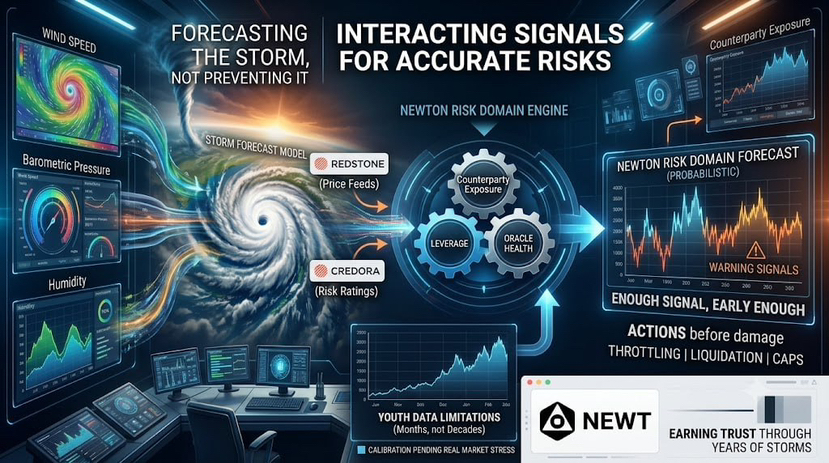

A weather forecaster doesn't measure just temperature, or just wind speed, or just barometric pressure in isolation and call it a forecast. A real forecast combines all three, plus humidity, plus historical storm patterns, because any single measurement in isolation can point in a misleading direction while the combined picture reveals what's actually coming. Newton's risk domain, which evaluates counterparty exposure, leverage, and oracle health as one interacting condition rather than three separate metrics, is built on exactly that logic, and the comparison is more precise than it first appears.

Think about what each individual signal misses on its own. Counterparty exposure alone tells you how concentrated a vault's risk is with a specific set of positions, but it says nothing about whether those positions are dangerously leveraged. Leverage alone tells you how much risk is amplified, but not who's on the other side of it. Oracle health alone tells you whether the price data feeding a decision is trustworthy right now, but it doesn't tell you whether the position that data is informing was already dangerous before the oracle had anything to do with it. A forecaster who only checked wind speed would miss a storm building from a pressure drop nobody was watching. A risk system that only checked leverage would miss a position that's dangerously exposed to a single counterparty regardless of how conservatively it's leveraged.

Where the analogy becomes genuinely useful, rather than just decorative, is in what a forecast actually promises. A forecaster doesn't stop the storm. They can't. What a good forecast does is give you enough combined signal, early enough, that you can move the boat, board the windows, or cancel the flight before the storm arrives instead of after. Newton's risk domain works the same way. It doesn't prevent a counterparty from defaulting or a leverage position from unwinding badly, no risk system can prevent the underlying event. What it does is combine enough signal, evaluated together rather than in isolation, to catch a dangerous condition forming and respond, through a block, a liquidation, or a CAP that throttles the transaction down to a safer size, before the damage actually lands.

This is also where the honest limitation of the analogy shows up. Weather forecasting has had over a century of accumulated data, satellite coverage, and continuously refined models to get combined-signal forecasting as accurate as it currently is, and even the best modern forecasts are still probabilistic, not certain, and still miss storms that form faster than the models can track. Newton's risk domain is working with a comparatively young dataset, a handful of oracle relationships including RedStone and Credora, and mainnet activity that's only just begun accumulating the kind of historical pattern a forecaster relies on to know which combinations of signals actually precede a real storm versus which combinations just look similar on paper.

I think that's the honest state of where Newton's risk domain sits right now: a sound methodology borrowed from a discipline that took generations to mature, applied to a dataset that's had months, not decades, to prove itself. The architecture, evaluating multiple interacting signals instead of trusting one, is the right call, the same way combined-signal forecasting was always going to beat single-metric forecasting once anyone tried building it properly. What isn't yet proven is whether Newton's specific combination of RedStone's price feeds, Credora's risk ratings, and whatever leverage and counterparty data feeds into a given policy has been calibrated against enough real market stress to catch the storms that matter, rather than just the ones that resemble the small dataset it's been trained and tested against so far.

Newton Protocol's risk domain treats counterparty exposure, leverage, and oracle health the way a real weather forecast treats wind, pressure, and humidity, as signals that only mean something combined, not the way a single-number credit score treats risk as one clean, isolated figure. The design is sound. Whether the forecast is accurate enough to trust with real institutional capital is a question only years of storms, not a launch announcement, can actually answer.

I'd watch specifically for how Newton's CAP outcome behaves during the first genuine market dislocation it faces, since that's the moment a forecast either earns trust or loses it. A forecaster who calls every cloudy afternoon a hurricane warning eventually gets ignored, and a risk domain that throttles too conservatively during ordinary volatility risks the same fate, teaching curators to write looser policies around it rather than trusting the signal itself.