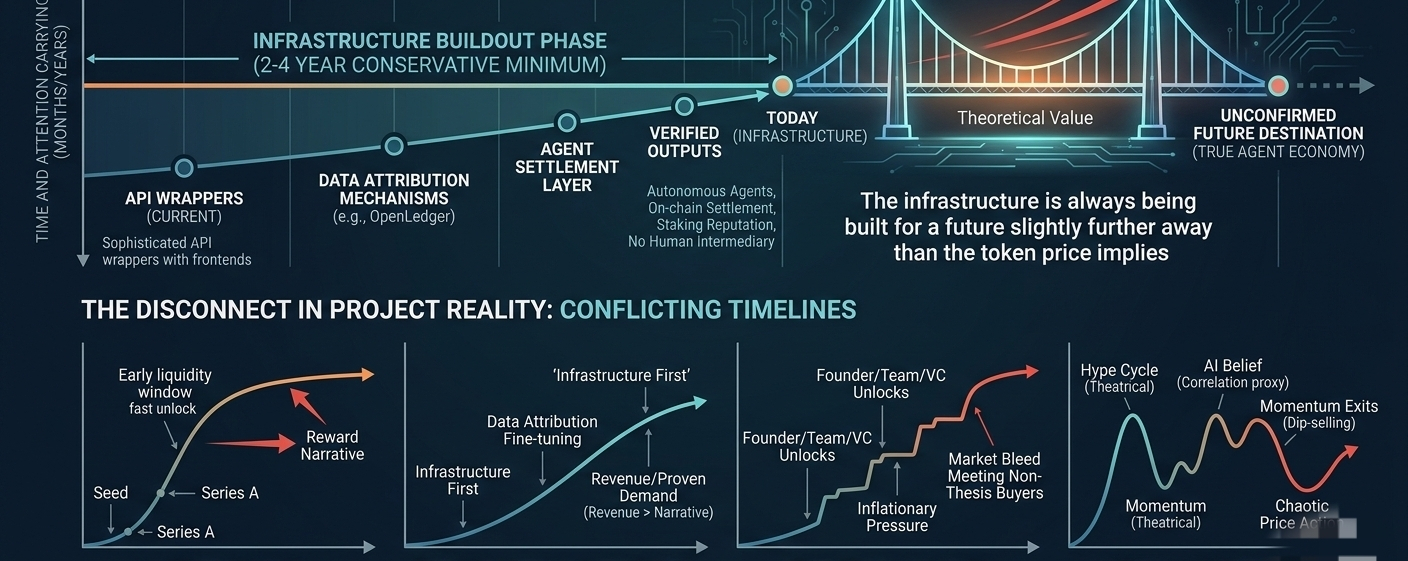

The agent economy angle is where things get more interesting and more dangerous at the same time. The idea that autonomous agents will need on-chain settlement layers, that they'll need to verify each other's outputs, stake reputation, pay for services without a human intermediary in every loop — this is genuinely compelling speculation that is probably correct on a long enough timeline. The problem i kos that we are still deeply in the phase where most things being called "agents" are sophisticated API wrappers with a frontend attached. The infrastructure is being built ahead of the actual agent economy by what is probably two to four years minimum, conservatively. Which is completely normal. Which is how infrastructure always gets built. But it creates a specific kind of positioning risk where you're holding a bridge to a destination that hasn't been confirmed yet, while paying carrying costs in both capital and attention that compound monthly.

"People say they want utility, but liquidity continues rewarding theater."

The on-chain attribution mechanism is what I keep coming back to as the most differentiated piece of the actual technical architecture. The claim is that OpenLedger can track data contributions to model training in a verifiable, tamper-resistant way — that when someone's data gets used to fine-tune a model, that relationship is recorded on-chain and can be referenced for compensation or governance purposes. If that actually works at scale, it solves a problem that is real and currently getting papered over with goodwill payments and vague promises from labs who have no actual mechanism for attribution. The labs have every incentive to keep this ambiguous. The moment attribution becomes technically verifiable, it becomes legally relevant, and the moment it becomes legally relevant, the free data extraction model starts facing structural pressure.

That's the interesting version of this story. Whether the market prices it before or after it's proven is the only question that matters for positioning.

· · ·

VC incentives are worth thinking about carefully here because they tend to shape the narrative arc in ways that aren't always visible from the outside. Projects in this category typically have investor structures where the early liquidity windows reward the narrative more than the metrics. You get well-placed coverage from people with aligned incentives, you get the right CT accounts amplifying at the right moment, you get exchange listings that bring temporary volume spikes, and then you get the slow mechanical bleed of unlock schedules meeting a market that has started looking at something else. The unlock schedule is usually the most honest document a project publishes, because it tells you exactly when different categories of holders will be in a position to exit — and that timeline rarely aligns neatly with the timeline on which the fundamental thesis resolves.

This isn't a critique specific to OpenLedger. It's the structural reality of how almost every project in this category gets brought to market. The incentives aren't necessarily misaligned in a malicious sense. It's more that the funding timeline, the product development timeline, the market narrative timeline, and the token unlock timeline are four separate curves that almost never peak at the same moment — and the holders who get hurt are usually the ones who assumed they would.

The retail psychology around AI tokens specifically has developed a split I haven't seen as cleanly in other sectors. There are holders who are believers in the AI macro trend and are using crypto exposure as a proxy for that belief because they missed the Nvidia trade and this feels like the next closest thing — which is a correlation that barely holds up under inspection but feels emotionally true in a way that's hard to argue out of. And then there are the pure momentum participants who don't care about the thesis at all and are reading chart structure and social volume and CT sentiment and positioning themselves accordingly. Those two groups create genuinely chaotic price action because they respond to completely different signals. The thesis believers buy the dip because the fundamental case didn't change. The momentum participants exit the dip because momentum is gone. And the resulting relief rallies that look like conviction are mostly short covering mixed with the believers averaging down — and the whole thing gets narrated afterward as "the market recognizing value" when it's really just two different time horizons colliding and creating a chart pattern that's optimistic from far away and ambiguous up close.

· · ·

The stablecoin flow picture for the AI sector broadly is in an interesting transition right now. For most of 2024 into early 2025, you had real inflows — capital that came in specifically for AI narrative exposure, not just rotated from other crypto sectors. Some of that capital has been sitting in positions that haven't worked the way the initial thesis suggested they would, and patience has limits. The question for something like OPEN entering the market is whether it's catching a rotation of that disappointed capital looking for a cleaner version of the same bet, or whether it's competing for attention and liquidity in a window where the available pool has contracted. Those are very different setups. One has a natural buyer base that's already primed. The other requires building a new buyer base from a more neutral starting point, which takes longer and requires sustained narrative maintenance that most projects can't execute well over the necessary timeframe.

What would actually change the calculus — not just for the trade but for the fundamental story — is if the data contribution model starts attracting real volume from entities that have genuine demand for provenance. If you see actual AI development teams paying into a system like this because the attribution mechanism solves a compliance problem or a quality-control problem that they're currently solving expensively in other ways, that's different capital formation than a well-designed whitepaper and a token. That's revenue. That's the separation between a project with a 12-month narrative runway and something that compounds quietly and then eventually starts showing up in conversations that matter. But that kind of announcement tends not to come before the listing pump. It comes during the slow middle period when most attention has drifted elsewhere — which is also when you find out whether the original believers had the conviction they thought they had.

"The infrastructure is always being built for a future that's slightly further away than the token price implies."

The exchange behavior around launch and early trading usually tells you more about the setup than the whitepaper does. Where the initial liquidity is concentrated, how the order book is structured in the first few weeks, what the funding rate dynamics look like as leverage enters — all of that gives you more signal about who's actually in this position and what their exit behavior will look like than any amount of tokenomics documentation. Projects that look healthy in their documentation frequently look different in their live order book. The paper and the market are describing the same thing from opposite ends and they rarely tell the same story.

· · ·

What I keep coming back to when I sit with OpenLedger as a market object is the question of the attention unlock. Not the token unlock schedule — the attention unlock. What's the event, or sequence of events, that causes a meaningful pool of capital to revalue this thing upward and hold it there long enough to matter? A partnership with a foundation model lab that has actual integration depth, not a memorandum of understanding that reads like a press release? An agent ecosystem that starts showing on-chain transaction volume that's attributable to real economic activity rather than test transactions and bootstrap incentives? An exchange listing during a macro window where the AI narrative has fresh legs and liquidity is seeking a place to express that view? Because right now the pitch is sophisticated enough to attract smart money — people who spend time with the architecture, understand the mechanism, believe the timeline — but not theatrical enough to attract the volume of less-informed capital that you actually need for price discovery to function in a way that rewards early holders. Smart money alone doesn't create a liquid market. It just creates a well-reasoned position waiting for a catalyst that may or may not arrive on a timeline that respects the position's cost basis.

The sophisticated thesis without the theatrical wrapper is a common trap. The market has seen too many of those to give them the benefit of the doubt automatically.

The thing that is genuinely novel about what OpenLedger is attempting — if the technical execution holds up — is that it's trying to build market structure for something that currently has no market structure at all. Data provenance has no liquid market. Model contribution has no standardized pricing. Agent labor has no settlement layer. OpenLedger is trying to be the infrastructure that makes markets possible for those things, which means it's not competing with existing infrastructure — it's trying to create demand for infrastructure in domains where the demand itself hasn't fully formed yet. That's a different risk profile than most projects in this space. It's also a different potential upside profile if the timing is right. The problem is that "if the timing is right" is doing enormous work in that sentence, and timing in early infrastructure is almost impossible to predict correctly and very easy to be right about eventually and wrong about in a way that matters for your actual position.

AI narrative intersecting with data ownership is the right idea at a potentially wrong time with a definitely crowded framing. That combination produces a specific kind of market outcome that's neither clean success nor clean failure — it's the long ambiguous middle where the people with the most patience and the most accurate read on timing eventually get rewarded, and everyone else either exits too early or holds through a drawdown that tests the limits of how much conviction they actually had versus how much conviction they thought they had when the thesis was easier to believe.

The market keeps rewarding theater. Not because the market is stupid. Because theater is what spreads. And what spreads is what gets priced. Whether what gets priced eventually reflects what's real — that part takes longer than most people's patience allows for.