I’ve been tracking Layer 1 payment chains since people genuinely believed Bitcoin would replace credit cards for coffee purchases. Most failed spectacularly. The few that survived usually abandoned payments altogether and pivoted into something safer, DeFi platforms, NFT hubs, or whatever narrative was selling that quarter. When Plasma launched its mainnet beta last September with zero-fee USDT transfers, I assumed Plasma would eventually follow the same script. Big claims, early hype, then a quiet shift once payment realities set in. That’s usually how these stories end. But Plasma hasn’t been behaving the way failed payment chains usually do, and that’s what keeps pulling my attention back.

What really started bothering me wasn’t the Plasma marketing narrative, but how Plasma validators were actually deploying infrastructure. Not slides about disrupting finance, but real capital commitments, validator behavior, and what those choices reveal about long-term conviction inside the Plasma network.

Right now $XPL sits at $0.1282, up 0.87% on the day with volume around 9.04M USDT. RSI is hovering near 55.97, neutral to slightly bullish territory. Price action alone isn’t impressive. What matters more is that $XPL is now trading above both the EMA(20) at $0.1271 and EMA(50) at $0.1263 for the first time in weeks. That shift suggests accumulation rather than random volatility. Buyers stepping into Plasma here don’t look like short-term traders chasing candles. It looks more like patient positioning after months of brutal downside.

The Plasma protocol itself uses PlasmaBFT consensus, a two-round Byzantine fault tolerant design that removes unnecessary confirmation steps by proving HotStuff’s third phase isn’t always required. That efficiency matters because sub-second finality is non-negotiable if Plasma wants to compete with Visa or traditional banking rails on user experience. Plasma wasn’t built as a general smart-contract playground. It was designed specifically for stablecoin payments. EVM compatibility through Reth keeps developer friction low, but the architecture is optimized for throughput and predictable execution, not experimentation.

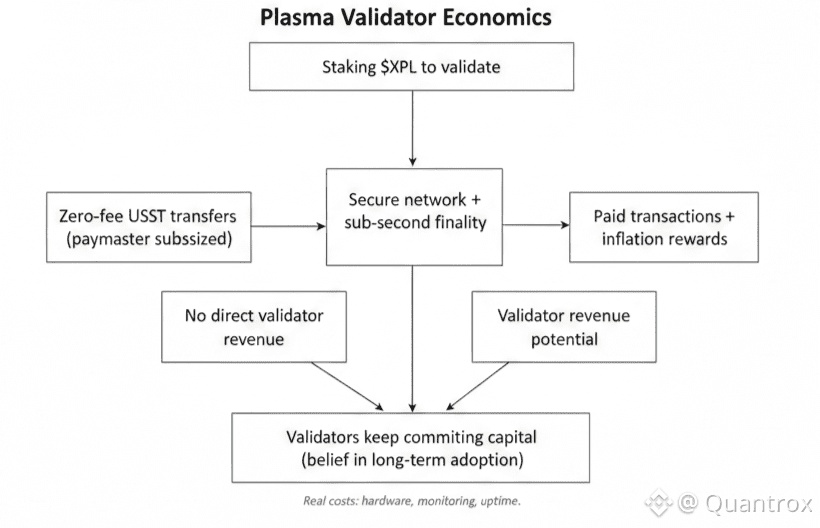

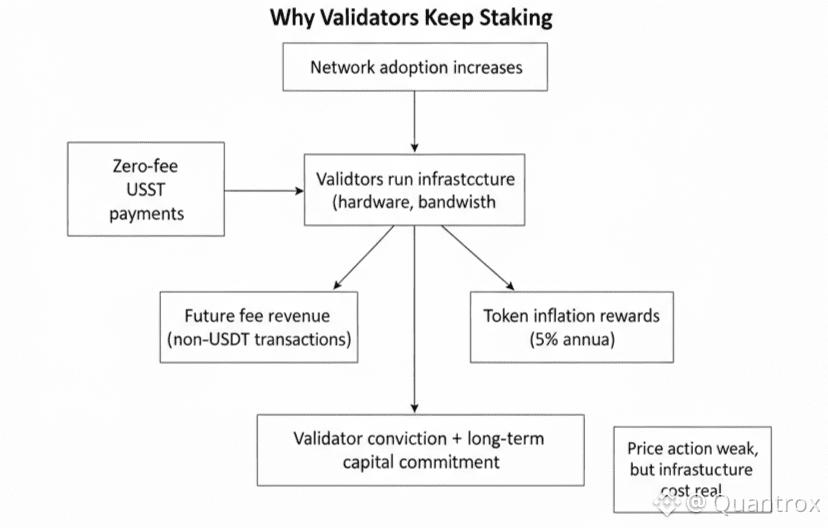

Validators on Plasma stake XPL to participate. That’s their skin in the game. They earn fees from non-USDT transactions that are burned via an EIP-1559 style mechanism, and they receive rewards from roughly 5% annual validator inflation. Structurally, it’s standard proof-of-stake economics. Nothing revolutionary there. What’s unusual is how Plasma validators are behaving given those incentives.

The economics don’t obviously favor them yet. Plasma subsidizes zero-fee USDT transfers through a paymaster system, meaning the protocol’s flagship use case produces no direct validator revenue. Validators are securing a network that deliberately gives away its most valuable service for free. They’re betting that paid transactions alongside subsidized USDT volume will eventually scale enough to offset inflation and operating costs. If that doesn’t happen, Plasma validators are running infrastructure that bleeds value while delivering its core product at a loss.

Maybe that’s just optimism around future XPL appreciation. But when you operate validator infrastructure, optimism alone doesn’t pay for bandwidth, hardware, monitoring, and uptime guarantees. Running Plasma nodes comes with real recurring costs. You don’t make those commitments unless you believe transaction volume will eventually justify the spend, or you’re making a pure price bet that could evaporate quickly.

Plasma processed $1.58 billion in active Aave borrowing as of November. That’s real leverage, not idle liquidity. WETH utilization reached 84.9%, USDT hit 84.1%. Those numbers suggest genuine capital demand rather than short-term incentive chasing. This was only two months after Plasma mainnet launched. Not Ethereum scale, obviously, but enough to demonstrate that Plasma can support meaningful DeFi activity secured by independent validators.

Daily trading volume around 9.04M USDT doesn’t tell you much about Plasma payment adoption. Trading volume rarely reflects actual utility. The real questions are harder to answer. How many applications are processing stablecoin payments on Plasma consistently? Is the Plasma Card gaining traction beyond internal testing? Are validator revenues growing in a way that can sustain infrastructure long-term? The team doesn’t publish granular payment metrics, so outsiders are left inferring adoption indirectly.

The circulating supply sits at roughly 1.8 billion XPL out of a 10 billion maximum. About 18% is live, with the rest locked under vesting schedules. That’s typical for a network this early. As unlocks accelerate, Plasma will face selling pressure unless real network demand scales fast enough to absorb it. The bet Plasma validators are making is that stablecoin transaction volume grows faster than token dilution erodes value.

What makes that bet interesting is commitment asymmetry. Validators aren’t passive XPL holders. They’re running infrastructure that can’t be unwound instantly if price collapses. If $XPL drops to $0.05, spot holders can exit in seconds. Validators can’t. Hardware, contracts, and operational complexity force longer time horizons. That creates a fundamentally different incentive structure inside Plasma compared to pure speculation.

You can see that long-term thinking in how Plasma launched. Aave deployed within 48 hours. Ethena launched USDe and sUSDe with roughly $1 billion in liquidity capacity. These weren’t casual integrations. Serious capital coordinated around Plasma before mainnet went live. That kind of preparation doesn’t happen unless participants expect the network to survive beyond initial hype cycles.

Staking for regular users goes live in Q1 2026, allowing delegation of XPL to validators. After that, reward distribution will depend on validator performance and delegated stake. Plasma validators will compete on uptime and commission rates, improving service quality while adding operational complexity. Running a Plasma validator isn’t just technical; it becomes partially a business development exercise.

The fee mechanism allows transactions to be paid in XPL or whitelisted assets like USDT or BTC. Maintaining predictable fiat-denominated costs while XPL fluctuates creates tension. When XPL appreciates, fees get cheaper in dollar terms. When it drops, costs rise, even though Plasma aims for stability. That volatility remains a hurdle for merchant adoption.

This is where centralized processors still dominate. Stripe offers predictable pricing mature infrastructure and immediate support. Plasma validators are competing against that with a more complex, less mature system. They’re betting that censorship resistance, permissionless access, and independence from intermediaries matter enough for certain users to accept trade-offs.

Most merchants probably won’t care. Convenience wins. But for cross-border payments, remittances, or environments where accounts get frozen arbitrarily, Plasma’s zero-fee USDT transfers with sub-second finality become genuinely compelling. That niche might be enough.

The $2 billion in day-one liquidity suggests some institutions believe that bet is worth making. Whether Plasma succeeds depends entirely on real payment adoption, not token charts. For now, validators keep committing capital and Plasma keeps processing transactions without collapsing. That alone already puts it ahead of most payment chains that never made it past the narrative stage.