, might still qualify for rewards. The exact mechanics of these allowed rewards remain undefined. The Securities and Exchange Commission, the Commodity Futures Trading Commission, and the Treasury Department would have a twelve-month window post-enactment to establish clear boundaries. In practice, this targets the pass-through model where issuers earn reserve income and share it with platforms to fund user reward programs.

III. The Banking Perspective: Deposit Disintermediation

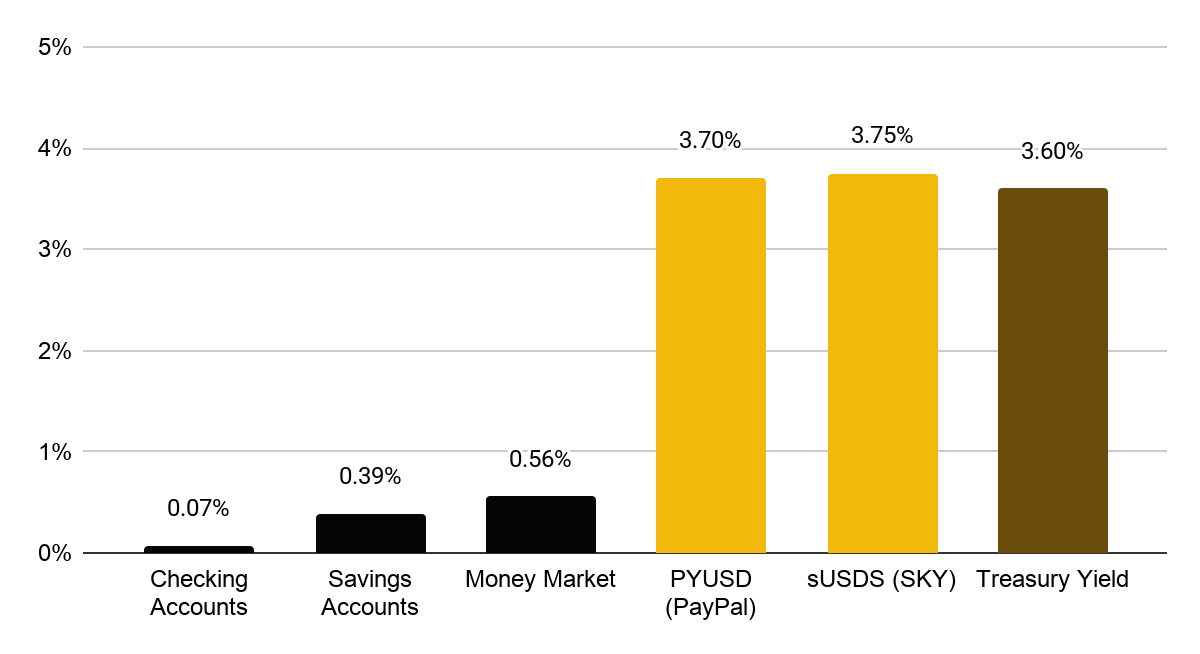

Why are regulators suddenly so focused on how stablecoins distribute yield? The answer lies in the traditional banking sector and the deposit disintermediation thesis. Banks fundamentally rely on a model of acquiring low-cost deposits from everyday savers and deploying those funds into higher-yielding assets like loans and government securities. With Treasury yields hovering around 3.8% to 4.0%, and checking accounts paying a mere 0.07%, banks capture a massive spread. This spread is the lifeblood of bank profitability.

Stablecoins represent a structural disruption to this highly profitable workflow. They introduce a highly competitive framework that drastically reduces the gap between what the financial system earns and what the end consumer receives. Over the past five years, approximately US$3 trillion in deposits have migrated from traditional banks to fintech platforms and neobanks. Stablecoins accelerate this trend by linking underlying yields directly to the users holding the assets. Financial analysts estimate that this level of stablecoin adoption could drive a significant runoff in core bank deposits over the next five years, reducing average bank earnings by approximately 3%.

Furthermore, fully reserved stablecoins primarily allocate their capital into sovereign assets like U.S. Treasuries rather than private sector lending. As capital shifts away from bank deposits, the pool of funds available for private credit creation shrinks. The two largest stablecoin issuers hold the vast majority of their reserves in U.S. government debt, tilting funding away from private lending and creating long-term structural headwinds for global credit markets.

IV. The Decorrelation of Stablecoins and Bitcoin

One of the most fascinating developments highlighted in this week's analysis is the fundamental strengthening of the stablecoin sector.

Historically, the supply of stablecoins moved in lockstep with the broader cryptocurrency market. It would expand during massive bull runs and contract when trading volumes and Bitcoin prices fell. Over the past year, that correlation has completely broken. Stablecoins have continued their relentless upward trajectory even as Bitcoin experienced a drop of more than 40% from its October 2025 cycle peak.

This decorrelation proves that stablecoins are no longer just a tool for trading crypto pairs. They have evolved into a mature infrastructure for global payments, settlement, and corporate treasury management. Recent institutional moves validate this shift. Major payment processors are acquiring blockchain infrastructure companies to connect stablecoin settlements across hundreds of countries. Multinational tech companies are expanding stablecoin functionalities across global markets. Regulation, starting with the GENIUS Act, has ironically served as an adoption catalyst by providing the institutional clarity required for massive enterprises to confidently enter the space.

V. The Rise of Yield-Bearing Stablecoins

The market reaction to the CLARITY Act highlights a crucial divide between utility-driven stablecoins and yield-driven stablecoins. The largest stablecoin in the world, Tether, does not pass yield through to its users. Its massive US$184 billion market cap has been built entirely on utility, proving that yield is not a strict prerequisite for massive scale. Many major stablecoin issuers do not pay interest, yet adoption has surged because they simplify moving dollars across borders.

However, the yield-bearing stablecoin segment has been the fastest-growing niche in the industry. Over the past year, the supply of yield-bearing stablecoins expanded from US7 billion to over US15.6 billion. Sky Protocol's USDS has been a standout performer, crossing the US$10 billion supply mark. Decentralized protocols generate yield differently than centralized pass-through models, utilizing on-chain lending, stability fees, and basis trade funding rates. How the CLARITY Act will ultimately treat decentralized finance yield remains a heavily debated open question. If decentralized finance yield is carved out, it could redirect capital toward on-chain protocols and structurally advantage those able to extract competitive yield for their users.

VI. 5 Key Takeaways

To ensure absolute precision regarding the findings of the Binance Research report, here are the exact insights extracted from the analysis:

Stablecoin supply has reached ~US$316B and is growing independently of broader crypto, driven by a combination of yield, payments and institutional adoption.

The direction of U.S. stablecoin regulation, from the GENIUS Act through to the CLARITY Act, is increasingly defining the rules for how stablecoins compete for capital and distribute yield.

Holding a stablecoin and earning yield simply for having a balance would be restricted. Exchanges, brokers, and affiliates would be restricted from offering yield directly, indirectly, or in any manner "economically equivalent to interest."

The push for tighter restrictions on stablecoin yield is ultimately about deposit funding economics. Banks rely on low-cost deposits, paying minimal interest to savers while deploying those funds into higher-yielding assets such as loans and securities.

The yield-bearing stablecoin segment has been one of the fastest-growing in crypto. Among the leading players, supply has expanded from approximately US7B a year ago to over US15.6B, now accounting for nearly 5% of the total stablecoin market.

VII. Looking Ahead

The trajectory of the CLARITY Act over the coming weeks will undoubtedly define the near-term outlook for the entire digital asset sector. The regulatory debates happening right now prove that the stablecoin market has matured to a point where legislative design choices have immediate, multi-billion-dollar consequences.

With a market capitalization of US$316 billion, stablecoins now have direct linkages to U.S. monetary policy and global bank funding markets. The central question surrounding the CLARITY Act is what stablecoins will be allowed to become in the future. Will they be restricted to simple payment instruments, or will they be permitted to evolve into full-spectrum financial products that directly compete with traditional bank deposits? The answer to this question will dictate the next chapter of the global financial system. Investors and market participants must pay close attention to the legislative markup sessions scheduled for late April, as any delays could push this critical regulatory framework into the post-midterm election cycle.

© This writing piece is originally published by Binance Research. We are just put our thoughts and include some opinions on it. We don't hold any rights or authority of it.