Mira been tracking $MIRA holder distribution for the past few days — not the verification technology, the actual ownership structure underneath the token. pulled the wallet data from CMC, mapped it against circulating supply, cross-referenced with the unlock schedule. and honestly? what i found makes the protocol thesis almost irrelevant to the short-term price conversation 😂

let me set the scene first. MIRA is building decentralized AI verification infrastructure. the technology works — atomic claim decomposition, multi-model consensus, on-chain cryptographic proofs logged on Base. Klok copilot runs on it processing billions of tokens daily. KGeN and Phala are integrated. the SDK is live. real usage, real integrations, genuinely useful infrastructure.

none of that changes what the wallet data says.

what bugs me:

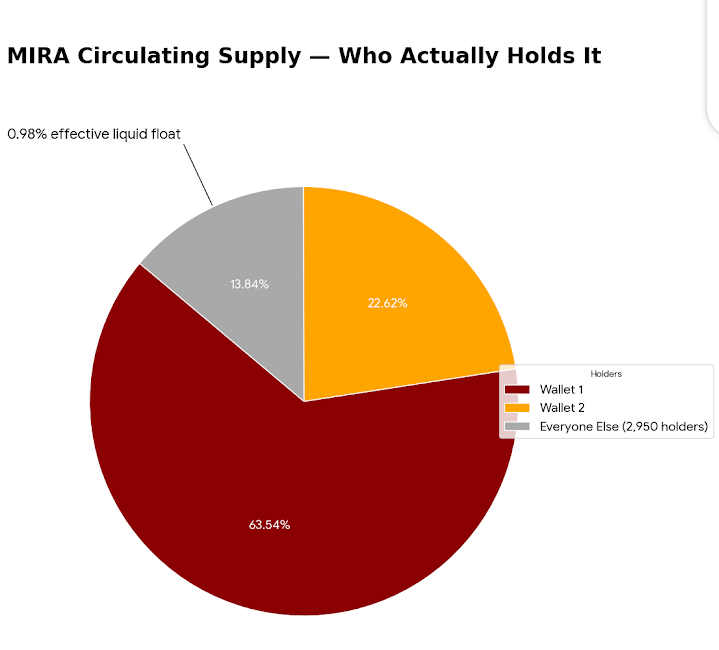

wallet 1 holds 28.08M MIRA. that's $2.50M worth. that's 63.54% of the entire circulating float. wallet 2 holds 10.00M MIRA. $892K worth. 22.62% of float. two wallets. combined: 86.16% of everything currently tradeable sitting in two addresses. top 10 wallets combined: 99.02% of circulating supply. everyone else — all 2,950 remaining holders — shares 0.98% between them.

that's not a distribution problem. that's a float that barely exists.

the tokenomics angle nobody discusses:

circulating supply: 234.07M tokens — 23.41% of total. but the real float is much smaller than that number suggests once you strip out the two dominant wallets. effective tradeable supply for everyone else is roughly 0.98% of 234.07M — about 2.29M tokens. that's the actual liquid market most participants are trading in.

allocation breakdown adds context. insider total sits at roughly 33.83% — team, advisors and contractors at 20%, private sale investors at 13.83%. public sale: 0.10%. essentially nothing. ecosystem incentives hold 25.97% — the largest single allocation — but those tokens vest over time, they aren't in circulation yet.

unlock schedule is what makes concentration dangerous rather than just uncomfortable. today Feb 26: 10.79M tokens unlocked. March 26: 23.6M — more than double today in one month. April: 14.13M. September brings a second spike at 25.82M across five allocations. 38 unlock events remaining in total. 765.92M tokens — 76.59% of supply — still locked.

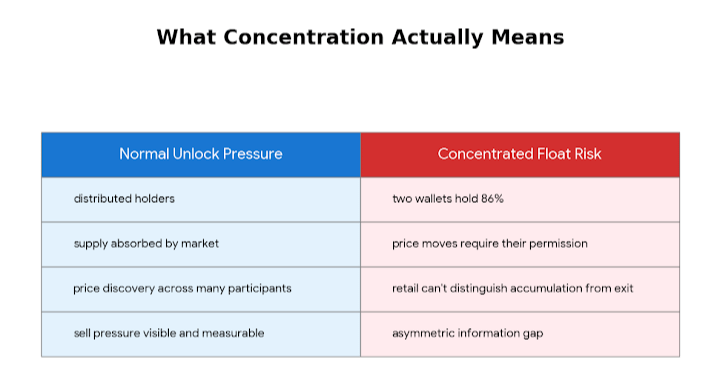

the frame worth running: when 86.16% of float is controlled by two wallets and 76.59% of total supply is still incoming — the price of $MIRA isn't being discovered by a market. it's being managed by a handful of participants who entered earlier and cheaper than anyone buying today. that's a diferent risk category than normal unlock pressure. unlock pressure assumes a distributed holder base absorbing supply. this assumes two wallets deciding when and whether to let price move.

FDV sits at $88.44M against a market cap of $21.65M. FDV/MC ratio: 4.08x. vol/mkt cap 24h: 37.18% — extremely elevated for a token this size. high volume on a thin concentrated float is either accumulation or distribution. from the outside those two look identical until they don't.

my concern though:

the mechanism here isn't that the two dominant wallets will definitely sell. it's that they don't need to sell for concentration to be a problem. price discovery in a market where 86% of float is controlled by two addresses isn't price discovery — it's permission. every rally requires those wallets to not sell. every dip could be either natural correction or quiet exit. retail participants have no way to distinguish between the two in real time. that asymmetry of information is the real risk, not the unlock schedule itself.

what they get right:

the verification architecture is genuinely differentiated. breaking AI outputs into atomic claims rather than verifying whole responses is smarter than it sounds — it means errors get isolated rather than contaminating an entire output. the multi-model consensus requirement adds real security depth. running the same claim through nodes using GPT, Claude, Grok, Llama simultaneously and requiring supermajority agreement across different training datasets is a meaningful attempt at correlated-error reduction.

Base network as the foundation is a credible choice. Coinbase's L2 brings institutional familiarity, lower fees, and existing liquidity infrastructure. for a verification layer targeting enterprise AI use cases and DeFi agents that need reliable outputs, Base is a more defensible home than a newer or less liquid chain.

the Klok integration is real traction. billions of tokens processed daily through a live consumer product means MIRA isn't theoretical infrastructure waiting for adoption — it has a production workload running right now. KGeN and Phala add gaming and secure compute verticals. the SDK being publicly available means any developer can integrate today without waiting for permission.

ecosystem incentives at 25.97% — the single largest allocation, bigger than team, bigger than investors — is the right signal about where the foundation's priorities sit. if those incentives successfully pull in node operators and integrators beyond the current three known partners, the demand loop could become genuinely self-sustaining over time.

what worries me:

the 37.18% vol/mkt cap ratio on a token this concentrated is the number i keep coming back to. total holders: 2,960. market cap: $21.65M. volume in 24 hours: roughly $8M worth of a token where two wallets hold 86% of float. that volume has to be coming from somewhere. either the dominant wallets are actively trading their positions — which means they're comfortable moving size — or a small group of retail participants is churning aggressively in a thin market. neither reading is particularly comfortable.

38 unlock events ahead means this concentration dynamic plays out against a backdrop of continuous new supply. each monthly unlock either gets absorbed by genuine demand growth or adds to the float that those two dominant wallets already control disproportionately.

honestly don't know if the two dominant wallets are long-term believers in the verification thesis or early participants who entered cheap and are managing an orderly exit across 38 unlock events. from the data available those two stories look exactly the same.

what's your take - concentration risk already priced in or the one variable most holders haven't modeled?? 🤔