Retail is staring at XDC like something is about to break open, while the order books are still mostly shrugging.

That is the part worth paying attention to. CoinMarketCap search data recently had XDC ranking above Bitcoin, Ethereum, and XRP among most visited tokens. On its own, that is not a trade. Search traffic is cheap, and crypto has a long history of turning curiosity into nothing. But the mismatch is strange. The crowd is digging through XDC, trying to decide whether it is the cleanest way to express the RWA thesis, while actual trading volume has not caught up with the attention.

The majors are noisy in a way that makes them bad proxies for this trade. Bitcoin is never just Bitcoin anymore. It is macro, ETFs, liquidity, rates, dollar strength, political signaling, and whatever risk desk is being forced to explain crypto exposure that week. Ethereum has its own mess: staking, L2 value leakage, fees, upgrades, regulatory classification, institutional adoption that sometimes looks more like institutions borrowing the brand than using the rails. XRP has the payments crowd, the legal memory, the old loyalists, and a market structure that never really trades like a clean institutional infrastructure bet. XDC is getting searched because it looks narrower. Less baggage. More direct exposure to the question people are circling: which smaller network is actually close to tokenized real-world asset flow?

Maybe that is too generous. Retail often calls it research when it is really just ticker shopping. Still, the behavior is not random.

The RWA market is already past $33.7 billion, excluding stablecoins. That number matters less because it is large and more because it is now large enough for serious firms to stop pretending the category is just crypto people renaming structured products. BlackRock, Franklin Templeton, and JPMorgan have moved close enough to tokenized assets that the conversation has changed. Treasuries are the easiest starting point because they are liquid, familiar, and tolerable inside institutional risk committees. Gold-linked products and asset-backed credit are not far behind because they can be explained without turning the meeting into a DeFi vocabulary test.

Consensus Miami 2026 gave the market the same signal in a louder room. More than 20,000 attendees, firms connected to more than $4 trillion in assets, and tokenization kept coming up because the old rails are still embarrassing when you look at them closely. T+2 settlement is still hanging around. SWIFT correspondent chains still create delays that feel absurd next to the way markets actually price information. Custodians hand off assets, fund admins chase position files, transfer agents maintain their own records, internal books drift away from external reports, and then operations people get stuck explaining why four systems that should describe the same economic reality do not match. Add legal onboarding on top of that: investor eligibility, transfer restrictions, sanctions screening, jurisdiction checks, redemption rules, approvals, signed documents, stale KYC, and audit trails that look clean only until someone asks for the full path six months later.

This is the part crypto people understate because it is boring. It is also the part institutions actually care about.

XDC has a more credible claim than most chains that suddenly discovered RWAs after the narrative turned profitable. It launched in 2019 around trade finance, cross-border payments, and enterprise settlement. Not exactly a retail-friendly story, but probably closer to the real pain than another generic L1 claiming it can tokenize everything. As of May 2026, XDC holds more than $870 million in tokenized real-world assets. That does not make it the default RWA network. It does not prove durable demand. It does mean the chain is not only selling architecture diagrams and future-tense promises. There are assets sitting on it.

The distinction matters because static assets can flatter a network. Flow is different. A chain can look important because value is parked there, then fail the moment the question shifts to how often those assets move, who is moving them, whether issuance keeps coming back, whether redemption is clean, and whether the network is becoming part of a repeatable workflow instead of a one-off pilot that looks good in a conference slide.

I keep coming back to that gap when looking at XDC: the asset base is real enough to avoid dismissing it, but the market still needs proof that this is becoming rail activity rather than balance-sheet decoration.

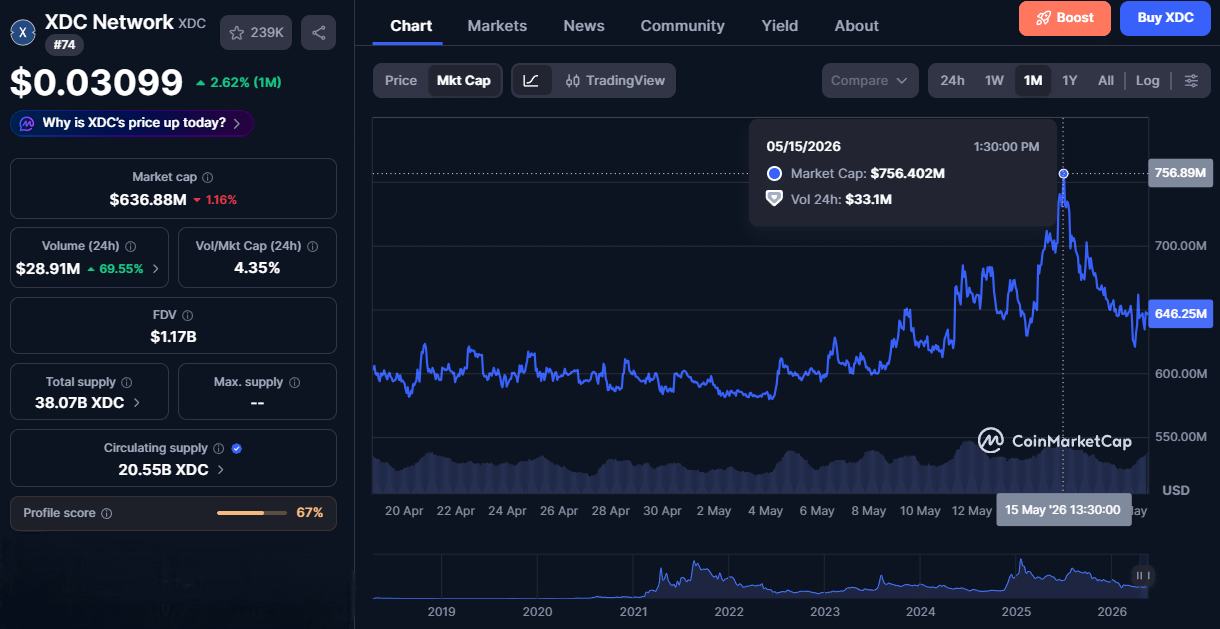

The $750 million market cap gives retail something easy to circulate. The 86% bullish sentiment reading on CoinMarketCap gives the community a mood board. Neither one tells an issuer where to route the next product. Neither one clears a redemption. Neither one answers whether XDC can handle the annoying parts of institutional tokenization without creating another reconciliation problem for the same back office it is supposed to help.

Compliance is where a lot of RWA commentary turns soft. People talk about compliant assets as if someone just adds permissions to a smart contract and the legal department goes home. The real version is messier. Who can hold the asset? Who can receive it? What happens if an address clears onboarding today and fails screening later? Can a transfer be stopped without breaking investor expectations? Can redemption be paused without creating legal exposure? Can the issuer show the regulator exactly who touched the asset, when, why they were eligible, and which off-chain obligation the token movement represented?

Banks do not need another sandbox that works only when everyone behaves perfectly. They need custody reporting, fund accounting, identity checks, internal controls, tax handling, transfer restrictions, redemption logic, and reconciliation against off-chain systems that are not going away just because a token exists. If the chain gives them faster settlement but forces three new manual checks downstream, the savings disappear.

Trade finance is even worse because delay is baked into the structure. Documents, shipping timelines, counterparties, collateral checks, fraud controls, country risk, payment timing, and legal enforceability all sit inside the workflow. Cross-border settlement is not slow because banks forgot speed exists. It is slow because every participant has a reason to protect itself, and protection keeps adding process. XDC’s focus there is relevant, but relevance does not equal capture. The network has to prove it removes friction in the live process, not just that it describes the friction accurately.

Institutions will not be loyal here. They will test multiple rails, compliment several in public, let procurement drag on forever, and then route actual volume through the option that creates the fewest new problems. A loud community can help a token trade for a while. It cannot make an operations team tolerate bad reporting, failed transfers, broken controls, or messy exception handling.

That is why the current attention around XDC is both interesting and fragile. Retail is trying to front-run an institutional plumbing trade before the data becomes obvious. The RWA category is real. The $33.7 billion market is real. The BlackRock, Franklin Templeton, and JPMorgan validation is real. The $870 million on XDC is real enough to deserve scrutiny.

But the next test is not narrative quality. It is volume, repeated usage, and visible movement tied to actual issuance, redemption, settlement, collateral, or trade finance workflows.

If the next quarterly on-chain volume reports print flat, that 86% sentiment reading will not drift lower. It will gap down.