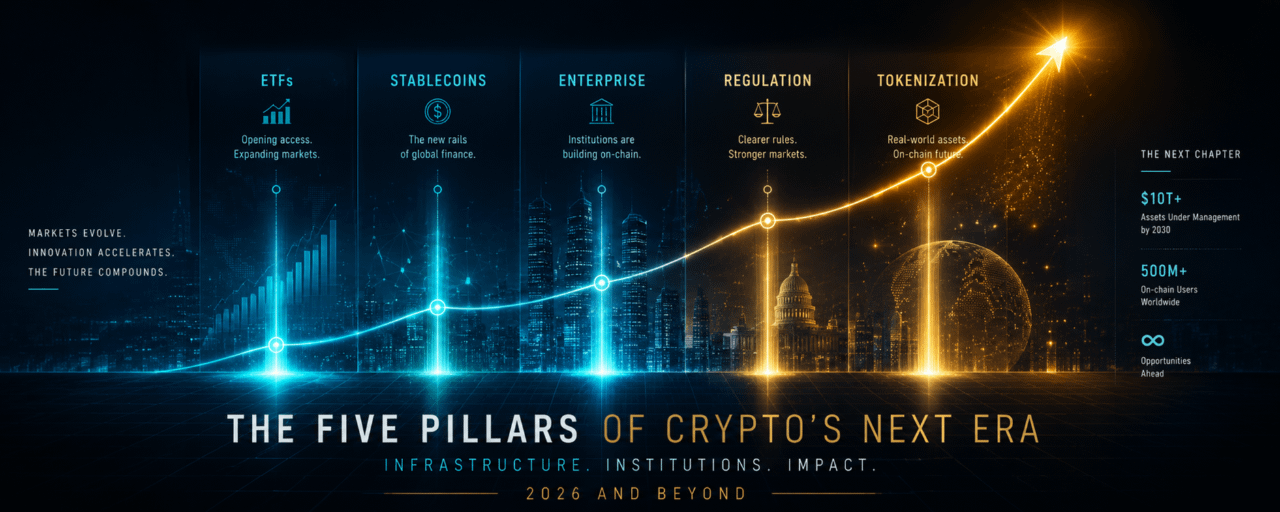

Forget the hype cycles and the crash headlines. Five structural shifts are quietly reshaping crypto from a speculative experiment into global financial infrastructure.

The Narrative Has Changed For most of its existence, crypto operated on a single, dominant story: this could be huge someday. That story attracted early adopters, fuelled speculative bubbles, and drove trillion-dollar market caps built more on possibility than on proof. And for years, critics were at least partially right to be skeptical — much of the activity was circular, speculative, and disconnected from real-world utility. 2026 feels different. Not because prices have gone parabolic (they haven’t — Bitcoin has traded in a wide range this year), but because the structural picture has shifted in ways that don’t reverse easily. The industry isn’t just bigger; it’s built differently. Here are five concrete signs that crypto has entered a genuinely new era.

Spot Bitcoin ETFs Are Now Mainstream Institutional Holdings The approval of spot Bitcoin ETFs in the United States in January 2024 was widely celebrated as a landmark moment. But the real significance has only become clear in hindsight. U.S. spot Bitcoin ETFs recorded approximately $22 billion in net inflows in 2025 alone, posting positive flows for seven months of the year. Ether ETFs added nearly $10 billion more. These aren’t retail day-traders — these are pension funds, endowments, RIAs, and family offices allocating to crypto through compliant, regulated wrappers for the first time. The GENIUS Act, passed in 2025, accelerated this further by establishing the first federal regulatory framework for payment stablecoins and clarifying how banks and financial institutions can issue and custody digital assets. The legislation effectively gave traditional finance a permission structure for engaging with crypto at scale. As Grayscale noted in its 2026 institutional outlook: fifteen years ago, crypto was a single asset with a market cap of roughly $1 million. Today, it’s an emerging alternative asset class with a combined market cap of approximately $3 trillion. The difference isn’t speculation — it’s institutional architecture.

The Stablecoin Market Has Crossed $310 Billion Numbers like “$310 billion” can feel abstract until you consider what they represent: a parallel, always-on, programmable dollar system that settles transactions 24 hours a day, 7 days a week, across borders, without clearing houses or correspondent banking delays. The total stablecoin market cap entered 2026 at a record $310 billion, led by Tether (USDT) and USDC, which together account for the vast majority of circulating supply. By May 2026, that figure had climbed further to approximately $320 billion. Stablecoin transfer volume reached $28 trillion in Q1 2026 alone. Annual stablecoin transaction volume crossed $4 trillion in 2025 — an 83% year-over-year increase. For context: Visa’s entire annualized network processes roughly $14 trillion. Stablecoins are no longer a rounding error by comparison. What’s changed isn’t just the volume. It’s the use case. In 2020, most stablecoin activity was crypto-to-crypto trading. By 2026, stablecoins are increasingly being used for B2B cross-border settlement, institutional cash management, and retail remittances. JPMorgan and BitGo have both expanded stablecoin-based settlement services. USDT and USDC now account for approximately 34% of all crypto-denominated cross-border transactions. The “stablecoin standard” — instant, low-cost, 24/7 dollar-denominated settlement — is increasingly the infrastructure that serious financial actors want.

Big Four Consulting Is Buying In — Literally On May 19, 2026, Deloitte — one of the world’s four largest professional services firms — acquired Blocknative, a cryptocurrency infrastructure company specializing in real-time mempool monitoring, gas fee prediction, and transaction management tools. The deal, structured as a talent acquisition, brings Blocknative’s specialized Web3 engineering team into Deloitte’s client services division, where they will focus on “driving Web3 innovation across Deloitte’s client portfolio.” Blocknative’s standalone API services will wind down by June 19 as the team pivots entirely to enterprise work. This might seem like a footnote. It isn’t. Deloitte already offers accounting, auditing, and corporate services for crypto firms. EY and PwC have built comparable practices. The acqui-hire of Blocknative represents something more pointed: a Big Four firm deciding that the talent required to build next-generation blockchain infrastructure is valuable enough to absorb directly, rather than contract out. When the firms that audit the Fortune 500 start acquiring crypto infrastructure teams, the “institutional era” isn’t approaching — it’s already here.

U.S. Federal Policy Has Shifted from Enforcement to Regulation For most of crypto’s history, the U.S. federal government’s relationship with the industry was defined by enforcement actions: SEC lawsuits, exchange settlements, exchange executive arrests, and repeated warnings that most tokens were unregistered securities. That posture has changed materially. The GENIUS Act established the first federal regulatory framework for payment stablecoins, allowing U.S. banks and financial institutions to issue and custody regulated stablecoins under structured oversight. The repeal of SAB 121 and the introduction of SAB 122 allowed banks to treat digital assets more like traditional assets — removing a significant accounting barrier that had kept major custodians on the sidelines. Crypto ETF approval timelines have accelerated. Regulatory clarity is deepening across trading, custody, and tokenization. The SEC, CFTC, and banking regulators are now building structured frameworks rather than pursuing case-by-case enforcement. This isn’t deregulation — it’s the opposite. It’s the construction of a regulatory architecture that makes it possible for institutional capital to engage with digital assets at scale, with legal certainty. That’s a fundamentally different operating environment than the one that existed two years ago.

Tokenized Real-World Assets Are Moving from Pilot to Production Perhaps the most consequential structural shift happening in crypto right now is the least discussed in mainstream coverage: the tokenization of real-world assets is quietly crossing the line from experiment to infrastructure. As of Q1 2026, tokenized U.S. Treasuries alone reached approximately $13–14 billion in on-chain assets. The broader tokenized RWA market has surpassed $25–32 billion depending on methodology — having more than tripled from $5.42 billion at the start of 2025. BlackRock’s BUIDL fund reached approximately $2.5 billion in assets under management and has now been integrated into DeFi rails, allowing a regulated Treasury fund to be used as collateral in decentralized lending protocols. In May 2026, BlackRock filed with the SEC for two additional tokenized fund structures, signaling a deliberate shift from individual pilot products to a diversified product line. As BlackRock CEO Larry Fink wrote in his 2026 annual letter, tokenization could help update the financial system by making investments “easier to issue, easier to trade, and easier to access.” The narrative, as one analyst put it, has shifted from “big banks exploring blockchain” to “big banks deploying products.” Tokenized real estate has moved from sandbox to secondary markets in Hong Kong and Dubai. Singapore’s MAS Project Guardian has reached operational roadmap phase. Morgan Stanley announced plans to support tokenized stock and ETF trading in the second half of 2026. Franklin Templeton, JPMorgan, and Ondo Finance are all in production. The “pilot” era of tokenization is over. What This Actually Means None of this makes crypto risk-free. Markets are still volatile, regulation is still evolving unevenly across jurisdictions, and significant execution challenges remain. But the five shifts above — institutional ETF adoption, a $310B+ stablecoin market, Big Four firms buying crypto talent, a federal policy pivot from enforcement to regulation, and tokenized assets crossing into production — represent something qualitatively different from previous cycles. Previous bull markets were built on speculation about what crypto could become. The current era is being built on proof of what it already is: settlement infrastructure, collateral, payment rails, and institutional capital allocation. The question is no longer whether crypto has a place in the financial system. The question is how large that place will be. The industry has entered a new era. The evidence is already in.