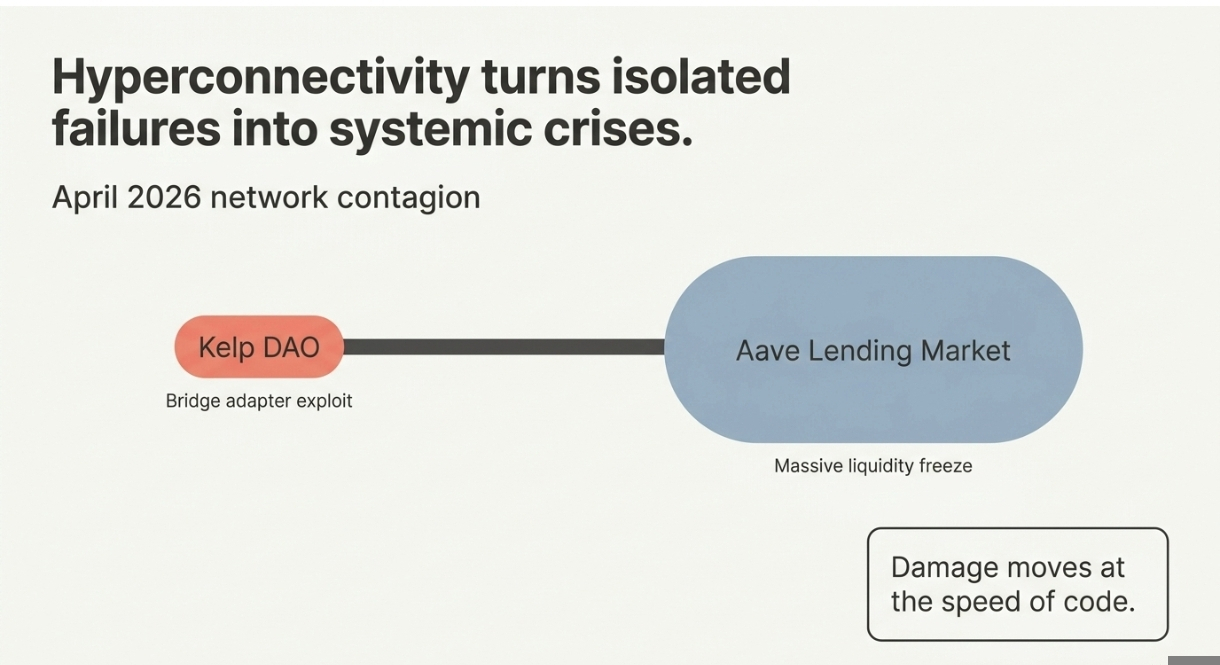

The Defi ecosystem is hyperconnected. This design allows capital to flow freely between different applications. However, this same connectivity means a failure in one isolated system can instantly infect the largest protocols in the market.

In April 2026, an exploit on a specific bridge adapter triggered a massive liquidity crisis on Aave. Hundreds of millions of dollars in legitimate user funds became completely frozen. The traditional financial world would rely on government bailouts or bankruptcy courts to resolve a crisis of this magnitude. The decentralized financial world chose a different path.

A coalition of independent protocols collaborated to build an automated emergency exit. They launched a custom smart contract in less than twenty-four hours to rescue trapped users.

II. The Anatomy of the Contagion

To understand the rescue operation, you must first understand the structural failure that trapped the users.

The crisis originated with Kelp DAO and an exploit involving its bridge adapter. An attacker manipulated the system to mint 116,500 unbacked rsETH tokens. This created approximately $293 million worth of digital assets out of thin air. These tokens had no real Ethereum backing them on the main network.

The attacker immediately deposited this unbacked rsETH into Aave as collateral. Aave algorithms recognized the rsETH as legitimate value. The attacker then used this fake collateral to borrow $236 million in real Wrapped Ethereum.

The attacker walked away with real assets. Aave was left holding hundreds of millions of dollars in worthless receipts.

III. The Liquidity Trap

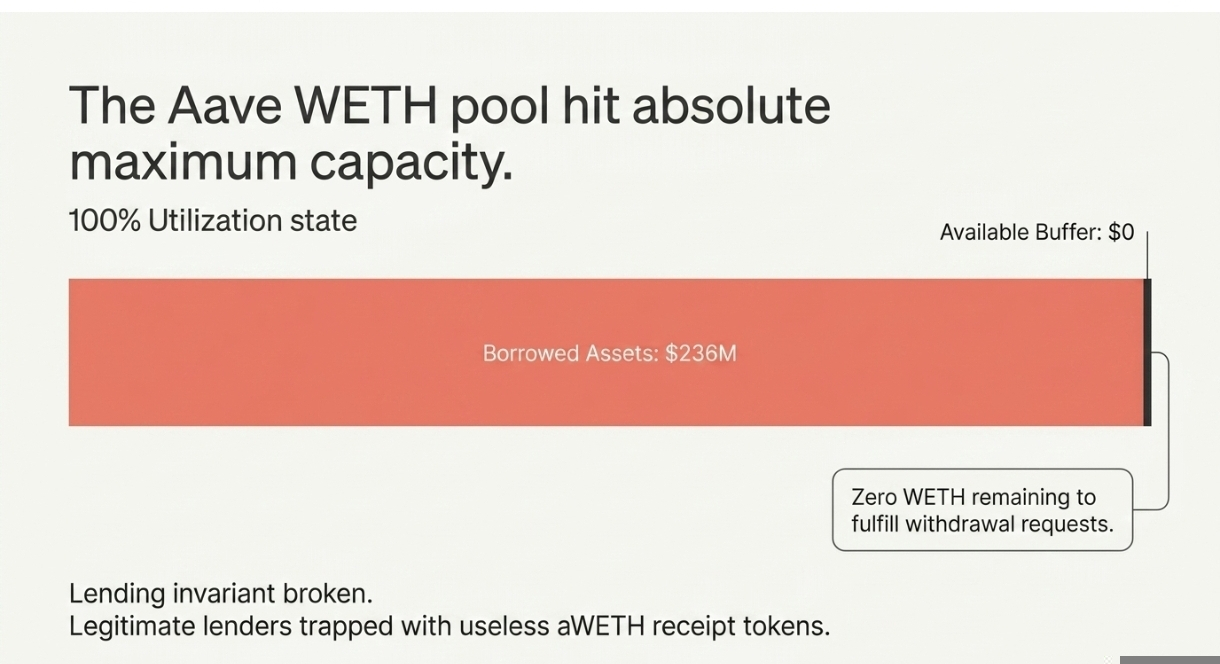

Aave operates on a pooled liquidity model. Users supply WETH to earn interest. Other users borrow that WETH and pay interest.

Under normal conditions, Aave maintains a healthy buffer of unborrowed assets. This buffer guarantees that suppliers can withdraw their funds whenever they want.

When the Kelp attacker drained $236 million in WETH, the buffer vanished. The WETH pool hit maximum capacity. This state is known as one hundred percent utilization. When utilization hits the absolute maximum limit, the lending invariant breaks. There is literally zero WETH left in the smart contract to fulfill withdrawal requests.

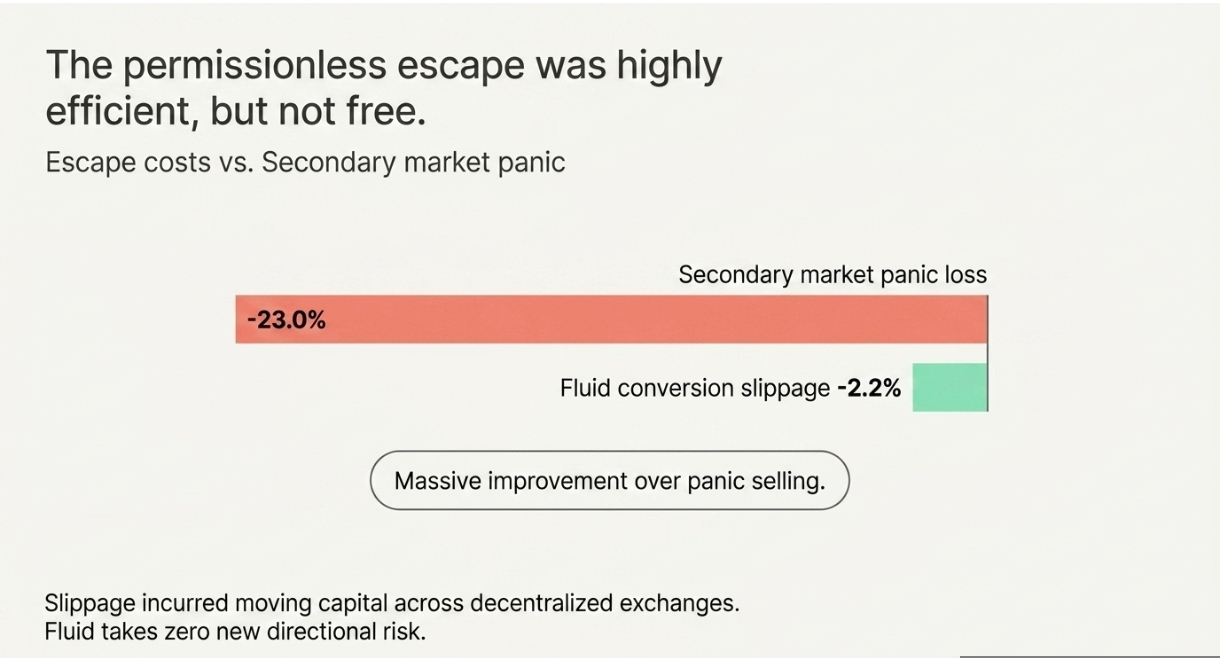

The legitimate lenders were left holding aWETH. This is the receipt token proving they supplied WETH to the protocol. Because the vault was completely empty, their aWETH receipts became useless. Panic set in. Users began selling their aWETH on secondary markets to anyone willing to buy it. Desperation pushed the price down heavily, and users were taking a twenty-three percent loss just to escape the frozen protocol.

IV. The Debt Cancellation Analogy

Think of this crisis like a crowded restaurant where the cash register suddenly breaks.

You are a customer who prepaid for a massive meal. You hold a receipt proving the restaurant owes you food. Suddenly, you realize the kitchen is completely out of ingredients. The restaurant cannot fulfill your order. You cannot get a refund because the register is broken. You are trapped with a worthless receipt.

Now imagine a massive corporate client walks into the restaurant. This client owes the restaurant a massive unpaid bar tab from previous visits.

The corporate client looks at you and makes an offer. The client will buy your prepaid receipt from you for a tiny discount. The client pays you in cash out of their own pocket. You get to leave the restaurant safely.

The corporate client then hands your prepaid receipt to the restaurant manager. The client tells the manager to use the value of your receipt to cancel out a portion of their massive bar tab.

The restaurant owes less food. The corporate client owes less money. You escape with your capital. No actual food had to leave the kitchen.

V. The Mechanical Rescue Flow

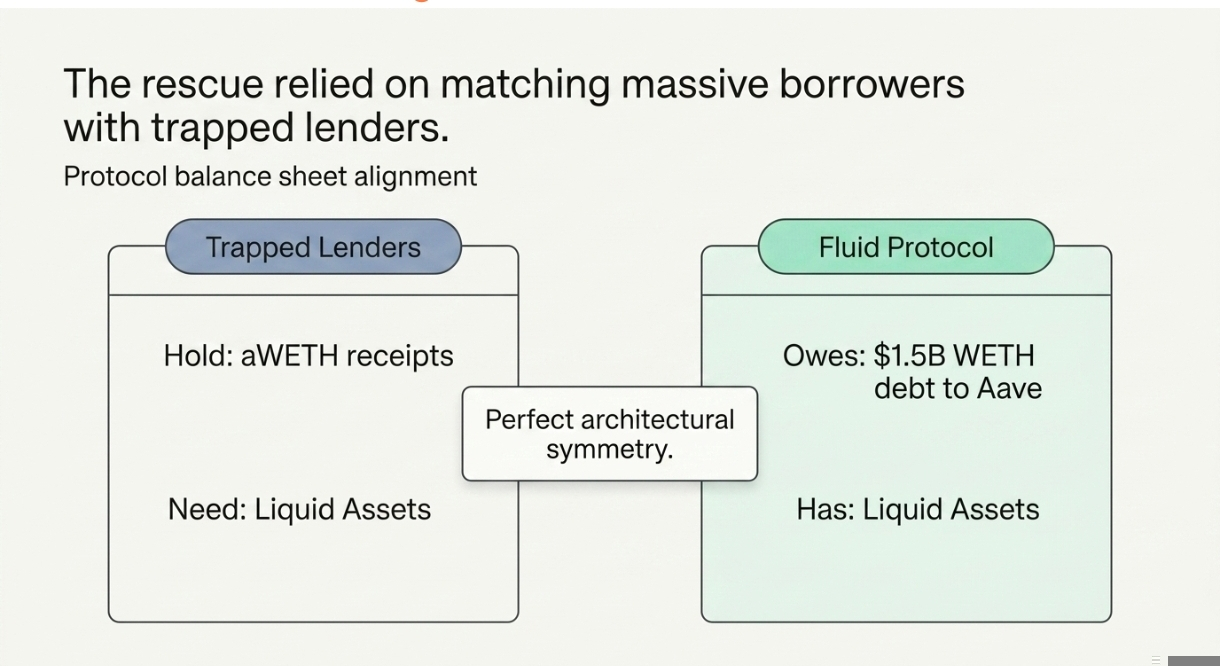

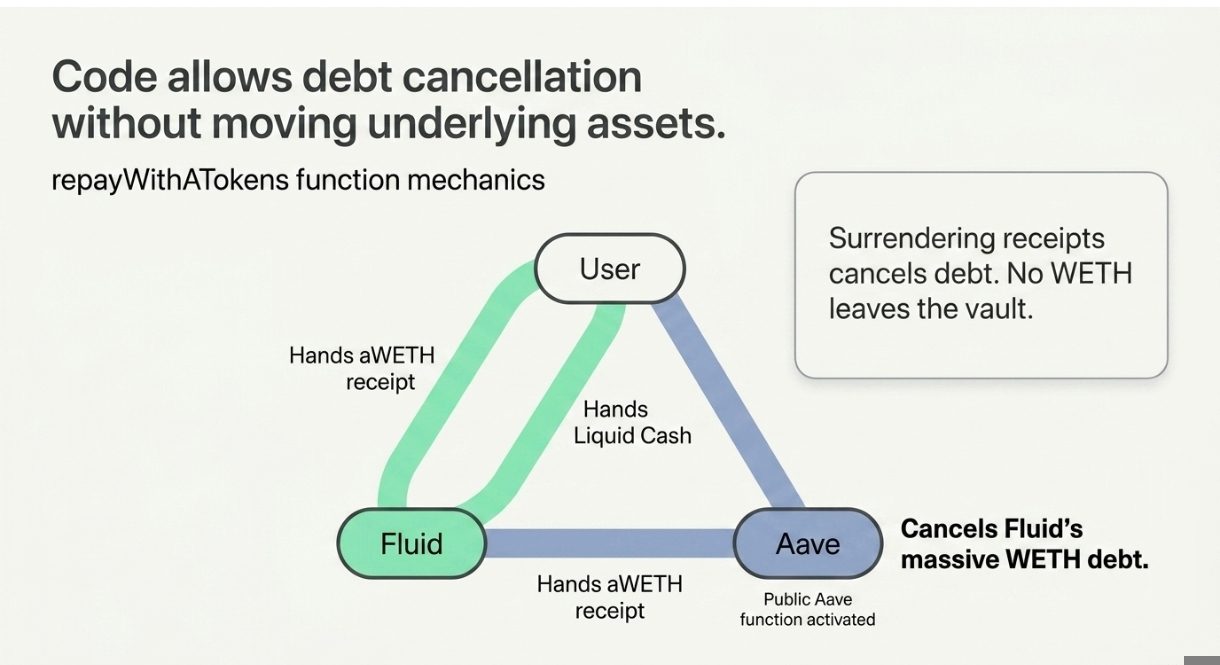

The corporate client in this scenario is a protocol named Fluid. Fluid is a decentralized exchange and lending platform. Fluid happens to be the single largest borrower of WETH on the Aave market. Fluid carries approximately $1.5 billion in WETH debt against its own vault positions.

Fluid owes Aave a massive amount of WETH. The trapped lenders hold aWETH receipts. Aave owes those lenders WETH.

Aave contains a specific public function in its code called repayWithATokens. This function allows anyone who owes Aave a debt to cancel that debt by surrendering aTokens instead of the underlying asset.

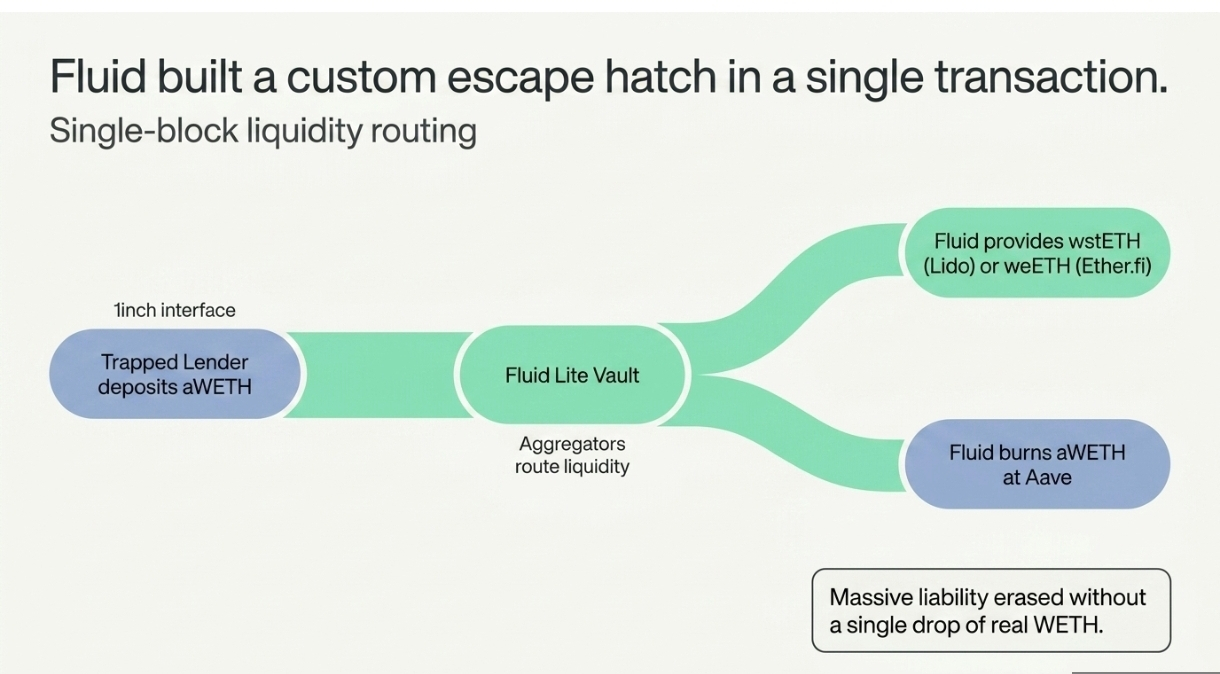

Fluid utilized this exact function to build the escape hatch. The mechanical process happens in a single transaction:

A trapped lender goes to the custom interface built by 1inch.

The lender deposits their aWETH into the Fluid Lite Vault.

Fluid accepts the aWETH and gives the lender an equivalent amount of a different liquid staking token. The lender receives wstETH supplied by Lido or weETH supplied by Ether.fi.

The lender walks away with a liquid asset they can immediately sell or hold.

Fluid takes the newly acquired aWETH and calls the repayWithATokens function on the Aave smart contract.

Aave destroys the aWETH and erases an equal portion of the WETH debt owed by Fluid.

This process extinguishes a massive liability on the Aave balance sheet without requiring a single drop of real WETH to leave the frozen pool.

VI. The Position of the Loopers

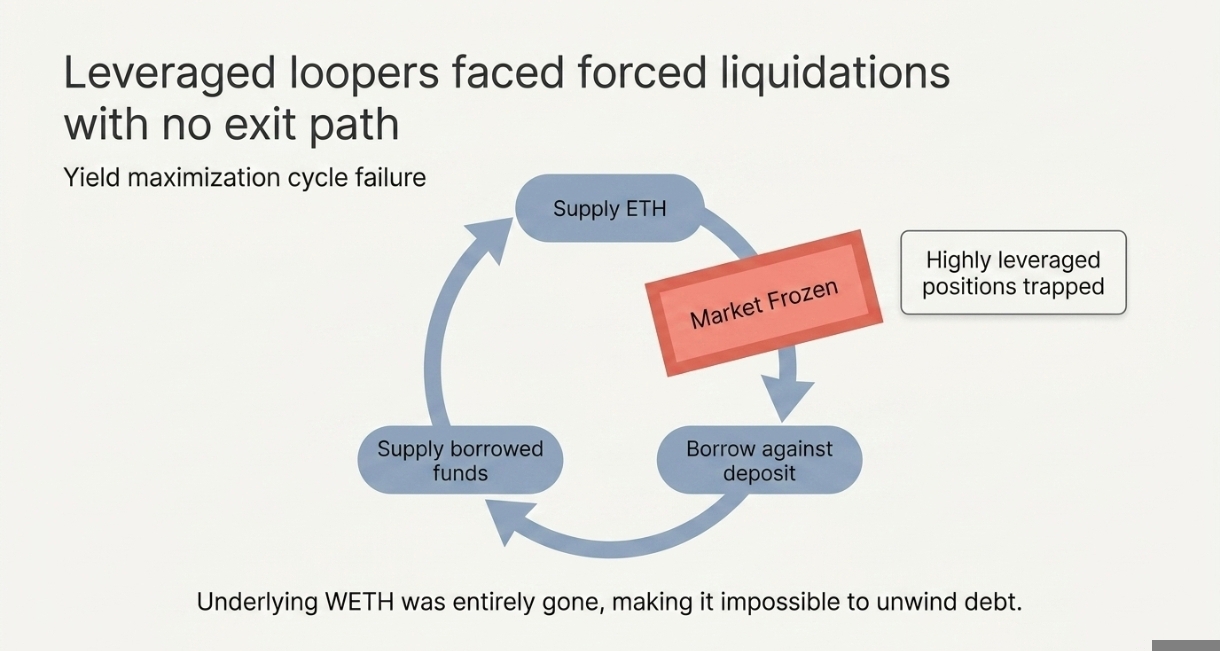

The escape hatch was not just built for simple lenders. It was also designed to rescue loopers.

Loopers are users who engage in a specific yield maximization strategy. A looper supplies Ethereum to Aave, borrows against that deposit, and then supplies the borrowed funds back into the protocol. They repeat this cycle multiple times to multiply their yield.

When the Aave market froze, the loopers were trapped in highly leveraged positions. They could not unwind their debt because the underlying WETH was entirely gone.

The Fluid infrastructure allows these specific users to safely switch their collateral. The protocol allows a looper to swap their frozen WETH collateral into wstETH or weETH collateral. Their total debt remains unchanged. However, their position is no longer tied to the frozen asset. They can safely unwind their leverage or simply hold the new yield bearing collateral on the platform.

VII. The Power of Permissionless Composability

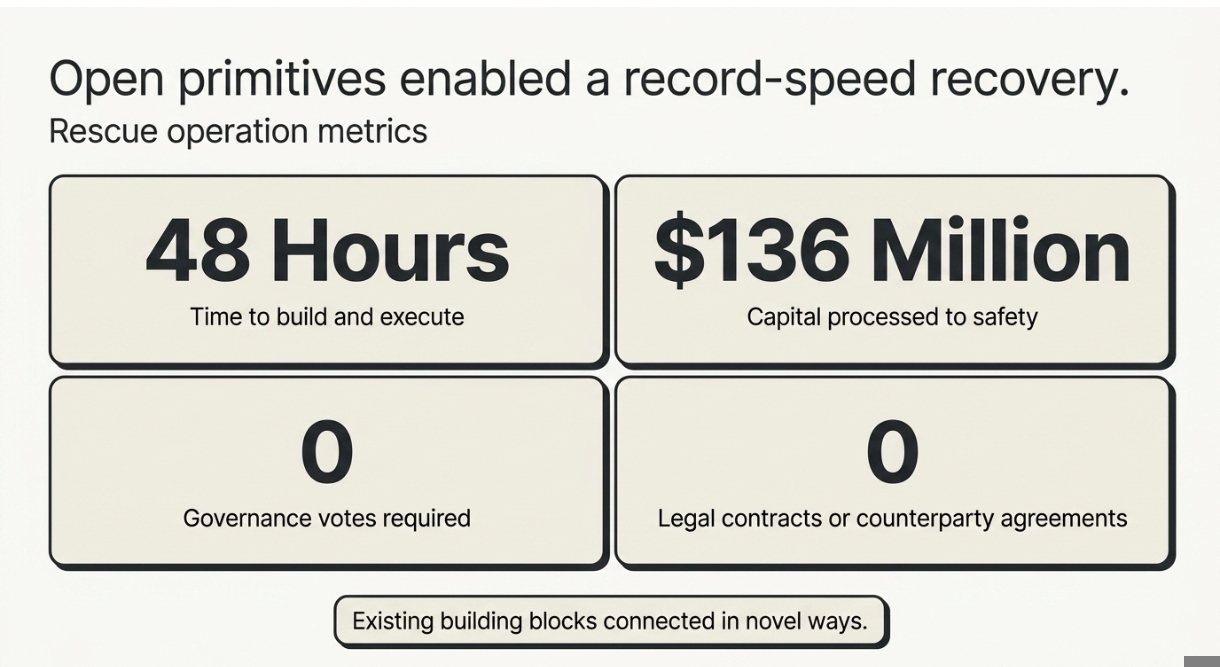

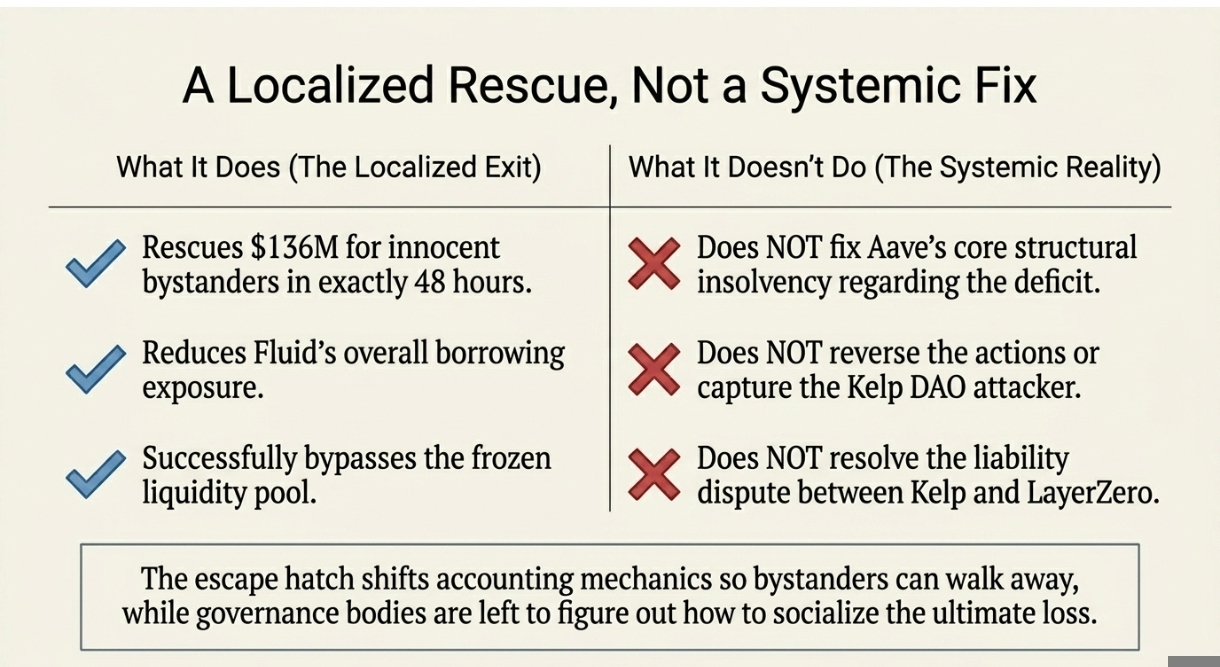

The speed of this rescue operation highlights the true defining feature of decentralized finance. It took exactly forty eight hours to process $136 million out of the frozen pool.

This happened without a single governance vote. It required zero treasury spending. It required no legal contracts or counterparty agreements.

The architecture allowed this because the building blocks are open and standardized. The aWETH token is a standard receipt. The wstETH token is a standard asset. The repayment function is public. Aggregators like 0x and Kyber Network can route liquidity from any open venue.

Fluid simply combined these existing open primitives to create a brand new route. They connected the pipes in a novel way to bypass the blockage.

VIII. The Cost of the Escape

The escape hatch is highly efficient, but it is not entirely free.

When a user executes the swap, they absorb a haircut of roughly two point two percent. If you swap one thousand frozen tokens, you lose a small fraction of your total value in the conversion process.

This discount exists because Fluid must exchange your aWETH for different liquid assets provided by external partners like Lido. Moving large amounts of capital across different decentralized exchanges always incurs a slippage cost. However, a two percent tax to instantly exit a frozen protocol is a massive improvement over the twenty three percent loss users were facing on secondary markets just hours earlier.

Fluid takes absolutely no new directional risk in this process. They are not buying the bad debt. They are simply exchanging one claim on collateral for another while reducing their own massive borrowing exposure.

IX. The Unsolved Root Problem

You must understand what this rescue protocol actually achieves. It does not fix Aave.

The escape hatch does not reduce the modeled bad debt sitting on the Aave balance sheet. It does not reverse the actions of the attacker. It does not resolve the dispute between Kelp DAO and LayerZero regarding who is ultimately responsible for the bridge failure.

The core protocol remains insolvent regarding that specific deficit. The rescue operation is strictly a localized exit for individual lenders. It shifts the accounting mechanics to allow innocent bystanders to walk away safely while the larger governance bodies figure out how to socialize the ultimate loss.

X. FIN

The Kelp DAO contagion and the Fluid rescue operation perfectly illustrate the dual nature of decentralized finance.

Composability is a double edged sword. The architectural openness allowed a failure in a small bridge adapter to instantly infect the largest lending market in the world. The damage moved at the speed of code.

However, that exact same openness allowed the ecosystem to cure itself. The solution to a catastrophic smart contract failure is rarely a human intervention. The solution is usually another smart contract designed to route liquidity around the damage.

You must stop viewing DeFi platforms as isolated banks holding your money. You must view them as interconnected ledgers. When one path is blocked, the transparent nature of the system allows anyone to build a new road out of the danger zone. And Always Do Your Own Research.