By the time a company says, “we were already investigating,” the damage is usually sitting in a folder somewhere with a date stamp on it.

That is the line in Richard Teng’s response that would make me nervous if I were sitting inside Binance’s legal department. Not the denial, not the “fundamental inaccuracies,” not even the sanctions-timing argument. Those are expected. The dangerous part is the admission that Binance had already opened the hood before The Wall Street Journal knocked. Once you say that, every bored analyst note, every half-escalated case, every Slack message from December 2025 starts to matter.

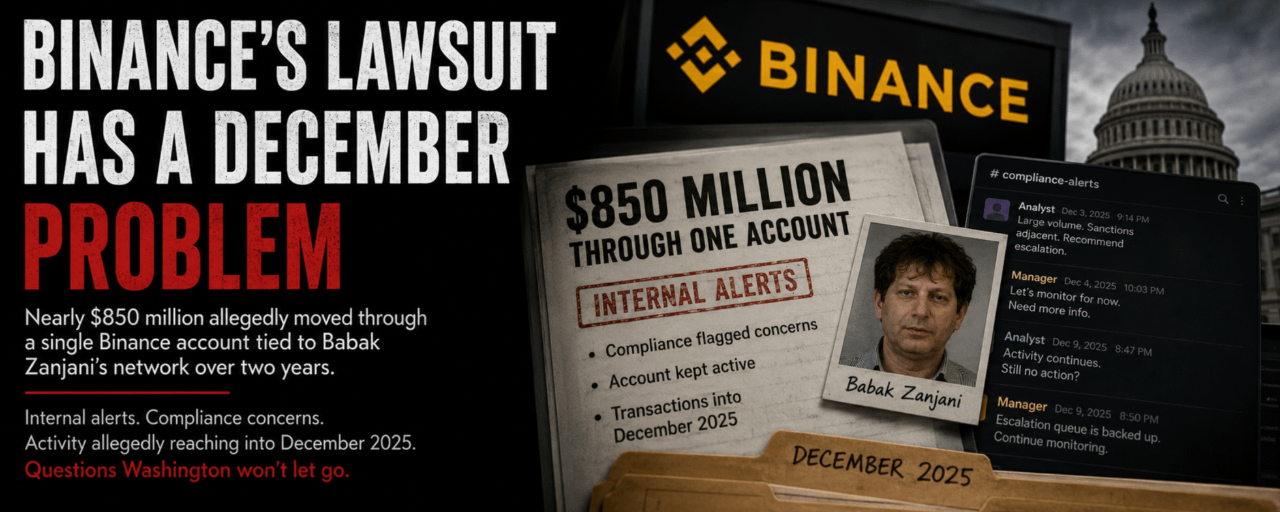

And the Journal’s allegation is not small enough to get lost in process fog. Nearly $850 million allegedly moved through a single Binance account tied to Babak Zanjani’s network over two years. One account. Not a swarm of dusty wallets spread across five chains and three mixers. One account sitting inside the world’s biggest crypto exchange, reportedly carrying Iran-linked flow while compliance staff flagged it more than once.

That is the kind of fact pattern that ruins sleep.

The corporate defense is trying to live in the clean legal lane. Teng says Binance did not permit sanctioned individuals to transact on the platform. He says the relevant transactions happened before the people involved were sanctioned. He says the company was already looking into the matter before the Journal reached out. Fine. Sanctions lawyers care about dates because dates decide cases. A transaction one week before designation is not the same thing as a transaction one week after. Nobody serious should pretend otherwise.

But I have spent too much time around financial investigations to believe the date alone ends the discussion. A compliance failure rarely looks like a villain stamping “approved” on a folder marked terror finance. It looks like a manager on a Thursday night deciding not to freeze a large account because the monitoring system has been screaming all quarter, 90 percent of the screams are garbage, and the desk is already furious about blocked flow. The analyst sees something off. The account has history. The explanation is not clean, but not clean enough for action is a very common category in crypto compliance. Someone writes a careful note. Maybe they push it up. Maybe the next person asks for more review. Maybe everyone waits for a harder match because nobody wants to shut down a whale-sized account on a sanctions-adjacent smell.

Then the name Babak Zanjani shows up in a subpoena packet and everyone starts acting like the system was always supposed to catch what it apparently learned to tolerate.

That is why the $850 million figure is so hard to scrub with language. At that size, the issue is not whether an alert existed. There are always alerts. The issue is how many times the institution looked at the same discomfort and found a way not to stop the account. The Journal is saying Binance’s own compliance people had flagged concerns. If that reporting holds, the company’s problem moves from “we missed it” to “we saw pieces of it and kept processing around it.” Those are very different conversations when federal investigators are in the room.

Binance also did itself no favors by suing the Journal in March. That move may have made sense to the people paid to fight reputational fires. The Journal had already reported in February that Binance facilitated more than $1 billion in transfers tied to Iranian operations, and Binance clearly wanted to shove the dispute into the safer terrain of media conduct and misreporting. Attack the process. Attack the framing. Make the paper defend itself.

Then the next story arrives with the kind of detail lawyers hate because it is not atmospheric. It is account-level. It has a named Iranian financier. It has an almost absurd number. It has internal warning signals. It has activity allegedly reaching into December 2025, which is not some ancient relic from the loose years. That is recent enough to drag in the cleaned-up Binance, the compliance-rebuilt Binance, the Binance that has spent years telling Washington it is no longer the old machine with a better logo.

The December detail is the poison. Inside a company, that is where people stop debating PR tone and start asking who still has message retention turned on. A Senate request for internal communications from that month does not feel like politics when you are the person whose name is on the review chain. It feels like nausea. People remember the joke they made in a channel. They remember the shortcut they took because everyone was overloaded. They remember saying “monitor for now” because freezing the account would have started a fight they did not have the authority or energy to win.

That is the part outsiders tend to miss. “We investigated” sounds responsible in a press response, but it creates a map for prosecutors. There was a first day. There was a person assigned. There was a reason the account was not killed then and there. There was probably a moment when someone saw enough to be uneasy but not enough to force the business to eat the loss. On day 47, maybe the case was still open, or reopened, or waiting for more information from a team that had already been reorganized twice. Maybe the account was generating enough volume that nobody wanted to move without a perfect sanctions hit. Maybe the compliance manager signed off because the tool had cried wolf all week and the escalation queue was backed up into the next quarter.

None of that fits neatly into “zero tolerance.”

Zanjani is not a normal name to have floating around a crypto compliance file. He is the kind of sanctions-evasion figure who changes the temperature of a review because the story around him is oil money, state pressure, shadow finance, and networks built to make formal controls look stupid. When a name like that is tied to a large account, people are supposed to slow down. If the Journal is right that Binance had internal concerns while the money kept moving, the company’s maturity pitch gets very thin very fast.

And Binance has been selling that maturity pitch hard. New leadership. Bigger compliance staff. Cooperation with law enforcement. More controls. More discipline. The post-settlement version of the company is supposed to be boring in exactly the places the old Binance was not. That is why this report stings. It does not just accuse Binance of having a dirty past. It asks whether the new machinery still lets the wrong account survive if the volume is large, the legal trigger is imperfect, and the internal file can be made to look busy enough.

Teng can keep arguing that the Journal left out context. Maybe it did. Binance can keep pointing to sanctions dates. Maybe those dates help. But if the DOJ starts walking the account backward, context becomes whatever was written before the lawyers arrived.

Somewhere, there is a compliance analyst who remembers the file, remembers the note, and is now wondering whether the Slack message they never deleted is going to be read aloud to a grand jury.