A guy walks into a gas station with cash, pays a disgusting spread, scans a wallet, gets BTC, walks out. That was the product. Not elegance. Not cheap fees. Cash in, coin out, no Coinbase onboarding, no bank asking questions, no two-day wait while some compliance queue decides whether your account looks normal.

The whole thing breaks the second that walk-up cash trade turns into a mini bank interview.

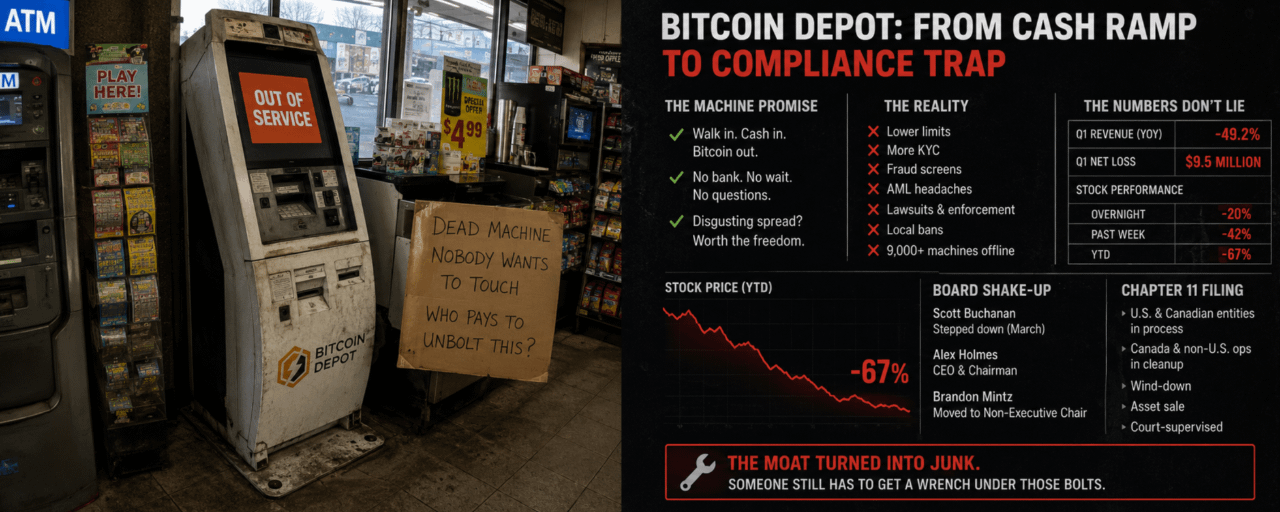

That is basically what happened to Bitcoin Depot. Lower transaction limits, more KYC, fraud screens, AML headaches, lawsuits, enforcement heat, local bans, operators getting treated less like kiosk vendors and more like money transmitters with a target on their back. The machine still has to sit there in the corner of the store, but now the customer flow is getting chopped up by warnings, ID capture, limits, and friction that kills the exact impulse transaction these boxes were built for.

So now there are 9,000-plus machines offline.

Picture the actual mess. A bodega owner has a dead Bitcoin box taking up space near the ATM and scratch-off tickets. A gas station manager has a bolted metal kiosk nobody can use and probably nobody wants to touch until someone explains who is paying to unbolt it, haul it, ship it, store it, or scrap it. These things are not browser tabs you close. They are metal, wiring, cash handling, service contracts, merchant relationships, compliance files, customer complaints, and a support line nobody wants to answer anymore.

BTM got smoked, down more than 20% overnight after already falling 42% the week before. Down about 67% on the year. The stock move was not some mystery reaction to a headline. Q1 revenue had already fallen 49.2% year over year and the company swung to a $9.5 million net loss. When a physical network loses that much revenue, the math gets nasty fast. Rent share still exists. Technicians still cost money. Cash logistics are still annoying. Fraud review does not get cheaper because fewer people are transacting.

The Chapter 11 filing in the Southern District of Texas just puts legal paperwork around what the machines already told you. The U.S. and Canadian entities are in the process, with Canada and non-U.S. operations getting dragged into their own cleanup. Wind-down. Asset sale. Court-supervised process. All the usual language.

The part that matters is simpler and worse. Bitcoin Depot built a cash-to-crypto business that needed volume, then had to operate in a market where volume became the dangerous part.

The CEO can say they tightened fraud controls and strengthened customer protection. I believe it. They probably had no choice. But once the customer has to stop, verify, read warnings, hit smaller limits, and wonder whether the operator is about to get sued or banned locally, the machine is no longer a quick cash ramp. It is a very expensive compliance screen bolted to the floor.

The board shuffle does not help the smell either. Scott Buchanan stepped down in March, Alex Holmes took over as CEO and chairman, Brandon Mintz moved out of the executive chair role into a non-executive seat. Maybe there are clean explanations for all of it. Markets do not give much benefit of the doubt when the chart is cratered, revenue is almost cut in half, and the company is preparing to sell off whatever is left.

The old bull-case was the footprint. More locations meant more access. More access meant more transactions. More transactions meant the ugly spreads could cover the overhead. Then compliance turned the footprint into a bill. More locations meant more machines to service, more local rules to monitor, more store owners to manage, more places where a regulator or lawyer could find a problem.

That is how the moat turns into junk in real time.

Someone still has to get a wrench under those bolts.