When I first came across Newton Protocol, I thought it was mainly another crypto project focused on automated trading.

That was my first impression.

I kept seeing terms connected to it such as financial agents, programmable permissions, secure infrastructure, rollup technology, and an onchain marketplace. The idea sounded interesting, but it also felt too broad. I could not immediately tell what Newton was actually building or which part of the project mattered most.

So I started looking deeper.

I went through its documentation, public repositories, token structure, and more recent project updates. As I read, my understanding slowly changed.

At first, I thought Newton was mainly designed to help automated systems trade, manage portfolios, and perform financial tasks. Later, I realized that its more important purpose is controlling what those systems are allowed to do.

That difference became the main reason I found the project worth studying.

Automation is already common in crypto. Bots can place trades, vaults can move funds between strategies, lending platforms can manage collateral, and smart accounts can carry out transactions without someone manually approving every step.

That can be useful.

It can also be dangerous.

If I give a service permission to use my funds, how do I make sure it stays within the limits I intended?

A normal wallet permission can be too broad. I may want a service to rebalance part of my portfolio, but I do not want it to move everything I own. I may allow it to trade a few selected tokens, but not interact with unfamiliar contracts. I may want it to stop after reaching a daily loss limit or pause when the market becomes unstable.

A private key does not understand any of that.

It only proves that someone or something had permission to sign a transaction. It does not know why the permission was given. It does not understand the boundaries that were supposed to come with it.

Newton is trying to solve this problem by adding programmable rules before a transaction is completed.

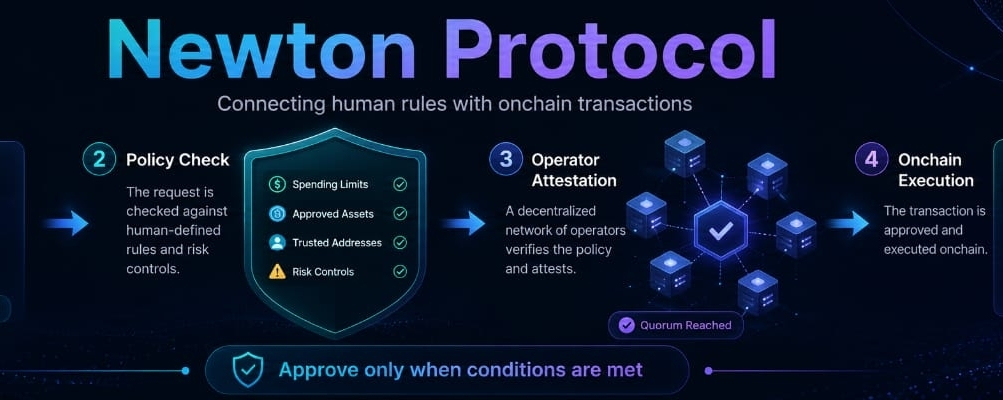

The easiest way I found to understand the project was to think of it as a permission checkpoint.

Before a protected transaction goes through, Newton can examine the proposed action and compare it with a policy. That policy may include spending limits, approved assets, trusted addresses, identity requirements, market conditions, compliance checks, or security warnings.

If the transaction follows the rules, it can be approved.

If it breaks them, it can be rejected before funds move.

This felt much more practical to me than simply calling Newton a platform for automated finance. Automation itself is not the hardest part. The harder problem is making sure an automated system cannot act outside the authority it was given.

I imagined a simple example while trying to understand how Newton might work in practice.

Suppose I manage a treasury wallet and use an automated service for routine payments. I may be comfortable allowing that service to handle regular expenses, but I would still want restrictions.

No single payment should exceed a certain amount.

Daily spending should have a limit.

Only selected tokens should be used.

Payments should go only to approved addresses.

Transactions involving flagged wallets should be rejected.

The service should stop when a security provider reports unusual risk.

The payment system could still do its job, but it would not have unlimited control.

That is the part I found most interesting.

Newton is not only about giving access. It is about giving access under specific conditions.

The process begins with what Newton calls an intent. An intent is a description of what an application wants to do. It may include the sender, receiver, amount, blockchain network, contract address, and function being called.

That request is then checked against a policy.

Some rules can be evaluated using information already included in the transaction. Other rules may depend on outside data, such as sanctions lists, market prices, identity results, proof-of-reserve reports, fraud signals, or security scores.

Newton’s operators evaluate the request and produce a decision.

When the request is approved, the system can create a cryptographic attestation. The receiving smart contract can verify that attestation before completing the action.

This part stood out to me.

The contract does not have to trust a simple message from a private server saying that everything is fine. It can verify that the required authorization process actually took place.

The timing matters too.

Many security tools detect suspicious transactions after they happen. They may send an alert, flag an address, or produce a report. That information can be useful, but it does not prevent the loss once the transaction has already been confirmed.

Newton is designed to check the rules before execution.

For me, that is one of the strongest parts of the project.

Prevention is usually more valuable than explanation after the damage is done.

Newton currently uses a policy language called Rego. I had not spent much time with Rego before, but the basic idea was easy to understand.

Instead of writing a long program for every possible situation, developers can describe the conditions that must be true before an action is accepted.

A rule might allow a transfer only when the amount stays below a fixed limit. Another could reject a payment when the receiving address appears on a restricted list. A trading rule could allow activity only for selected assets.

A stricter policy might pause transactions when volatility rises too far.

This approach feels natural for financial controls because companies and organizations already think in terms of conditions.

A business may allow employees to spend up to a certain amount without extra approval. A treasury may allow payments only to approved vendors. A trading desk may set limits on position size, slippage, or daily losses.

Newton is trying to express these kinds of rules in a form that can be checked before an onchain action is completed.

I also like the separation between the application and the policy.

A trading system can focus on choosing and placing trades. The policy can focus on deciding which trades are acceptable.

A payment application can focus on sending funds. The policy can define how much can be sent, where it can go, and what conditions must be met.

This makes the rules easier to inspect and update.

Still, there is an obvious risk.

A policy is only as useful as the person who writes it.

Newton may enforce a rule correctly, but that does not mean the rule itself is sensible. A badly designed policy could block legitimate users or approve something dangerous. A rule that works during normal market conditions may behave badly during an extreme event.

That means developers still carry a lot of responsibility.

Policies need to be tested, reviewed, monitored, and updated over time.

While looking at the developer side, I found simulation to be one of the more useful features. Developers can submit a sample transaction and see whether the policy would approve or reject it without using real funds.

That matters because authorization systems can fail in two directions.

They can be too weak and allow dangerous activity.

They can also be too strict and stop normal users from completing ordinary transactions.

Testing gives developers a chance to catch both problems before real money is involved.

The developer process also made something else clear to me. Newton does not currently look like a simple consumer app. It appears to be infrastructure mainly for developers, protocols, payment providers, treasuries, and organizations.

A regular user may never interact with Newton directly.

Instead, it could operate behind a wallet, a payment service, a trading platform, or a smart contract. The user would mainly notice the result when a transaction is approved, limited, or blocked.

Newton uses an operator network connected to EigenLayer. These operators evaluate policies and help produce the attestations used by smart contracts.

The purpose is to reduce dependence on one private authorization server.

If a single company controlled every approval, users would need to trust that company to remain secure, available, and honest. A compromised server could approve harmful transactions, reject legitimate ones, or stop working completely.

A network of operators can reduce that risk.

But I would not assume the system is strongly decentralized just because several operators are involved.

I would still want to know how many operators are active, who controls them, how independent they are, and what happens when they disagree. I would also want to understand how new operators join and whether participation becomes more open over time.

Newton’s operator structure appears to remain permissioned at this stage.

That may be reasonable while the network is developing, but it also means the project should be clear about the level of decentralization it currently provides.

Another important part of Newton is its use of outside data.

Some policies can work entirely with onchain information. Others need information from external sources.

A payment policy may need a current sanctions result. A lending policy may need market prices. A business may want to check identity status. A stablecoin issuer may need information about jurisdiction or compliance.

Newton allows policies to use data oracles for these checks.

This makes the system more flexible, but it also creates another source of risk.

Operators may correctly agree on a result while the original data itself is wrong or outdated.

Cryptography can prove that a decision was produced and signed. It cannot guarantee that an outside provider supplied accurate information.

This is not only a Newton problem. It affects almost every blockchain system that depends on real-world data.

A strong implementation may need several providers, clear expiration times, fallback rules, and careful handling when information becomes unavailable.

The correct response may also depend on the type of transaction.

A small payment might be delayed and retried.

A large treasury transfer may need to be rejected until reliable data becomes available.

These decisions should be built into the policy rather than left to chance.

The more I researched Newton, the more I noticed that its public identity has changed over time.

Earlier descriptions focused heavily on automated agents, secure rollup technology, programmable accounts, model registration, trading tools, and a global marketplace.

The project seemed to be building a broad environment where developers could offer automated financial services and users could give those services controlled access to their funds.

The current direction feels narrower.

It also feels more focused.

Newton now presents itself mainly as an authorization layer for onchain transactions. Its newer material gives more attention to policies, operators, attestations, compliance checks, payment controls, and runtime restrictions.

I do not see the older and newer versions as completely separate.

Automated trading agents still need permissions.

Financial services still need spending limits.

A marketplace of automated tools would still need a way to stop those tools from doing more than users intended.

The authorization layer could support the earlier vision.

However, some parts of the original plan are less visible now. The model marketplace and wider agent economy do not appear as central to the current developer experience as the policy system.

I think narrowing the focus may be a sensible move.

Building agents, trading systems, a marketplace, a secure rollup, token incentives, and an authorization layer all at once would be extremely difficult.

The challenge is communication.

Someone researching Newton may still find older material describing it mainly as an automated trading or model marketplace project. Newer documentation may present something different.

The team needs to explain which parts are active, which have changed, and which remain longer-term ideas.

Automated trading still offers a useful example of how Newton could be used.

Suppose I allow a service to rebalance part of my portfolio.

I might let it trade only selected assets. I may limit how much can be placed in one position. I may reject trades with high slippage. I may block interactions with contracts that have not been approved.

I may also require the service to stop when daily losses reach a fixed amount.

The trading service would still choose the trades.

Newton would define the limits around them.

That distinction matters.

Newton is not necessarily deciding what financial action should be taken. It is checking whether the proposed action stays within the rules.

Payments may be an even stronger use case.

A payment company may need transfer limits, fraud checks, sanctions screening, merchant restrictions, or regional controls. These checks are often managed through private systems that users cannot inspect.

Newton could allow some of those rules to be written as policies and connected directly to a smart contract.

A business might permit small supplier payments automatically while requiring stronger approval for large transfers.

A payment service could reject transactions involving restricted addresses.

A stablecoin issuer could apply selected checks before a transfer, mint, or redemption.

This does not remove the legal or operational complexity of financial compliance. It simply creates a clearer way to connect those rules with onchain activity.

Treasury management is another area where I can see practical value.

Many crypto organizations use multisignature wallets. Multisigs improve security by requiring several approvals, but they can also slow down routine activity.

A policy system could allow small, regular payments within an approved budget while requiring extra approval for larger transfers.

It could block payments to unfamiliar addresses.

It could limit certain actions to specific tokens and contracts.

This could give organizations more flexibility without giving one person or automated service full control over treasury funds.

The same idea could apply to employees, contributors, and service providers.

A contributor may be allowed to pay approved vendors but not move reserves. A portfolio manager may be allowed to rebalance assets but not withdraw them. A service may be permitted to interact with one contract while being blocked from everything else.

These kinds of limited permissions already exist in traditional financial systems.

Newton is trying to bring similar controls to onchain accounts.

Lending platforms and liquidity protocols could also use the system as a safety layer.

A lending protocol may want to pause certain actions when an oracle price moves too far from other market prices. A liquidity pool could reject operations when reserves fall below a safe level. A protocol could block actions that would create unhealthy collateral conditions.

These rules act like automatic circuit breakers.

They may not be needed during calm periods, but they can become important when markets move suddenly.

The difficulty is setting them correctly.

A rule that activates too quickly could freeze a healthy system.

A rule that reacts too slowly may fail to prevent damage.

Again, Newton can enforce the decision, but the people designing the policy still need to choose the right conditions.

The NEWT token is another part of the project I examined carefully.

NEWT launched with a maximum supply of one billion tokens. Its planned uses included staking, network security, fees, governance, and payments connected with the earlier marketplace idea.

Staking still makes sense within the current architecture. Operators evaluating policies and producing attestations need incentives and consequences.

Governance may also become more important over time, especially if the community gains greater influence over upgrades, operator rules, treasury decisions, and network settings.

Some of the other token uses are less clear today.

The earlier marketplace was expected to use NEWT for registration and royalty payments. Since that marketplace is not currently the most visible part of the product, I would want updated evidence before treating that utility as active.

I also paid attention to token vesting.

Only part of the total supply was circulating at launch. Other allocations were set aside for contributors, backers, ecosystem funds, the foundation, network rewards, and related purposes.

Those tokens are released over time.

That means circulating supply can continue to rise.

Anyone studying NEWT should look beyond its current price. Token releases, treasury movements, network demand, staking participation, and actual protocol usage may all matter.

I also noticed that public platforms do not always show the same circulating supply. Different services may use different definitions for tokens that are unlocked, vested, circulating, held by treasuries, or actively traded.

Because of that, I would compare several sources instead of trusting one number.

More importantly, I would keep the token separate from the underlying technology.

Newton could build useful infrastructure while the token performs poorly.

The token could also attract market attention before the protocol gains real adoption.

Those stories are connected, but they are not identical.

The strongest part of Newton, from my point of view, is its focus on stopping harmful actions before execution.

Crypto security often depends too much on users making perfect decisions. Once a transaction is signed and confirmed, there may be no realistic way to reverse it.

Newton adds another check between permission and execution.

A transaction may be technically valid but still be rejected because it breaks a spending limit, uses an unapproved contract, fails a compliance rule, or crosses a risk threshold.

I also like the idea of making policies visible and testable.

When rules exist only inside a private service, users may not know how decisions are made. A written policy can be inspected, tested, updated, and audited.

The flexibility is useful too.

The same structure could support treasury controls, stablecoin rules, trading restrictions, payment limits, identity requirements, and lending safeguards.

At the same time, I would not ignore the problems.

The system is technically complex. Developers need to understand smart contracts, policy design, operators, attestations, outside data, and failure handling.

A weak integration could create the appearance of security without providing much real protection.

The operator network still needs to show broader independence. External data providers remain possible points of failure. Policies can contain mistakes or become outdated.

Authorization checks must also remain fast enough that they do not make applications frustrating to use.

The project’s changing identity is another challenge.

Newton needs to explain its current focus clearly so people are not left comparing an older marketplace vision with a newer authorization product.

Adoption will be the final test.

Infrastructure becomes valuable when real applications use it. Documentation and technical design are useful, but Newton will need active operators, reliable policies, developer integrations, and measurable transaction activity.

I began exploring Newton because I expected to find a project mainly focused on automated trading and financial agents.

I ended up seeing it differently.

I now think of Newton as a system for limiting the authority of applications, wallets, and automated services.

That may sound less dramatic than a worldwide marketplace of financial agents, but it addresses a more immediate problem.

As software gains more control over digital a