When I first came across Bitcoin, I didn’t fully understand what made it so important. It looked like just another digital currency. But after going through its original concept, I realized it’s not really about money at all. It’s about removing trust from the system.

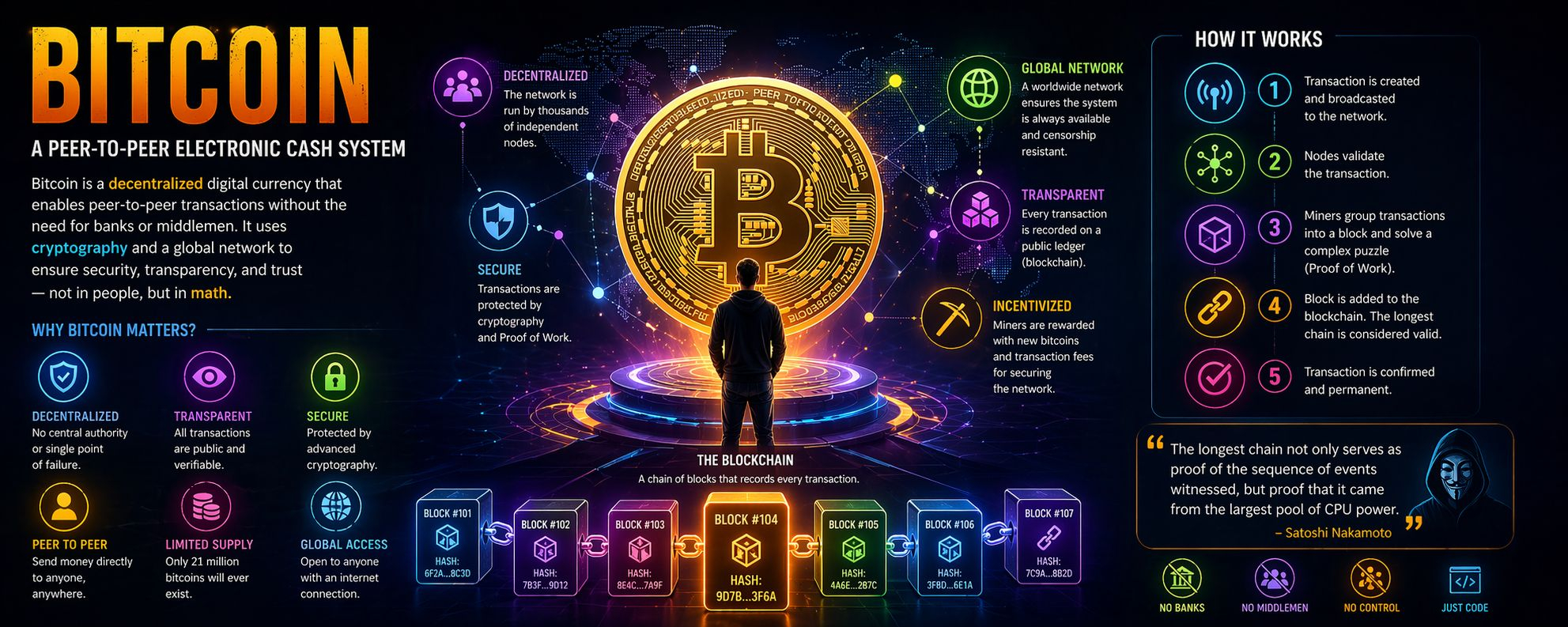

The idea behind Bitcoin is surprisingly simple. Instead of relying on banks or financial institutions to process transactions, it creates a system where people can send payments directly to each other. No middleman, no approval, no control from a central authority.

This matters more than it sounds.

In traditional finance, everything depends on trust. You trust banks to hold your money, process your payments, and resolve disputes. But that trust comes with costs. Transactions can be reversed, fees are added, and access is controlled. It works, but it’s not perfect.

Bitcoin approaches this differently.

Instead of trust, it uses cryptographic proof. Every transaction is recorded and verified by a network of participants. These transactions are grouped into blocks, and each block is linked to the one before it, forming a chain. This structure makes it extremely difficult to alter past records.

This is what we now call blockchain.

But the real challenge Bitcoin solved is something called double spending. In digital systems, it’s easy to copy data. So how do you make sure someone doesn’t spend the same digital coin twice?

The solution is clever.

All transactions are shared across the network. Participants, often called nodes, keep track of them. Special participants, known as miners, compete to add new blocks to the chain by solving complex computational problems. This process is called proof of work.

Once a block is added, it becomes part of a growing history that is extremely hard to change. To rewrite it, someone would need to redo the work of that block and every block after it, which requires massive computational power.

This is where security comes from.

As long as most of the network is honest, the system remains reliable. The longest chain represents the valid history, and the network automatically agrees on it without needing a central authority.

Another interesting part of the system is incentives.

Miners are rewarded for their work. They receive newly created coins and transaction fees. This encourages people to support the network and keeps the system running smoothly. Instead of relying on a company or government, Bitcoin relies on aligned incentives.

But this model isn’t without challenges.

Proof of work consumes a lot of energy. As the network grows, scalability becomes an issue. There are also concerns about mining becoming concentrated in certain regions or groups. And of course, price volatility adds another layer of uncertainty.

Still, none of these take away from the core idea.

Bitcoin introduced a new way of thinking. It showed that it’s possible to build a system where participants don’t need to trust each other, yet can still interact securely. That idea goes far beyond payments.

It’s a shift from “trust people” to “trust the system.”

And that shift is what makes Bitcoin more than just a digital currency. It’s a foundation for a new kind of financial structure, one where control is distributed, rules are transparent, and participation is open.

For me, understanding this changed how I see not just Bitcoin, but the entire space built around it.

It’s not just about sending money.

It’s about redefining how systems can work without relying on trust.