I want to be direct about something that’s been increasingly hard to ignore.

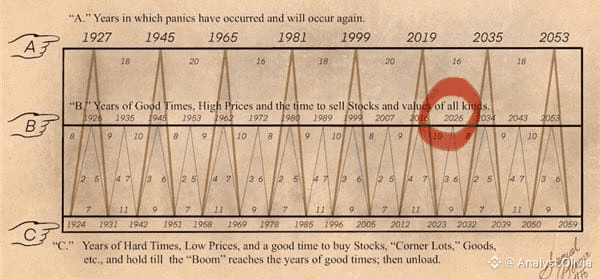

As we move toward 2026, the warning signs I’ve been tracking aren’t just flashing anymore , they’re starting to align. And what worries me isn’t a typical slowdown or a garden variety correction. It’s the structure of where the pressure is building.

This feels different.

The Bond Market Isn’t as “Calm” as It Looks

There’s a growing narrative that the bond market has stabilized. People point to declining volatility indicators and call it a win.

But lower volatility does not automatically mean lower risk.

What we’re seeing looks less like stability and more like compression, the kind that shows up before something breaks. The real stress isn’t in the front end of rates anymore. It’s concentrated in long-dated Treasuries, and that pressure is unresolved heading into the new year.

Long-term funding costs remain elevated, and the market is demanding a premium that hasn’t gone away.

Foreign Demand for U.S. Debt Is Quietly Weakening

This part matters far more than most people realize.

China continues to reduce its exposure to U.S. Treasuries. Japan, still the largest foreign holder, hasn’t exited,but its buying behavior has changed meaningfully. Currency volatility and domestic policy constraints mean every purchase is now conditional.

Historically, when foreign buyers stepped back, someone else absorbed the supply. Today, that margin for error is razor thin.

The system is still functioning, but the buffer is shrinking.

Japan’s Currency Stress Is a Global Risk Vector

For years, Japan was easy to ignore. That’s no longer the case.

A weakening yen forces policy responses that ripple outward, particularly through global carry trades. These strategies work quietly and efficiently, until they unwind. When they do, the stress doesn’t stay local.

Historically, the impact shows up most clearly in U.S. Treasury markets, where liquidity is assumed but not guaranteed.

Connect the Dots

Here’s the situation in plain terms:

Real yields remain uncomfortably high

Term premiums are elevated and sticky

Liquidity conditions are tighter than headlines suggest

Investors are pricing government level risk more seriously

Yes, equities can still rise. Gold can make new highs. Commodities can rally.

None of that contradicts what’s happening underneath.

By the Time It’s Obvious, It’s Already Over

This is the part most people misunderstand about financial crises.

By the time GDP data confirms trouble, or headlines declare a recession, markets have already repriced. The damage happens quietly , in funding markets, in spreads, in the plumbing, while attention is elsewhere.

What’s forming into 2026 doesn’t look like a routine slowdown.

It looks closer to a sovereign funding stress, the kind that eventually forces central banks back into markets, whether they want to or not, and whether they admit it or not.

The Timeline Still Makes Sense

The pressure points are exactly where financial stress has historically begun.

That’s why my focus hasn’t changed:

Watch bonds first. Everything else is secondary.

Bonds move before stocks.

Before commodities.

Before narratives.

Why I’m Saying This Publicly

I’ve called major market peaks before they happened. If and when I decide to exit markets entirely, I’ll say it publicly, not quietly, not after the fact.

Institutions charge enormous sums for this kind of analysis. I don’t believe this information should be hidden behind paywalls or gated access.

This isn’t fear-mongering.

It isn’t a sales pitch.

It’s pattern recognition, and history has a habit of rhyming when the structure lines up.

The data is there.

The signals are forming.

The only real question is whether we’re willing to pay attention before everyone else does.

Stay alert.

Stay informed.