The Ninth Circuit left Polymarket and Kalshi in the place they were trying hardest to avoid: state court, with Nevada and Washington regulators treating their event markets like gambling products that never bothered to get licensed.

That is a bad room to be in if your whole defense depends on sounding more like a derivatives venue than a sportsbook. The judges did not shut down the companies’ broader argument that the Commodity Futures Trading Commission should have the main say over event contracts. They just said, in effect, that the argument was not enough to yank these cases out of state court right now.

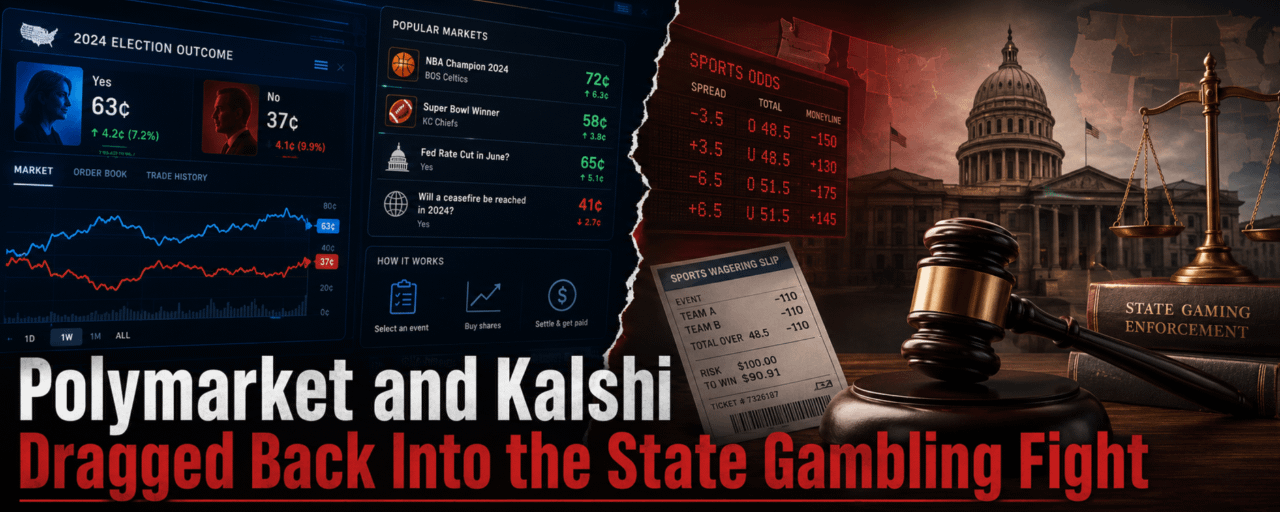

So the immediate problem is not a grand constitutional fight over the future of prediction markets. It is more boring and more dangerous than that. It is lawyers for venture-backed trading platforms walking into local court fights where the other side is talking about gaming licenses, consumer protection, sports betting rules, tax leakage and casino law. The CFTC may loom over the industry in Washington. A Nevada regulator looking at sports markets on an app has a much simpler description for it.

Unlicensed betting.

On Thursday, the Ninth Circuit denied emergency motions from both companies. Polymarket and Kalshi had asked the appeals court to pause lower-court rulings while they argued that Nevada and Washington’s lawsuits belonged in federal court. The panel was not convinced they had shown a strong chance of winning that removal fight.

The legal mechanics are dry, but the effect is not. The companies have been arguing that the Commodity Exchange Act and CFTC oversight should preempt state enforcement. The appeals court said that using federal law as a defense does not automatically create the kind of federal question that moves a case out of state court. Polymarket also tried the federal-officer route, arguing that because it complied with federal requirements it was operating under federal control. The judges were not interested. A private company does not become a federal officer just because it follows federal rules.

That leaves the platforms stuck in a strange split-screen. On investor calls, in policy conversations and across the usual crypto-finance chatter, prediction markets are sold as cleaner, smarter market infrastructure. Prices reveal information. Traders absorb risk. Regulators should not crush innovation because the product feels unfamiliar. Then the state cases arrive, and suddenly the argument has to survive in front of judges who are not reading the pitch deck and do not care how many people on Twitter think election odds are useful.

They are looking at sports contracts. They are looking at whether money is being staked on outcomes. They are looking at whether the company has a gaming license.

Polymarket’s week looked even worse because the court loss came alongside a reported private-key hack. That is not some separate crypto subplot. It cuts directly into the credibility problem. A company asking courts to treat it like serious financial plumbing does not want to be explaining, at the same time, how key management failed badly enough for hackers to get a shot at the operation. Regulators do not need much help making the “backdoor casino” argument when the tech side is producing the kind of security mess crypto was supposed to have outgrown by now.

Kalshi still has the New Jersey ruling in its pocket. Earlier this year, an appeals court there sided with the company and blocked state officials from restricting sports-event contracts on the platform. That matters, and it gives Kalshi a real case to wave around when states try to flatten everything into gambling law.

But New Jersey is not the whole country, which is the part the industry keeps running into. Maryland, Ohio and Nevada have been more comfortable letting gambling regulators press their claims. In April, Nevada Judge Jason Woodbury kept restrictions on Kalshi’s sports-related contracts in place, saying the products were substantially similar to wagers offered by licensed sportsbooks. That is the line Kalshi cannot finesse away with better branding. Once a judge says your contract looks like a sportsbook wager, the rest of the derivatives vocabulary starts sounding decorative.

The federal government is not exactly neutral here. The CFTC and the Justice Department have pushed back against some state enforcement actions, warning that aggressive state moves could interfere with federally regulated derivatives markets. That gives Polymarket and Kalshi useful ammunition, but not control of the battlefield. State regulators are still filing. State judges are still ruling. And now a House panel is investigating both companies while the courts are already split and the operating risk is getting harder to hide.

The ugly part is the logistics. Every state fight costs time, money and narrative control. Every ruling that compares event contracts to sportsbook wagers gives the next regulator another paragraph to copy. Every exploit or operational failure makes the “trust us, we are financial infrastructure” line a little harder to deliver with a straight face.

Somewhere, Kalshi’s lawyers now have to write the next state-court filing knowing Judge Woodbury’s “substantially similar to wagers” language is sitting there waiting for them.