Based on Cicada Market Making Research. All figures sourced from publicly available data including on-chain analytics, platform documentation, academic research, and industry reporting. Featuring insights from Outcome.

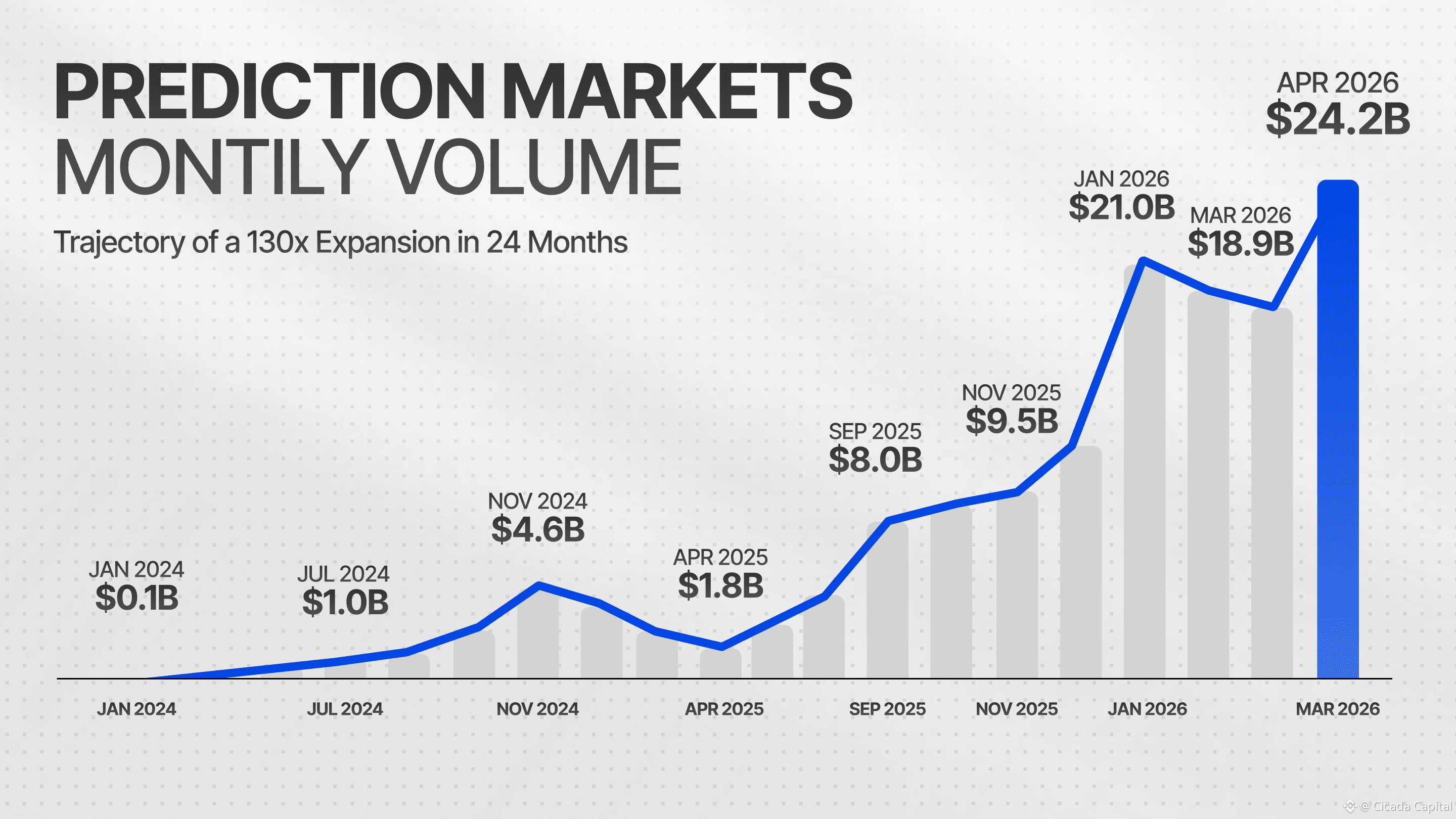

In January 2024, total monthly volume across all prediction market platforms sat at roughly $100M. By April 2026, that number reached $24.2B. A 130x expansion in 24 months, with the trajectory showing no signs of flattening. Most people still think of prediction markets as a crypto-native experiment, and that framing is about two years out of date.

Kalshi won its legal battle against the CFTC in May 2025, establishing binary event contracts as legally tradeable instruments under US commodity law.

CME Group entered the category. DraftKings and FanDuel brought their combined 12M+ user base along. Robinhood integrated Kalshi directly into its brokerage interface and generated $300M ARR faster than any product in the company’s history. ICE invested $2B into Polymarket at a $15B valuation, and Kalshi itself reached a $22B valuation in March 2026.

A forming asset class with regulated infrastructure, institutional capital, and mainstream distribution all arriving simultaneously. That convergence is rare and the window it creates for early operators is finite.

Who Actually Makes Money Here

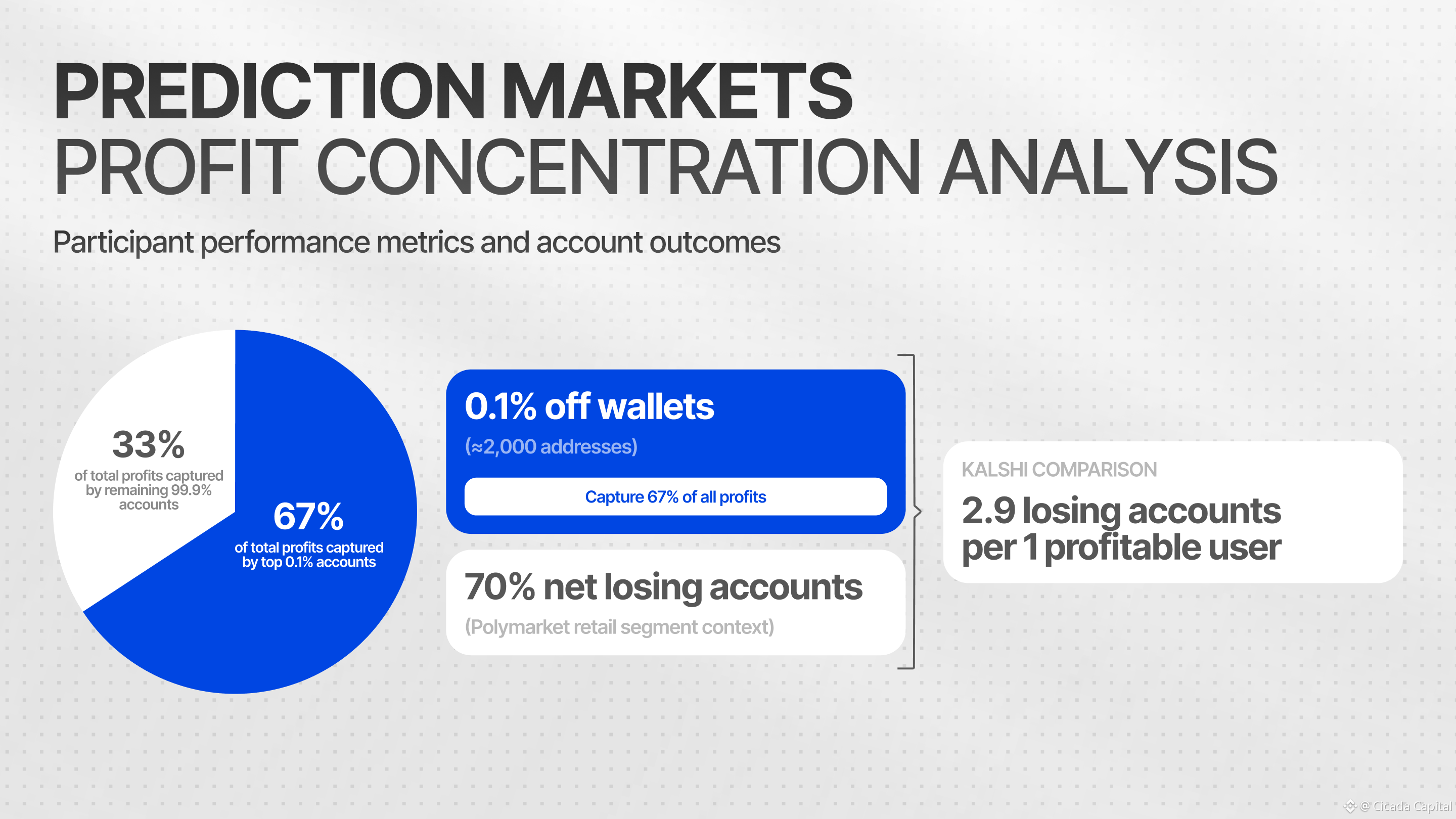

The profit structure of prediction markets is the most important fact about them for anyone considering market-making as a strategy.

Across Polymarket's 1.6M registered accounts, 0.1% of wallets capture 67% of all profits. That top cohort, roughly 2,000 addresses, has accumulated approximately $500M since late 2022. On Kalshi, 2.9 losing accounts exist for every profitable one.

Retail participants lose systematically and persistently. They trade on opinion, overweight recent events, and have no access to the pricing models that determine fair value on these instruments.

The professional layer is extraordinarily thin. TRM Labs data shows that accounts with more than 10,000 fills generate 35.2% of total volume. On most Polymarket markets, there are literally one or two active bots providing two-sided liquidity.

The counterparty pool is deep, the competition is minimal, and the behavioral patterns of retail flow are predictable enough to build a durable edge against.

The information asymmetry is large, the professional population is small, and the platforms are actively paying operators to provide liquidity through rebate programs distributing approximately $5M per month. For a market-maker, the structural setup here is about as clean as it gets.

The Platform Landscape

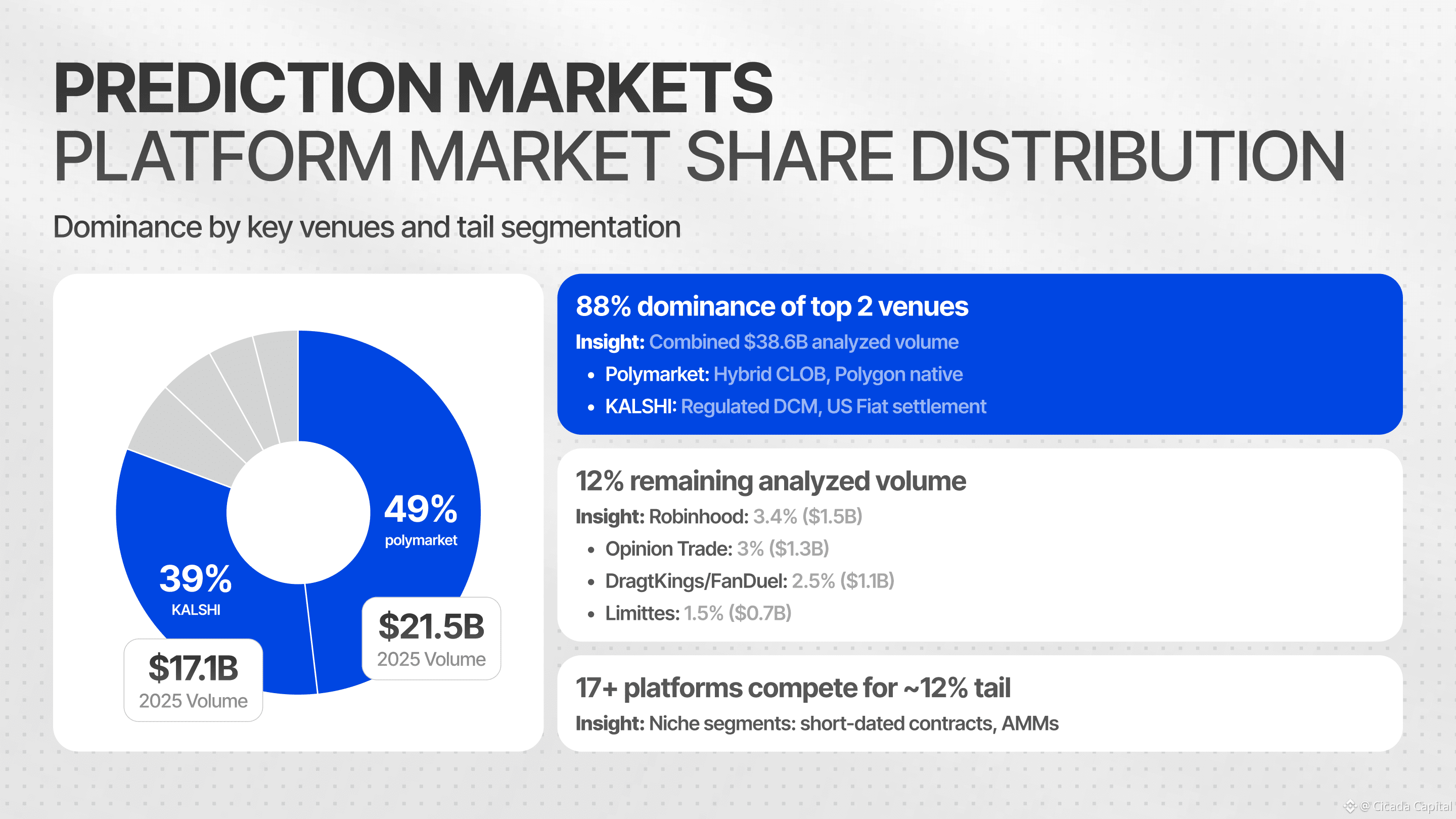

Polymarket and Kalshi together account for 97.5% of all volume. The remaining 17+ platforms share approximately $1.25B annually.That concentration means any serious operation must be native to both dominant venues, while the long tail represents early-entry opportunities where designated market-maker arrangements, equity stakes, and fee-share structures are still negotiable.

Polymarket operates as a decentralized CLOB on Polygon with zero maker fees and a rewards program calibrated to reward tight two-sided quoting.

Kalshi is the regulated counterpart, a CFTC-licensed Designated Contract Market settling in USD with 4% APY on idle balances and 40% of volume already coming from institutional participants.

Three emerging platforms carry strategic weight beyond their current size:

Opinion launched on BNB Chain in October 2025 and generated $3.1B in cumulative volume within three weeks, briefly surpassing both dominant platforms on weekly flow.

Limitless on Base runs 30-minute crypto price contracts, a segment that sits closer to short-dated options than traditional prediction markets.

Hyperliquid HIP-4, announced in February 2026, brings outcome tokens to Hyperliquid’s L1 unified with the same account infrastructure handling spot and perpetual trading. HIP-3, permissionless perpetuals launched October 2025, now generates 35%+ of Hyperliquid’s total volume, and that precedent defines what early market-maker positioning on HIP-4 at the testnet stage could be worth.

Each of these platforms represents a different entry dynamic, and collectively they suggest that the prediction market landscape is still early enough in its maturation that first-mover advantages across multiple venues remain genuinely available.

The Monetization Stack

The near-term cash flow engine is core market-making on Polymarket’s CLOB. Two-sided quoting across 30–50 markets, calibrated to the rewards formula and optimized for spread capture, generates approximately 50% APR on $500K of deployed capital in conservative modeling. Capital requirement to enter is $50K, and breakeven arrives in 4–6 weeks.

Cross-platform arbitrage between Polymarket, Kalshi, and Opinion Trade layers directly on top of that foundation. IMDEA Networks documented over $40M in extractable arbitrage profit from Polymarket alone across a single 12-month period, analyzing 86M trades.

The opportunity takes three principal forms:

Intra-market arbitrage where YES plus NO prices sum below $1.00 after fees, a structurally risk-free trade

Cross-platform pricing gaps on identical events quoted differently across venues

Stale-price windows of 30–120 seconds following macro data releases, when Polymarket typically reprices before Kalshi

The crypto-edge layer is where existing options and perpetuals expertise transfers most directly. Polymarket’s 5-minute and 15-minute crypto price markets, launched March 2026, price at systematic discounts to the implied probabilities derivable from Deribit IV.

An operator continuously computing fair value from risk-neutral density and quoting against that model creates an edge that retail participants fundamentally cannot replicate, with directional exposure hedging cleanly through offsetting spot or perpetual positions.

As capital accumulates, the strategy stack expands upward. An OTC desk serving institutional clients who need 100K+ tickets generates 80–200 bps per trade on $5M of working capital.

Delta-neutral holding positions earn 4% APY from both Polymarket and Kalshi simultaneously on long-dated markets. Designated market-maker arrangements on emerging platforms, particularly Hyperliquid HIP-4 pre-mainnet, layer equity upside on top of operating revenue.

Where the Real Margin Lives

The highest-multiple opportunity in this landscape sits at the intersection of prediction market liquidity and institutional capital demand. Family offices, macro hedge funds, and private banks want exposure to political and macroeconomic event outcomes.

The liquidity to express that exposure now exists on regulated platforms at scale. What these institutions lack is an access format compatible with their operating model, meaning USD wire settlement, standard subscription documentation, independent NAV administration, and legal structure that compliance teams can approve.

The gap is operational and legal, and an operator who closes it captures 200–500 bps of structural margin on AUM, with marginal costs approaching zero once the infrastructure is running.

The product architecture runs through an offshore SPV that issues notes to investors, with the portfolio manager deploying capital through qualified custody into Polymarket and Kalshi positions, optionally hedged through Deribit options or treasury bills for principal protection structures. Four products are immediately buildable within this framework:

US Macro Bundle: quarterly rolling basket of 30–40 positions across FOMC decisions, CPI prints, NFP releases, and GDP advances, targeting $10M — $30M in AUM with fee structures generating ~$800K/year at $20M

Election Year Hedge: 92% of NAV in T-bills guaranteeing principal return, 8% in delta-neutral position across US midterm and European election outcomes, targeting $20M — $50M in AUM with ~$1.5M — $2M/year in fees at $30M

Crypto Catalyst Notes: 100% active exposure across BTC ETF flows, ETH staking yields, halving metrics, and regulatory decisions with Deribit overlay for delta hedging, targeting $5M — $15M in AUM

Stable Politics Yield: fully deployed across 200+ low-volatility markets with no single position above 1% of NAV, targeting 8–12% net APR to the investor as a stablecoin treasury alternative

Setup cost for the full product infrastructure runs $150K to $250K one-time, with annual operating costs of $300K — . The economics become compelling above $30M in AUM, which is the threshold at which the product layer should activate. Below that, market-making and capital strategies provide the cash flow and track record needed to attract institutional allocators.

The Competitive Clock

The firms that will eventually dominate prediction markets at institutional scale, Susquehanna, DRW, Jump, are watching and some are already building. What they have not yet done is systematically occupy the full range of market-making opportunities across platforms, categories, and deal structures that currently exist. That gap defines the entry window.

The calendar concentrates the stakes considerably. The POLY token launch drives a surge in retail participation and new market creation velocity. US midterm primaries beginning Q2 2026 will grow political event volume by 3x — 5x.

Hyperliquid HIP-4 mainnet arrival in Q3 2026 opens a new venue at the ground floor. The November 2026 midterm elections are the peak liquidity event of the year, rewarding operators who arrive with calibrated models and pre-positioned capital across the key markets.

Every month of delay is a month of compounding disadvantage in a market where reward structures favor incumbents, where track record drives institutional access, and where the professional layer is still thin enough that a well-resourced operator can establish genuine market presence before the window closes.

What the Numbers Actually Look Like

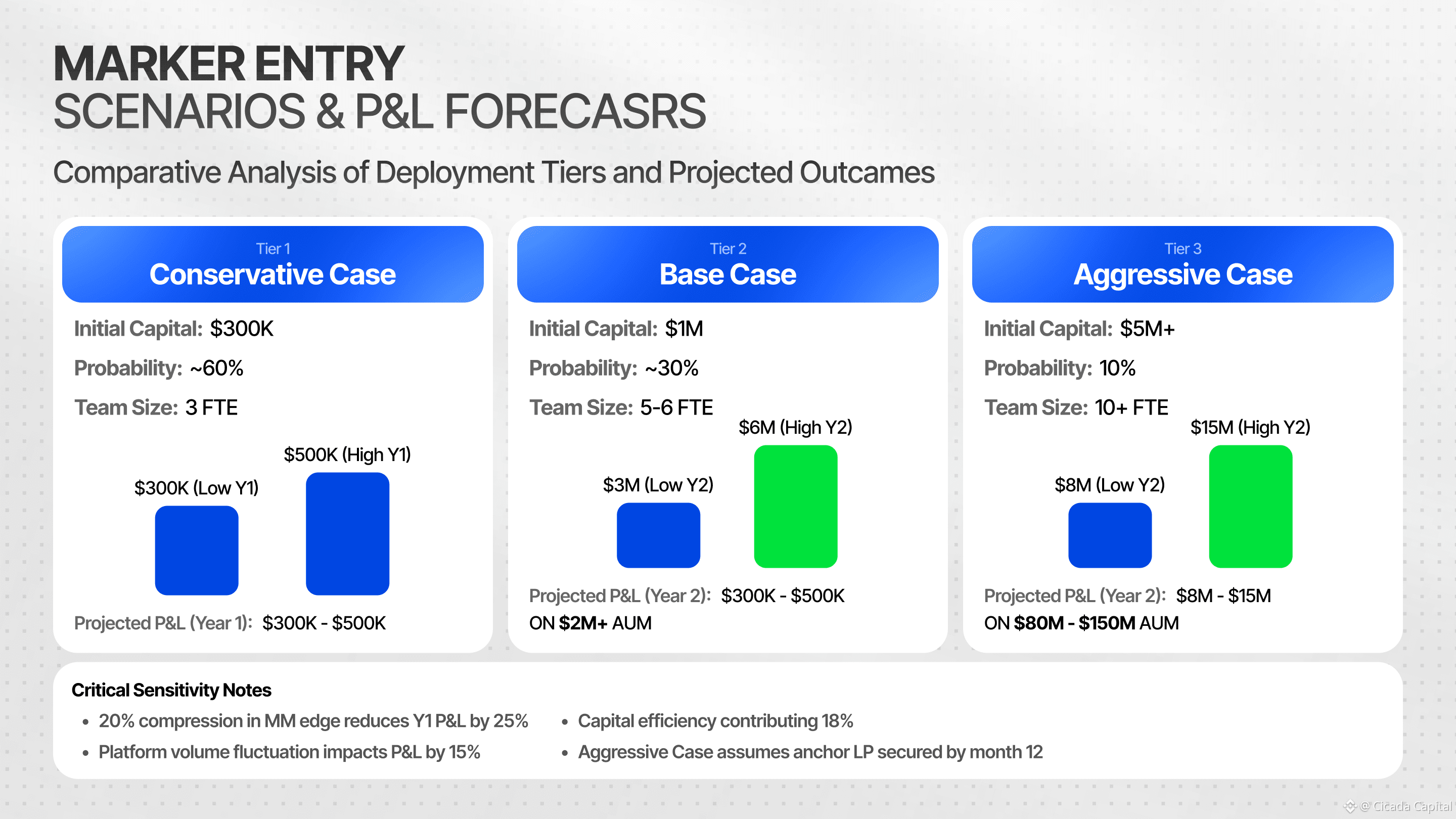

Three scenarios frame the range of realistic outcomes for a production-tier entry. The conservative case, which Cicada Market Making assigns approximately 60% probability, deploys $300K of initial capital with a three-person team, reaches breakeven at month 5, and generates $300K — $500K in Year 1 P&L representing 100% — 170% return on deployed capital.

The base case, at 30% probability, scales to $200K — $350K per month by months 12–18 as the first structured product launches, with Year 2 P&L reaching $3M — $6M on 20M+ in AUM. The aggressive case, at 10% probability with $5M+ of initial capital and an anchor LP secured by month 12, targets $8M — $15M in Year 2 P&L on $80M — $150M in AUM.

The most sensitive variable across all scenarios is MM edge in basis points, where a 20% compression translates directly to 25% reduction in Year 1 P&L. Platform volume and Polymarket’s reward rate each carry 15% — 20% sensitivity, while capital deployment efficiency contributes another 18%.

On the risk side, the four areas requiring active management are adverse selection from informed traders on political markets, regulatory action against either dominant platform, Polymarket reward structure changes post token launch, and TradFi competition arrival compressing margins in the most accessible strategies.

Each has a defined mitigation path, and collectively they reinforce the same conclusion: the earlier the entry, the more favorable the risk profile.

Conversation with Outcome Labs

We sat down with Jonathan, Chief BDO at Outcome Labs, to get an operator’s view on what actually differentiates on-chain prediction markets from traditional bookmakers, and where the next wave of volume is likely to come from.

Q: What does an on-chain prediction market give a trader that a traditional bookmaker fundamentally can’t?

It’s a matter of who the counterparty is. A bookmaker would set odds to protect their margin, and the model depends on the house coming out ahead. In other words, they profit when you lose.

Whereas an on-chain market would be more efficient, more visible, and fairer infrastructure precisely because you’re not competing with the house. You trade at a market-set price vs. other participants, with positions and payouts verifiable on-chain.

Because more of the process is automated on-chain, the cost of executing that trade is more capital-efficient. Depending on the design, on-chain prediction market resolution mechanisms can be more closely related to the actual outcomes if you have multiple parties composing a resolution and involve verified oracles, in comparison to a centralized system which may be predisposed to manipulation or inaccuracies.

Q: Which category isn’t being priced yet but should be, and what’s the infrastructure gap holding it back?

At the moment, a large proportion of prediction market volume is sports, given the general population’s interest in it and the analogs they share with sportsbooks, making them easier to understand intuitively for a retail audience. In the future, as liquidity increases, you should see prediction markets become a primitive that is relevant for institutions. For example, you can expect economics and politics to grow as discretionary macro hedge funds arrive in the coming years. They would just require trading infrastructure such as prime brokers to enable them to trade safely. Another large unlock would be leveraging prediction markets for real-world risk, such as insurance-style, parametric markets around weather and natural disasters, the kind of Property & Casualty (P&C) exposure insurers typically want to hedge with reinsurers.

Right now, what’s preventing institutions from entering, as you mentioned, is infrastructure. Hyperliquid is unique in that its back-end will be white-labeled across many builder-code front-ends. Wallets, exchanges, trading terminals, and prime brokers that incorporate Hyperliquid should readily have access to HIP-4 already within a cross-margin setup. Being able to access a thick order book with minimal fees will enable increased adoption of that order book across multiple distribution channels. With the increased adoption of Hyperliquid builder codes, that should only be a matter of time.

Q: With most platforms looking similar on the surface, where’s the real moat: liquidity, resolution infrastructure, or distribution?

All of those matter, but in a world of multiple prediction markets, having the order book readily available through multiple distribution channels increases the chance of network effects and higher usage. Liquidity for contracts will ensure flow continues to come, which acts as a flywheel. The resolution infrastructure is important for the whole system to feel fair and for users to feel respected — that funnels into brand transparency.

Not all prediction markets will be built on Hyperliquid, which is some of the most efficient trading infrastructure with minimal cost bloat (i.e., a 13-person team) and is able to benefit from the value of the HYPE community, for which there are sufficient revenues going back towards buyback pressure. HYPE is likely one of the only success stories in crypto that was able to successfully engineer tokenomics in a way that encourages organic marketing. Hyperliquid is already on the path towards cementing its position within on-chain trading, including spot and derivatives, which many perps platforms have tried and failed to recreate during the past meta. Hyperliquid has already reached a degree of escape velocity with its DAT listings, coverage by Wall Street, and increased presence, which leads to widespread adoption through more seamless conversations (e.g., with builder codes rather than manual business development deals).

You’ve seen prediction markets such as Kalshi and Polymarket both announce attempts to enter the perps space. The market already understands how difficult it is to enter perps and recreate the same flywheel Hyperliquid created, given its lack of venture funding (and the resulting lack of typical token-dumping pressure), and the benefits set up for market makers (e.g., cancel priority, speed bumps), among others. By leveraging existing infrastructure that already has market makers plugged in, the ability to cross-margin positions, and the increasingly wide distribution scope that builder codes provide, HIP-4 should have a more intuitive and natural path towards building adoption.

Taken together, these answers reinforce the report’s core thesis: liquidity, resolution, and distribution aren’t separate moats, they compound on each other, and platforms stacking all three early are the ones positioned to absorb the next leg of volume.

Maxim Moris’s Vision, CEO of Cicada

We also asked Maxim Moris, Cicada’s CEO, for a more candid, on-the-ground read on platform dynamics and what’s actually likely to move volume through the rest of 2026.

Q: Which emerging platform has a realistic shot at capturing at least 10% of the market by the end of 2026?

Kalshi’s success in the US makes sense in context: the country never had the kind of established betting industry Europeans grew up with, so Kalshi simply walked into an open niche. A lot of the platforms trying to copy that playbook elsewhere miss this entirely — in most other countries, that niche has been occupied by traditional bookmakers for decades.

You see it directly in the even around an event as massive as the World Cup, many Polymarket and Kalshi clones still struggle to attract real liquidity, because users are already anchored to other platforms. Polymarket’s own growth, meanwhile, has been driven in no small part by informed and insider-adjacent flow, which is clearly bad for market integrity, but doesn’t change the underlying demand: people like to bet, the population prone to it isn’t shrinking, and on-chain prediction markets fit naturally into crypto’s broader trajectory.

Over time this market will accumulate more rules and more regulation, and that’s exactly the environment new entrants need to find real footing.

Q: Are the US midterms the only major volume driver this year, or are there hidden catalysts?

The midterms are the obvious, scheduled catalyst, but the less obvious one is structural rather than calendar-based: as long as informed flow and insider-adjacent trading keep pulling sophisticated capital toward these platforms, and retail gambling demand keeps growing rather than shrinking, volume gets pulled forward independent of any single event on the calendar. The midterms will spike attention, but the underlying growth curve is being driven by participation dynamics that don’t reset after election day.

Q: Will short-term 30-minute crypto price contracts become more popular than traditional event markets?

No — they serve a fundamentally different class of trader. Short-dated crypto contracts attract people thinking in options-like, intraday terms, while event markets attract people with a view on a real-world outcome. They’ll grow in parallel rather than one displacing the other.

That mix of structural inefficiency, sticky user habits, and a regulatory framework still being written is, in Maxim’s view, exactly what makes this window worth moving fast on now rather than waiting for the rules to fully settle.

The Thesis

Prediction markets have reached the scale and regulatory legitimacy that makes them a genuine asset class. The current structure, with retail participants losing systematically to a thin professional layer while institutional capital forms but remains largely without proper access infrastructure, describes a market in early transition.

The opportunity for an operator with existing algorithmic trading expertise runs across three time horizons. Near-term cash flow comes from market-making and arbitrage strategies that reach profitability within weeks of deployment.

Medium-term margin expansion comes from OTC operations and cross-platform capital strategies that layer on top of a running infrastructure base. Long-term operating leverage comes from structured products that monetize the institutional access gap with margins that resemble software businesses rather than trading desks.

The infrastructure required to enter is accessible, the market structure is genuinely favorable, and the regulatory environment has cleared. The window is real and it is closing.