I’ve been quietly watching $SIGN for the better part of a year now, the way you keep an eye on a project that feels like it’s operating on a different timeline than the usual hype cycles. What keeps pulling me back isn’t the grand vision on the website or the partnership announcements everyone else quotes. It’s something quieter in the token’s own market structure: the way this low-float setup has quietly built a kind of self-reinforcing demand loop that most people seem to be reading completely backward.

Here’s the non-obvious thing I’ve landed on. The market is treating $SIGN’s current scarcity like a fragile party trick that’s about to end with the April 28 backer unlock. I see the opposite. That same constrained supply, paired with the kind of daily trading volume that would look ridiculous on a larger float, is actually the earliest evidence that real credential verification and token-distribution activity is already generating sticky, protocol level buying pressure. The unlock isn’t dilution risk; it’s the moment the token gets enough liquidity to let that early demand breathe and scale.

Let me walk you through how I got there, just the numbers I keep coming back to.

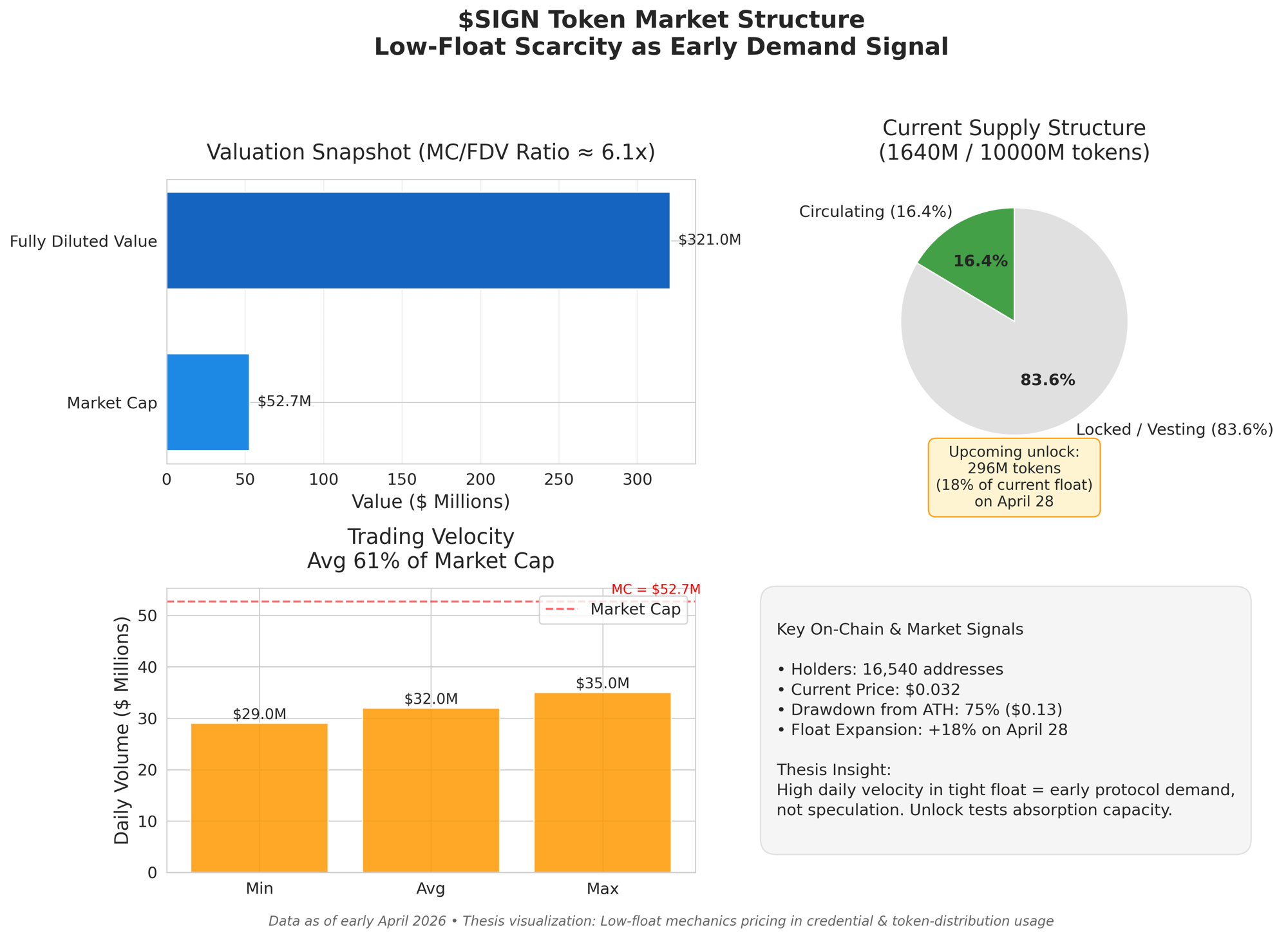

Right now the token trades at roughly $0.032 with a market cap of about $52.7 million against a fully diluted valuation north of $321 million. That six-times gap isn’t some abstract future overhang; it’s the direct result of only 1.64 billion tokens 16.4 percent of the 10 billion total being in circulation. What matters here is how the market has been pricing that scarcity. Instead of treating it as temporary, the price action suggests participants are already betting that the utility layer will grow into the supply schedule rather than the other way around.

Look at the volume. We’re routinely seeing $29–35 million traded in a single day. That’s north of 60 percent of the entire market cap turning over daily. In most low-float names that kind of turnover screams pure speculation. With SIGN it feels different because the project’s whole point is moving verifiable credentials straight into executable token flows. High velocity here starts to read less like churn and more like early users and pilots actually testing the rails attestations getting issued, small capital programs settling, proofs being verified. The float is so tight that even modest real usage shows up as outsized volume.

Then there’s the holder base: just 16,540 addresses. On paper that looks narrow for something positioned at national-infrastructure scale. But zoom in and it tells a cleaner story. These aren’t thousands of tiny retail bags being flipped; the concentration is still early-participant heavy, the kind of wallets that tend to hold through noise because they’re tied to the actual product. That base hasn’t been diluted yet. It’s still small enough that any genuine uptick in protocol usage new schemas live, new grants distributed, new sovereign pilots—will register as visible holder growth instead of getting lost in the noise.

Price itself is sitting about 75 percent off the September 2025 all-time high around $0.13. Normally that would make me cautious. Here it feels like the drawdown happened on the original low-float hype and has since stabilized precisely because the underlying mechanics (volume to float ratio especially) never really broke. The token has been holding this range while the broader market has done its usual dance. That resilience strikes me as more meaningful than another green candle.

And then the unlock itself. On April 28 roughly 296 million tokens about 18 percent of today’s circulating supply are scheduled to hit the market from backers. At current prices that’s around $9.5 million of supply. Plenty of analysts are framing it as the big risk event. I keep seeing it as the release valve. Backers have been locked since genesis; their exit isn’t panic selling if the demand side is already showing up in the volume data. More importantly, that extra liquidity could be exactly what lets new participants enterprises, smaller governments, even retail users interacting with the credential layer actually enter without moving the price 20 percent in either direction.

Of course the counterargument is fair and I hear it all the time: “History shows first major cliffs rarely get absorbed cleanly, especially in infra tokens.” Fair enough. If the volume dries up post unlock or the same absolute dollar flow suddenly looks tiny against the new float, then yeah, the whole scarcity narrative was just smoke. I’m not blind to that.

What would actually confirm my view over the coming weeks is straightforward. If price holds or grinds higher through the event window, if daily volume stays elevated as a percentage of the new larger float, and if we start to see the holder count tick up meaningfully instead of flat-lining, that would tell me the protocol demand I think is already latent is finally showing up in the open. The opposite clean breakdown on sustained volume with no quick recovery would mean the float was the only thing holding it together and I’d happily admit I got it wrong.

I’m not here to sell you the next moonshot narrative. I’m just sharing where my own conviction sits after staring at the same dashboard for months. SIGN isn't priced on perfect future adoption yet. It’s priced on a market structure that has forced early conviction to matter more than it usually does. April 28 doesn’t break that structure it tests whether the structure was built on something real. So far the data keeps pointing the same way, and that’s why I keep coming back to this one.

The simple takeaway for me: the token’s current setup isn’t a low-float gamble waiting to unwind. It’s a deliberate scarcity engine that’s already started to price in the very usage the project was built for. Everything after the unlock is just confirmation.

@SignOfficial #SignDigitalSovereignInfra $SIGN