The first time I explored onchain lending, something felt fundamentally backwards. Blockchain was supposed to give people greater control over their assets, yet qualifying for better credit often meant exposing more of my financial life than I would ever share with a bank. It solved the trust problem by creating a privacy problem.

Today’s lending models are largely trapped between two flawed approaches. Some rely almost entirely on public wallet activity, treating transaction history as a proxy for creditworthiness. Others fall back on centralized identity providers that collect sensitive documents behind closed APIs. Neither approach is satisfying. One exposes too much, while the other reintroduces the very trust assumptions decentralized finance was meant to reduce.

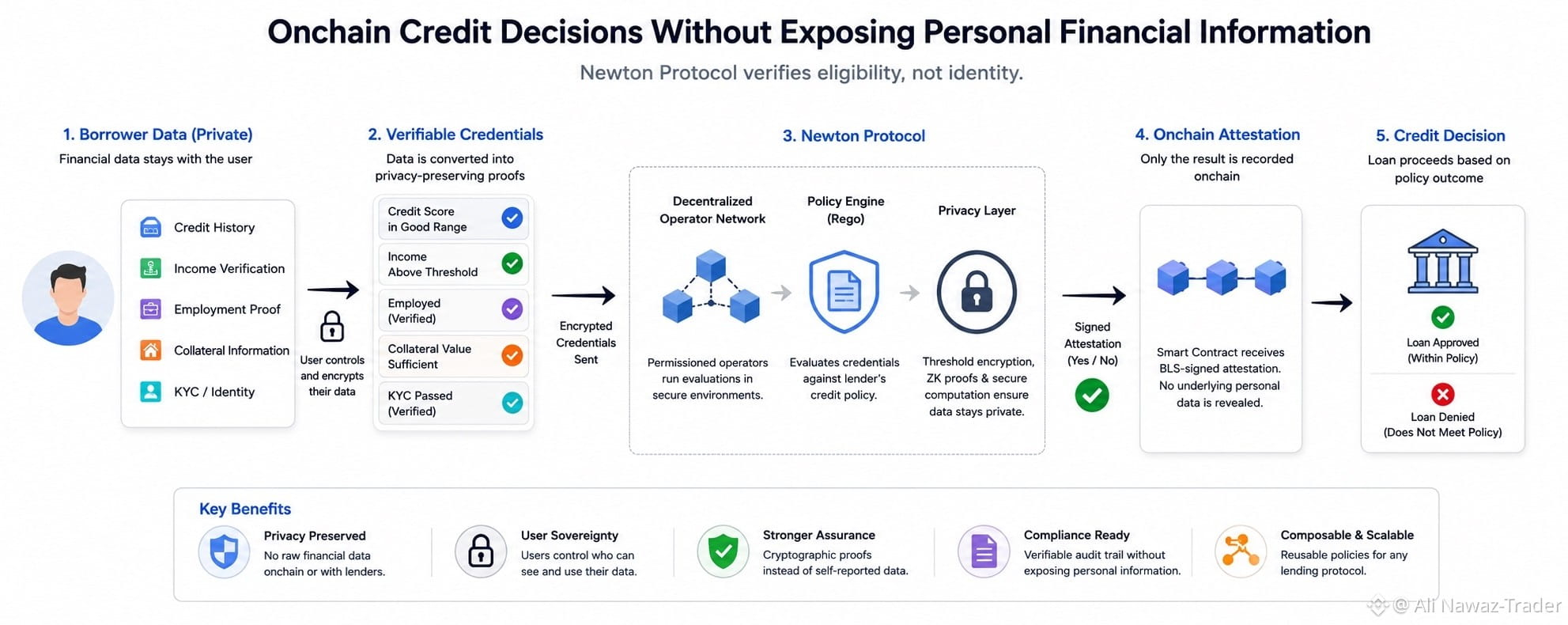

The deeper issue is surprisingly simple. Credit decisions are not about knowing everything about a borrower. They are about verifying a handful of important facts. Does this person meet the required credit threshold? Has their income been verified? Is the collateral sufficient? Are they eligible under the lender’s risk policy? Those questions require proof, not surveillance.

Think about airport security. The officer doesn’t need your entire life story to decide whether you can board a flight. They only need confirmation that you meet specific security requirements. Credit underwriting should work the same way. The industry has quietly treated “verifiable” and “visible” as if they mean the same thing, when they are fundamentally different.

Newton Protocol takes a different architectural approach. Instead of exposing raw financial information, users hold privacy-preserving W3C Verifiable Credentials representing attributes such as verified income, credit history, jurisdiction, or collateral value. These credentials are evaluated against programmable policies written in Rego, while cryptographic techniques such as threshold encryption, zero-knowledge proofs, and decentralized policy evaluation ensure that only the outcome reaches the blockchain. Smart contracts receive a cryptographic attestation confirming whether predefined conditions have been satisfied, not the personal data itself.

This changes more than privacy. It changes trust. Borrowers retain ownership of their financial information, lenders receive stronger cryptographic assurances than self-reported documents, and compliance becomes programmable without turning blockchain into a public database of personal finance. Every authorization can also produce a verifiable compliance receipt, allowing audits without exposing confidential records.

The role of $NEWT fits naturally into this design by supporting the decentralized operator network that performs policy evaluation and secures these attestations through economic incentives. But the larger innovation is not the token. It is the realization that onchain credit decisions do not require public financial exposure to be trustworthy.

As decentralized finance matures, the strongest lending systems may not be the ones that collect the most data. They will be the ones that prove exactly what matters while revealing almost nothing else.

#newt $NEWT #Newt @NewtonProtocol