For most of crypto’s history, institutions treated blockchains as speculative venues rather than operational infrastructure. The debate focused on whether regulated capital could ever hold volatile tokens safely. What is happening around Solana now reflects a different question. Large financial organizations are no longer testing whether the network deserves attention. They are deciding which parts of their settlement and distribution stack can realistically live on it.

This shift matters because settlement is the slowest, most expensive layer of traditional finance. Payments move in batches, reconciliation spans days, and even well-capitalized banks rely on systems built decades ago. The recent integration of Solana into stablecoin settlement and tokenized instruments suggests that some institutions see it as a way to compress those timelines without rewriting their entire internal infrastructure.

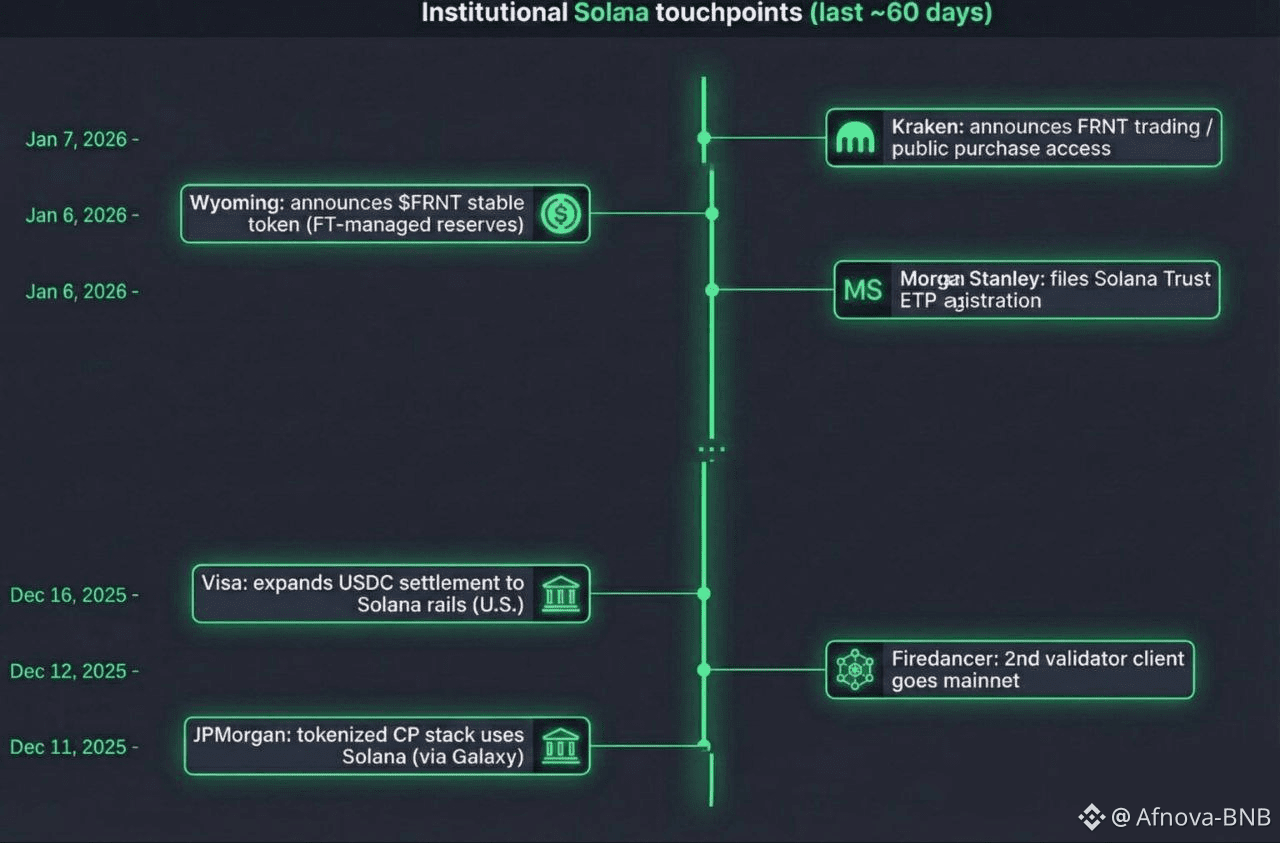

Wyoming’s launch of a state-issued digital dollar is not significant because of the token itself, but because of the governance wrapper around it. A state commission with a legal mandate and a reserve manager like Franklin Templeton chose to distribute a regulated instrument through Solana. That decision reframes Solana from a retail trading venue into a regulated distribution rail that can survive audit, disclosure, and custody requirements. It is the kind of precedent that internal compliance teams rely on when approving integration with public networks.

The Morgan Stanley trust filings belong to a different but related layer of the stack. These are not on-chain experiments. They are regulated wrappers designed to let clients gain exposure without touching the chain. What makes them relevant is timing. They arrive after generic listing standards reduced the friction of launching commodity-style crypto products. When a firm of that size treats Solana alongside Bitcoin in public filings, it signals that internal risk committees view the asset as operationally defensible, not just marketable.

These two tracks, infrastructure usage and price exposure, often get conflated. In reality they serve different institutional needs. Holding SOL through a trust product satisfies portfolio allocation. Using Solana as a settlement rail addresses back-office pain points. The latter tends to outlive market cycles because it is anchored in operational cost rather than asset appreciation.

Visa’s expansion of USDC settlement on Solana illustrates this logic. High-volume payment flows are constrained by per-transaction fees and throughput ceilings on traditional rails. Solana’s design trades extreme decentralization for speed and low marginal cost, making it suitable for clearing thousands of small transfers where human intervention would be uneconomical. In practice this means a US-based institution can settle dollar-denominated transfers in near real time without waiting on correspondent banks or overnight batches.

JPMorgan’s tokenized commercial paper experiment shows how this infrastructure gets composed with existing systems. The bank did not abandon permissioned settlement. It layered Solana on top of its JPM Coin workflows and integrated it with R3’s Corda. That hybrid approach reduces the risk of pushing sensitive workflows fully onto a public chain while still capturing the efficiency of public settlement. It is a pattern likely to repeat as banks selectively externalize pieces of their stack.

On-chain activity metrics provide a reality check on whether these integrations are symbolic. Millions of daily active addresses, tens of millions of transactions, and meaningful DEX volume indicate that the network is not idle between press releases. Tokenized real-world assets approaching a billion dollars in value show that developers are building products that require persistent storage, settlement finality, and liquidity, not just speculative trading.

Yet the architecture that enables this scale introduces its own risks. Solana’s validator economics favor well-capitalized operators, which leads to stake concentration and a lower Nakamoto coefficient than proof-of-work networks. Institutions understand this as governance risk. They need to know who can push upgrades, how quickly bugs propagate, and whether outages can be contained without coordination failure.

The introduction of Firedancer is an explicit response to that concern. By adding a second validator client, Solana reduces its dependency on a single codebase. In practical terms, it is similar to running two independent air traffic control systems in parallel. If one has a fault, the entire network does not grind to a halt. This does not decentralize stake, but it does bound systemic failure, which is often the real blocker in institutional risk models.

Stablecoin balances on Solana add another layer to this story. With a large share of supply denominated in USDC, the network functions as a quasi-dollar clearing system. That liquidity is what makes Wyoming’s stable token distribution and Visa’s settlement expansion operationally feasible. Without deep stablecoin pools, these integrations would remain pilots rather than production systems.

Consider a simple scenario. A state agency issues digital dollars backed by reserves. A resident redeems those tokens through an exchange that integrates directly with Solana. The transfer clears in seconds, the reserve ledger updates in real time, and the audit trail is available without manual reconciliation. None of this requires the resident or the agency to understand validator mechanics. They interact with a financial instrument that behaves like money but settles like software.

Whether this infrastructure succeeds over the long term depends less on token price and more on whether its risk profile remains bounded. Client diversity must continue to expand. Validator incentives must remain viable so that participation does not collapse into a handful of operators. Regulatory wrappers like trusts and state-issued tokens must keep forming around the rails so that integration does not stall at the compliance desk. If those conditions hold, Solana’s role as a settlement layer becomes less a speculative thesis and more a piece of institutional plumbing that quietly outlives the narrative cycles around it.