When I saw that @NewtonProtocol was featured in the Global Blockchain Business Council (GBBC) 101 Real-World Blockchain Use Cases Handbook (2026 Edition), I wasn't interested in the recognition itself.

What interested me was a much bigger question:

What does an institution actually consider a real-world blockchain use case?

After digging into Newton Protocol's architecture and its Mainnet Beta, I came away with a different conclusion than I expected. The next phase of blockchain adoption may not be determined by who executes transactions the fastest, but by who can make those transactions verifiable before they happen.

For years, DeFi has focused on execution. Liquidity became deeper, automation became smarter, and protocols became more capital efficient. But as automation expanded, another challenge emerged.

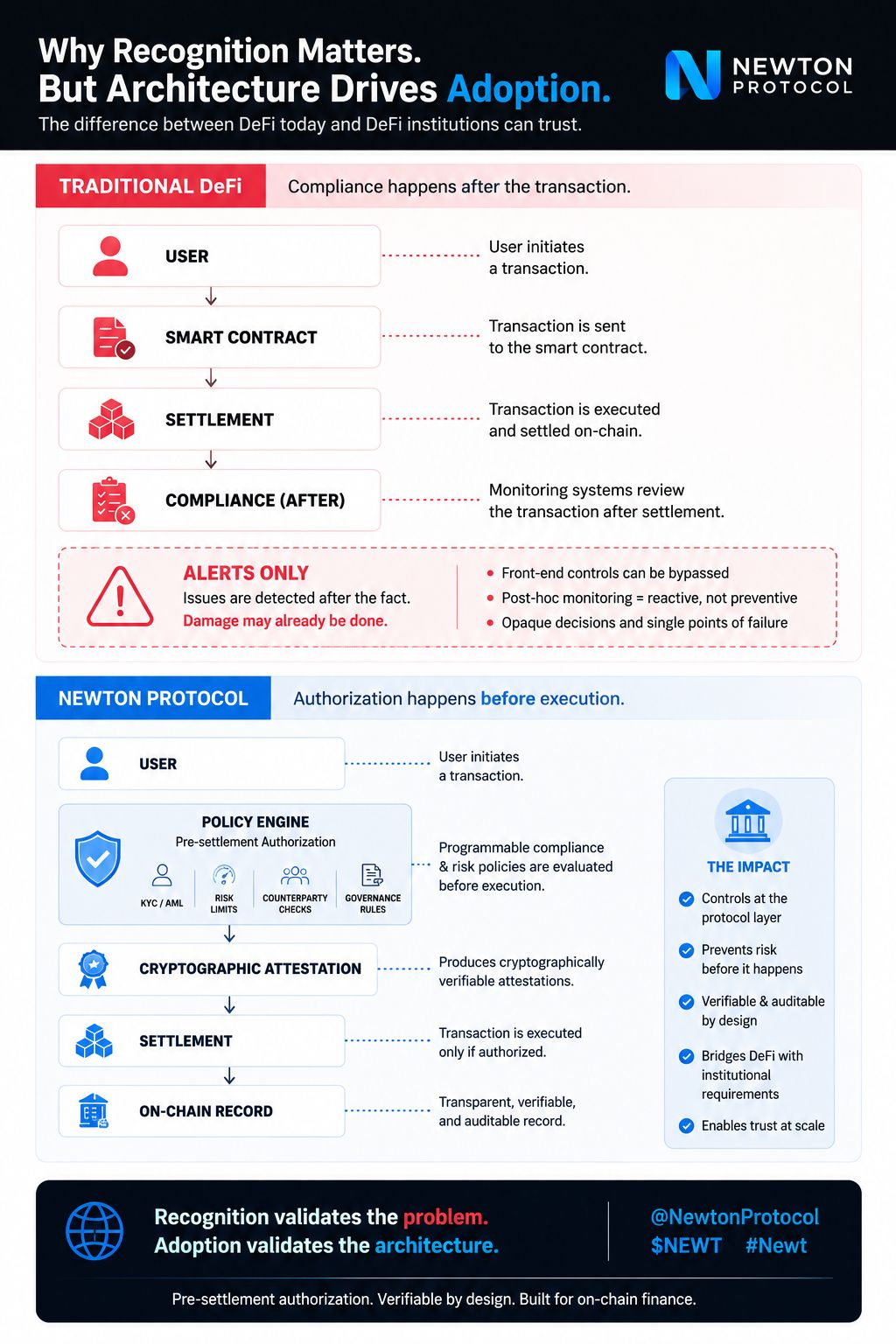

Who verifies that an automated action is actually authorized before value moves?

Most compliance systems today operate either at the application layer or after execution. That creates two obvious weaknesses. Front-end restrictions can often be bypassed by interacting directly with smart contracts, while post-transaction monitoring may identify problems only after assets have already moved.

What stood out to me in the GBBC handbook is that Newton approaches this problem differently.

Instead of treating compliance as something checked after execution, Newton introduces a pre-settlement authorization layer where programmable risk, compliance, and permission policies are evaluated before an on-chain transaction is executed. Every authorization can produce cryptographically verifiable attestations, making it possible to independently verify that predefined policies were satisfied rather than relying solely on trust in an intermediary.

I think that's a much more significant architectural shift than most people realize.

The handbook compares this approach to traditional payment networks, where card transactions are authorized before settlement by checking identity, fraud rules, and spending limits in real time. Newton applies a similar principle to on-chain finance—not to recreate traditional banking, but to bring pre-execution controls into decentralized infrastructure in a transparent and verifiable way.

One thing I think people are overlooking is that institutional adoption has rarely been limited by blockchain performance alone.

Large organizations don't simply ask whether a protocol is decentralized or efficient. They need governance, auditable decision-making, operational accountability, and enforceable policies that fit existing compliance expectations. Without those guarantees, faster transactions don't necessarily reduce institutional risk.

This also highlights an important distinction between recognition and adoption.

Being featured in the GBBC handbook does not automatically prove market adoption.What it does indicate is that the underlying architecture addresses a problem the industry increasingly considers important. Whether this evolves into production-scale infrastructure will depend on developers, financial institutions, and applications choosing to build around verifiable authorization rather than relying on fragmented compliance models.

Of course, every architectural decision introduces trade-offs.

Embedding policy enforcement before execution increases governance complexity and implementation overhead. The challenge is maintaining DeFi's composability while providing the operational controls institutions expect. If authorization becomes too restrictive, innovation slows. If it's too permissive, institutional trust remains difficult to achieve.

The more I looked into Newton, the more I felt the industry is asking a different question than it was a few years ago.

We're no longer asking:

Can blockchain automate finance?

We're beginning to ask:

Can blockchain automate finance while keeping every critical decision transparent, enforceable, and independently verifiable?

My takeaway is that Newton's inclusion in the GBBC 101 Real-World Blockchain Use Cases Handbook is significant not because it celebrates another blockchain project, but because it reflects where institutional thinking appears to be heading.

If pre-settlement authorization becomes a standard layer for on-chain finance, the biggest innovation may not be faster execution—it may be making autonomous execution predictable, accountable, and trustworthy at scale.